大摩还表示,台积电仍然是其在AI半导体供应链中的首选,台积电保证了AI真实的需求,且这家云服务提供商正在设计自己的AI芯片(ASIC定制芯片),这提升了市场对AI半导体的信心。

大摩还表示,台积电仍然是其在AI半导体供应链中的首选,台积电保证了AI真实的需求,且这家云服务提供商正在设计自己的AI芯片(ASIC定制芯片),这提升了市场对AI半导体的信心。當下市場聚焦雲計算巨頭的資本支出和台積電CoWoS封裝產能的分配。大摩認爲,AMD似乎已經削減了2025年在臺積電的CoWoS訂單,但這部分產能立即被英偉達接手,預計到2025年,英偉達的需求佔比將達63%。雲計算資本支出由於對GPU器的投資,同比增長正在加速,或在2025上半年達峯值。

隨着芯片產業駛入「快車道」,市場的焦點轉向美國雲計算巨頭的資本支出和台積電CoWoS(封裝)產能的分配,這些或在短期內導致較劇烈的市場波動。

10月23日,摩根士丹利分析師Charlie Chan、Daniel Yen等發佈報告稱,目前對人工智能持樂觀態度,但市場對第四季度資本支出的預期可能過高,最終可能並不理想。而云AI半導體客戶仍在進行生產轉型,更多的採購將在2025年上半年進行。

大摩還表示,台積電仍然是其在AI半導體供應鏈中的首選,台積電保證了AI真實的需求,且這家雲服務提供商正在設計自己的AI芯片(ASIC定製芯片),這提升了市場對AI半導體的信心。

大摩還表示,台積電仍然是其在AI半導體供應鏈中的首選,台積電保證了AI真實的需求,且這家雲服務提供商正在設計自己的AI芯片(ASIC定製芯片),這提升了市場對AI半導體的信心。

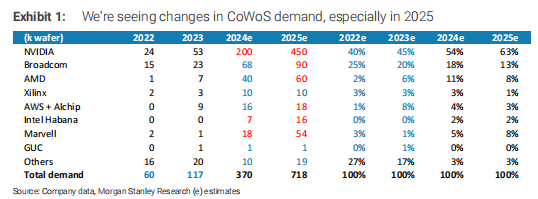

CoWoS分配洗牌,英偉達接手AMD

總的來看,台積電CoWoS產能預計在2024年將達到370萬塊晶圓,而到2025年這一數字將增長至718萬塊。

大摩在報告中指出,近期,CoWoS需求動態發生了一些變化。鑑於對新AI芯片MI325需求的不確定性,AMD似乎已經削減了2025年在臺積電的部分CoWoS晶圓訂單,需求由2024年的11%,減少至2025年的13%。但台積電的訂單情況似乎仍然穩健,這部分產能立即被英偉達接手,預計到2025年,英偉達的需求佔比將達63%。

英特爾旗下AI芯片製造商Habana尚未改變其在臺積電的晶圓預訂量,Marvell則將2025年在臺積電的預訂量提高到2024年的三倍,Alchip也開始爲一些3nm項目預訂一些CoWoS。

值得注意的是,台積電還在最近的業績電話會議上提到,公司正在設計自己的AI芯片(ASIC),且似乎保留了其30%的CoWoS產能用於ASIC。

此外,大摩還預計,如果2024年亞馬遜的Trainium 2產量爲20萬塊,那麼依據CoWoS產能預訂情況,到了2025年,Trainium 2的產量可能達到40萬塊,Inferentia 2.5的產量則可能達到50-60萬塊。

而對於英特爾Gaudi 3,大摩認爲,其2025年的AI服務器數量約爲2-2.5萬塊,這意味着芯片消耗量爲16-20萬塊,與其16k CoWoS預訂量一致,芯片產量約爲20萬塊。

雲計算資本支出可能在2025上半年達峯值

在雲計算巨頭的資本支出方面,大摩指出,在過去的週期中,一個2-3年的上升週期通常後面會跟隨2-4個季度的下降期。下降週期指「年同比增長放緩」,尤其是來自美國超大規模雲計算公司的放緩。

2024年第二季度美國雲資本支出數據顯示,雲資本支出已從2023年第二季度和第三季度的底部回升。由於對GPU服務器的投資,雲資本支出同比增長正在加速。

大摩表示,如果這一週期重複,上升週期可能會持續到2025年上半年。

歷史數據顯示,當數據中心建設處於起步階段時(2005-2015年),更容易看到資本支出增長大幅增加。2015年後,由於「摩爾定律」放緩和雲服務提供商銷售增長減速,資本支出增長趨於正常化。大摩在報告中稱,隨着GPU的快速發展並具有未來貨幣化的潛力,2025年第一季度資本支出同比增長可能仍然強勁,超過30%:

「因此,根據歷史趨勢,週期峯值應該出現在2025年上半年。」

編輯/rice