Can Entegris, Inc. (NASDAQ:ENTG) Improve Its Returns?

Can Entegris, Inc. (NASDAQ:ENTG) Improve Its Returns?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity One of the best investments we can make is in our own knowledge and skill set. With that in mind, this article will work through how we can use Return On Equity (ROE) to better understand a business. By way of learning-by-doing, we'll look at ROE to gain a better understanding of Entegris, Inc. (NASDAQ:ENTG).

我們可以做的最好的投資之一是投資於自己的知識和技能。考慮到這一點,本文將介紹我們如何利用淨資產收益率(roe)來更好地理解業務。通過學以致用,我們將通過ROE來更好地了解Entegris公司(納斯達克:英特格)。

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors' money. Put another way, it reveals the company's success at turning shareholder investments into profits.

ROE,即淨資產收益率,測試一家公司有效增加價值和管理股東資金的能力。換句話說,它揭示了公司將股東投資轉化爲利潤的成功程度。

How Do You Calculate Return On Equity?

怎樣計算ROE?

The formula for ROE is:

roe的公式是:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

淨資產收益率 = 淨利潤(從持續經營中獲得)÷ 股東權益

So, based on the above formula, the ROE for Entegris is:

因此,根據上述公式,英特格的ROE爲:

5.3% = US$184m ÷ US$3.5b (Based on the trailing twelve months to June 2024).

5.3% = 18400萬美元 ÷ 35億美元(截至2024年6月的過去十二個月)。

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.05 in profit.

「回報」是過去十二個月的利潤。概念化這一點的一種方式是,對於每1美元的股東資本,公司獲得了0.05美元的利潤。

Does Entegris Have A Good ROE?

英特格的ROE值如何?

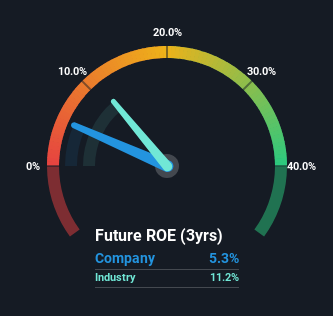

Arguably the easiest way to assess company's ROE is to compare it with the average in its industry. Importantly, this is far from a perfect measure, because companies differ significantly within the same industry classification. If you look at the image below, you can see Entegris has a lower ROE than the average (11%) in the Semiconductor industry classification.

可以說,評估公司ROE的最簡單方法是將其與同行業的平均值進行比較。 重要的是,這遠非完美的衡量標準,因爲同一行業內的公司存在顯著差異。 如果您看下面的圖片,您會發現英特格的ROE低於半導體行業分類的平均水平(11%)。

That's not what we like to see. However, a low ROE is not always bad. If the company's debt levels are moderate to low, then there's still a chance that returns can be improved via the use of financial leverage. A high debt company having a low ROE is a different story altogether and a risky investment in our books. To know the 2 risks we have identified for Entegris visit our risks dashboard for free.

這不是我們願意看到的。 然而,低ROE並不總是不好的。 如果公司的債務水平適中或較低,則仍然有可能通過使用財務槓桿來改善回報。 一個高負債公司的低ROE則完全是另一回事,在我們看來是一種風險投資。 要了解我們爲英特格確定的兩個風險,請免費訪問我們的風險儀表板。

Why You Should Consider Debt When Looking At ROE

爲什麼在觀察ROE時你應該考慮債務問題?

Most companies need money -- from somewhere -- to grow their profits. That cash can come from retained earnings, issuing new shares (equity), or debt. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the use of debt will improve the returns, but will not change the equity. That will make the ROE look better than if no debt was used.

大多數公司需要資本來增加利潤。這些資本可以來自保留收益,發行新股(權益)或債務。在前兩種情況下,ROE將捕獲這種資本用於增長的情況。在後一種情況下,使用債務將提高回報,但不會改變股權。這將使ROE看起來比沒有使用債務要好。

Entegris' Debt And Its 5.3% ROE

英特格的債務及其5.3%的roe

Entegris does use a high amount of debt to increase returns. It has a debt to equity ratio of 1.18. With a fairly low ROE, and significant use of debt, it's hard to get excited about this business at the moment. Investors should think carefully about how a company might perform if it was unable to borrow so easily, because credit markets do change over time.

英特格確實使用大量債務來提高回報率。其債務資產比爲1.18。由於roe相對較低且大量使用債務,目前很難對這家業務感到興奮。投資者應認真思考,一家公司如果無法輕鬆借款,其表現可能如何,因爲信貸市場確實會隨時間發生變化。

Conclusion

結論

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. In our books, the highest quality companies have high return on equity, despite low debt. All else being equal, a higher ROE is better.

股本回報率是衡量企業創造利潤並返還給股東的能力的有用指標。在我們的觀念中,高股本回報率的高質量公司儘管負債率較低,但其他事項均相等。 其他事項均相等的情況下,較高的ROE更好。

But when a business is high quality, the market often bids it up to a price that reflects this. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to check this FREE visualization of analyst forecasts for the company.

但是,當一個業務質量高的公司時,市場通常會將其競拍到反映這一點的價格。利潤增長率相對於股票價格反映的預期,是特別重要考慮的因素。因此,您可能想要查看分析師對該公司的預測的這個免費可視化。

Of course Entegris may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

當然,英特格可能不是最佳股票購買選擇。因此,您可能希望查看這些具有高roe和低債務的其他公司的免費集合。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。