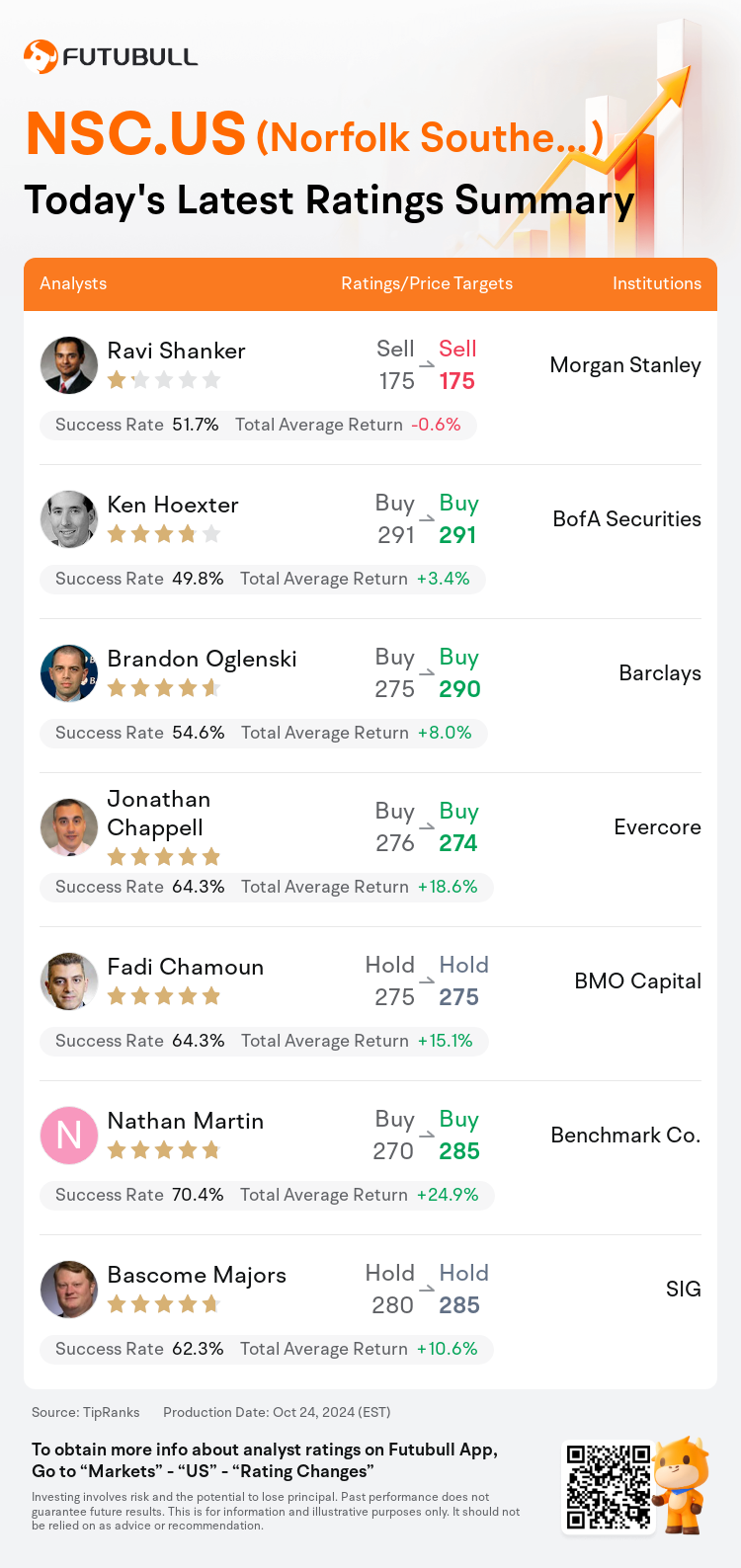

On Oct 24, major Wall Street analysts update their ratings for $Norfolk Southern (NSC.US)$, with price targets ranging from $175 to $291.

Morgan Stanley analyst Ravi Shanker maintains with a sell rating, and maintains the target price at $175.

BofA Securities analyst Ken Hoexter maintains with a buy rating, and maintains the target price at $291.

