Capital Allocation Trends At Kronos Worldwide (NYSE:KRO) Aren't Ideal

Capital Allocation Trends At Kronos Worldwide (NYSE:KRO) Aren't Ideal

0.023 = US$32m ÷ (US$1.7b - US$273m)

0.023 = US$32m ÷ (US$1.7b - US$273m) Ignoring the stock price of a company, what are the underlying trends that tell us a business is past the growth phase? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. And from a first read, things don't look too good at Kronos Worldwide (NYSE:KRO), so let's see why.

忽略一家公司的股价,有哪些潜在趋势告诉我们一个业务已经过了增长阶段?通常情况下,我们会看到已被使用资本回报率(ROCE)的趋势下降,这通常与被使用资本的数量减少同时发生。这样的趋势最终意味着业务正在减少其投资,也在其投资上赚得更少。从初步阅读来看,康诺斯全球(纽交所:KRO)情况不太乐观,让我们看看为什么。

What Is Return On Capital Employed (ROCE)?

我们对 Enphase Energy 的资本雇用回报率的看法:正如我们上面看到的,Enphase Energy 的资本回报率没有提高,但它正在重新投资于业务。投资者必须认为未来会有更好的前景,因为股票表现良好,使持股五年以上的股东获得了 690% 的收益。最终,如果基本趋势持续存在,我们不会对它成为一只多头股持有期很久很有信心。

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Kronos Worldwide is:

只是为了澄清,如果您不确定,ROCE是评估公司在其业务投资中赚取多少税前收入(以百分比表示)的指标。在康诺斯全球的计算公式如下:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

资产雇用回报率(ROCE)是指企业利润,即企业税前利润除以企业投入的总资本(负债加股权)。如果ROCE高于企业财务成本的承受能力,那么企业就会创造出更多的价值。

0.023 = US$32m ÷ (US$1.7b - US$273m) (Based on the trailing twelve months to June 2024).

0.023 = 3200万美元 ÷ (17亿美元 - 2.73亿美元)(基于截至2024年6月的最近十二个月)。

Therefore, Kronos Worldwide has an ROCE of 2.3%. Ultimately, that's a low return and it under-performs the Chemicals industry average of 8.7%.

因此,康诺斯全球的ROCE为2.3%。最终,这是一个较低的回报率,低于化学品行业平均值8.7%。

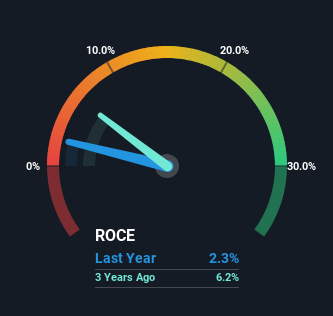

Above you can see how the current ROCE for Kronos Worldwide compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Kronos Worldwide .

在这里,您可以看到康诺斯全球当前的资本回报率与先前的资本回报率相比,但过去仅能了解有限。如果您感兴趣,您可以查看我们为康诺斯全球准备的免费分析师报告中分析师的预测。

So How Is Kronos Worldwide's ROCE Trending?

那么,康诺斯全球的资本回报率趋势如何?

There is reason to be cautious about Kronos Worldwide, given the returns are trending downwards. About five years ago, returns on capital were 10%, however they're now substantially lower than that as we saw above. Meanwhile, capital employed in the business has stayed roughly the flat over the period. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. If these trends continue, we wouldn't expect Kronos Worldwide to turn into a multi-bagger.

对于康诺斯全球存在谨慎的理由,即资本回报率呈下降趋势。大约五年前,资本回报率为10%,然而,正如我们上面所看到的,现在远低于此水平。同时,业务中使用的资本在这段时期基本持平。这种组合可能表明一家仍有部分资本可供运营的成熟企业,但由于可能面临新竞争或利润率较低,实际收益较低。如果这些趋势持续下去,我们不会期望康诺斯全球成为一个巨大成功的投资标的。

The Key Takeaway

重要提示

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. Investors must expect better things on the horizon though because the stock has risen 27% in the last five years. Either way, we aren't huge fans of the current trends and so with that we think you might find better investments elsewhere.

总的来说,同等资本投入带来更低回报并非复利机器的迹象。投资者必须期待未来会有更好的情况发生,因为股价在过去五年里上涨了27%。无论如何,我们并不支持当前的趋势,因此我们认为您可能会在其他地方找到更好的投资机会。

Kronos Worldwide does have some risks, we noticed 3 warning signs (and 1 which is a bit concerning) we think you should know about.

康诺斯全球确实存在一些风险,我们注意到了3个警示标志(以及一个有点令人担忧的),我们认为您应该了解这些。

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Hao Tian International Construction Investment Group确实存在一些风险,我们已经发现了一条警示标志,你可能会感兴趣。对于那些喜欢投资于实力雄厚的公司的人,可以查看这个由财务状况强大、股本回报率高的公司组成的免费列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有任何反馈?对内容有任何疑虑?请直接与我们联系。或者,发送电子邮件至editorial-team@simplywallst.com。

这篇文章是Simply Wall St的一般性文章。我们根据历史数据和分析师预测提供评论,只使用公正的方法论,我们的文章并不意味着提供任何金融建议。文章不构成买卖任何股票的建议,也不考虑您的目标或您的财务状况。我们的目标是带给您基本数据驱动的长期关注分析。请注意,我们的分析可能不考虑最新的价格敏感公司公告或定性材料。Simply Wall St没有任何股票头寸。

译文内容由第三方软件翻译。