Barclays analyst Brandon Oglenski maintains with a buy rating, and adjusts the target price from $275 to $290.

Barclays analyst Brandon Oglenski maintains with a buy rating, and adjusts the target price from $275 to $290.

Evercore analyst Jonathan Chappell maintains with a buy rating, and adjusts the target price from $276 to $274.

BMO Capital analyst Fadi Chamoun maintains with a hold rating, and maintains the target price at $275.

Furthermore, according to the comprehensive report, the opinions of $Norfolk Southern (NSC.US)$'s main analysts recently are as follows:

Norfolk Southern's recent earnings disclosure was comparatively positive. Despite various challenges anticipated to affect Q4 margins, there is a pathway identified for the company to significantly enhance its profitability by 2025, which is seen in relation to a compelling equity valuation.

The company is identified to have significant potential to enhance margins more so than other Class 1 rails in the near to medium term, considering it starts from a lower base compared to its competitors. The recorded 480 basis points of margin growth in the second quarter and an additional 170 basis points in the third quarter signify progress in the right direction. The company's recent increase in carloads, approximately 4% higher than the previous year, and the expected continuous narrowing of its operating ratio gap across Eastern network geographies supports this positive outlook.

Norfolk Southern's third-quarter adjusted earnings per share increased by 23% compared to the previous year, surpassing the consensus estimates. The company has also maintained its target for a 66% full-year operating ratio, despite a reduction in its 2024 revenue growth forecast to 1% year-over-year from an earlier projection of 3%. The expectation is that Norfolk Southern will enhance its earnings through productivity improvements.

Following the company's quarterly results, it's noted that the Chief Operating Officer is making significant progress in areas where the company has faced challenges in the past. The implementation of precision scheduled railroading and the pursuit of efficiency gains are contributing to margin enhancements. The company's confidence in achieving an operating ratio below 60 is supported by macroeconomic factors, even though the impressive operating ratio this quarter may have been influenced in part by volume and operating leverage advancements.

Norfolk Southern's recent quarterly earnings surpassed expectations, highlighting the company's effective cost-saving measures and indicating a significant structural cost turnaround. Comparatively, this quarter was particularly strong when measured against a competitor that experienced more challenges during the same period.

Here are the latest investment ratings and price targets for $Norfolk Southern (NSC.US)$ from 7 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

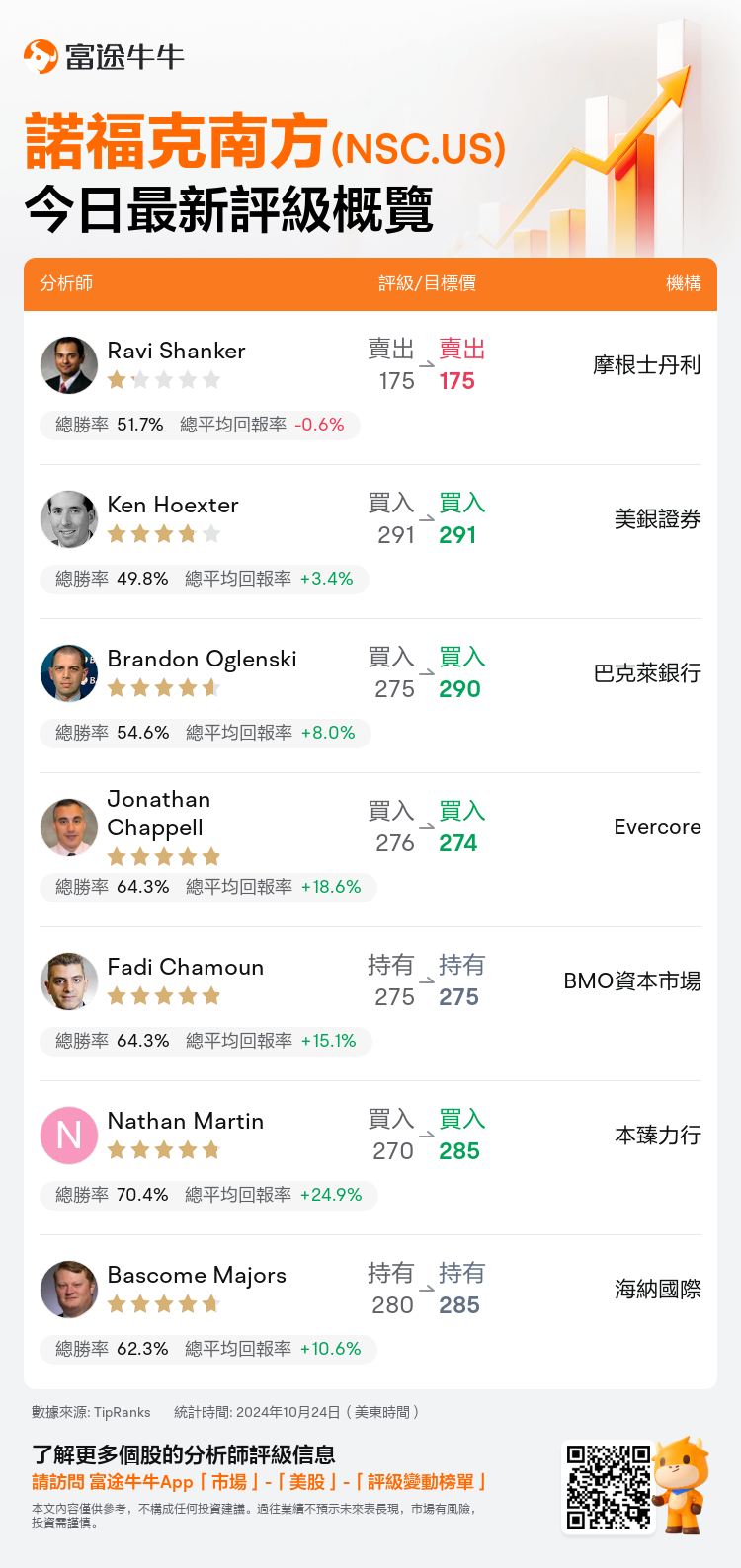

美東時間10月24日,多家華爾街大行更新了$諾福克南方 (NSC.US)$的評級,目標價介於175美元至291美元。

摩根士丹利分析師Ravi Shanker維持賣出評級,維持目標價175美元。

美銀證券分析師Ken Hoexter維持買入評級,維持目標價291美元。

巴克萊銀行分析師Brandon Oglenski維持買入評級,並將目標價從275美元上調至290美元。

巴克萊銀行分析師Brandon Oglenski維持買入評級,並將目標價從275美元上調至290美元。

Evercore分析師Jonathan Chappell維持買入評級,並將目標價從276美元下調至274美元。

BMO資本市場分析師Fadi Chamoun維持持有評級,維持目標價275美元。

此外,綜合報道,$諾福克南方 (NSC.US)$近期主要分析師觀點如下:

諾福克南方最近披露的收益狀況相對積極。儘管預計各種挑戰將影響第四季度的利潤率,但已確定了一條路徑,公司可在2025年顯着增強其盈利能力,這與引人注目的股權估值相關。

相較於其他一級鐵路公司,諾福克南方在近至中期內被確定具有顯著的增強利潤空間潛力,考慮到它相對競爭對手更低的起點。第二季度記錄的邊際增長480個點子以及第三季度額外的170個點子表明了取得正確進展。公司最近的裝車量增加約4%,較前一年高,預計其在東部網絡地理區域間的運營比率縮小將支持這一積極展望。

諾福克南方第三季度調整後的每股收益較前一年增長了23%,超過共識估計。儘管其2024年營收增長預期從3%降至1%,但公司也保持了全年運營比率66%的目標。預期諾福克南方將通過提升生產力改善盈利。

根據公司季度業績,首席營運官正取得在公司過去面臨挑戰的領域取得重大進展。實施精準調度鐵路和尋求效率收益正在促進邊際增強。儘管本季度的出色運營比率在一定程度上可能受到成交量和運營槓桿方面的進展影響,公司對實現低於60的運營比率的信心得到了宏觀經濟因素的支撐。

諾福克南方最近的季度收益超出預期,突顯了公司有效的節約成本措施,並表明了重大結構性成本轉變。比較而言,本季度在同期經歷更多挑戰的競爭對手的表現尤爲強勁。

以下爲今日7位分析師對$諾福克南方 (NSC.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。