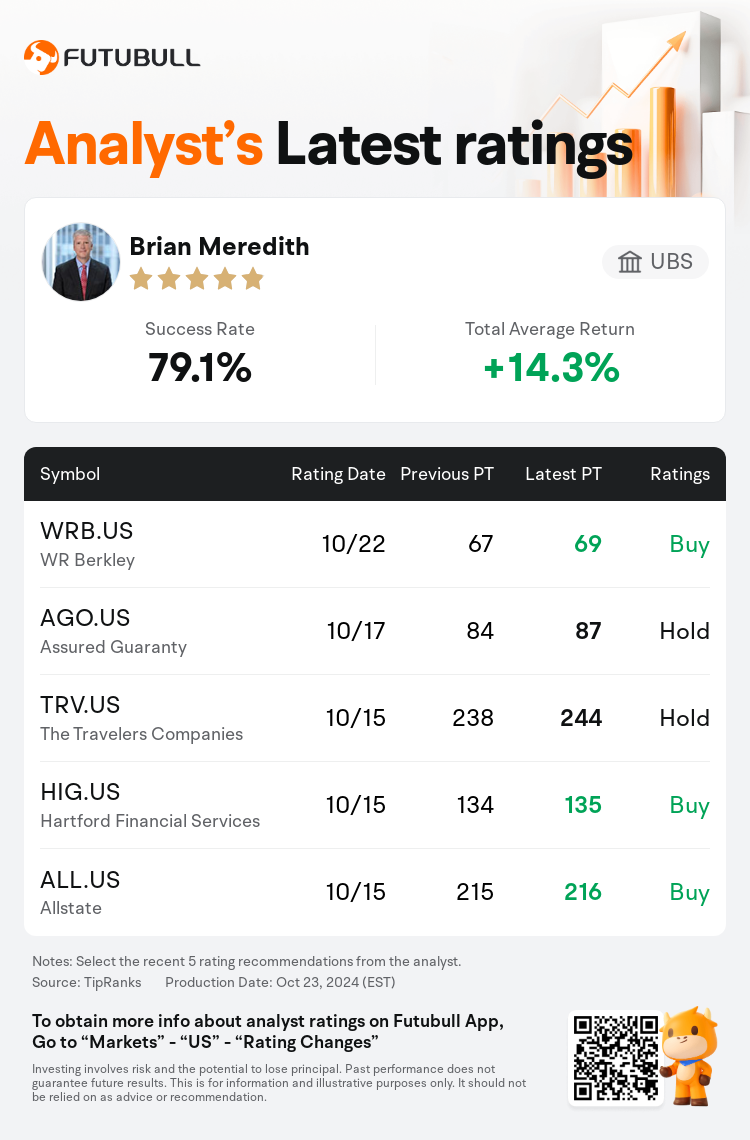

UBS analyst Brian Meredith maintains $WR Berkley (WRB.US)$ with a buy rating, and adjusts the target price from $67 to $69.

According to TipRanks data, the analyst has a success rate of 79.1% and a total average return of 14.3% over the past year.

Furthermore, according to the comprehensive report, the opinions of $WR Berkley (WRB.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $WR Berkley (WRB.US)$'s main analysts recently are as follows:

Following Q3 results, the expectation for W. R. Berkley's valuation has increased, with the recognition that it has historically maintained a significant premium compared to peer multiples. This is attributed to its long-term success in growing equity at a rate surpassing that of other top-performing peers.

The company's Q3 outcomes were consistent, displaying strong combined ratios even amidst heightened catastrophe losses. Although there was an uptick in the expense ratio, attributed to growth initiatives and technological investments, and a slight slowdown in premium growth compared to previous rates, the management remains optimistic about growth prospects throughout various sectors of the business.

After W. R. Berkley revealed Q3 operating EPS of 93c, exceeding both the expected 90c estimate and the consensus forecast of 92c, it is believed to have been a solid quarter, although it may have slightly underwhelmed in comparison to peer results, given that net premium growth fell short and rate hikes were modest. There's indication of rate gains in auto and other liability coverages, but it's challenging to foresee rates climbing sufficiently across the insurer's portfolio to reach the anticipated 10%-15% growth in Q4. It seems that the consensus viewpoint aligns with this perspective.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

瑞士銀行分析師Brian Meredith維持$WR柏克利 (WRB.US)$買入評級,並將目標價從67美元上調至69美元。

根據TipRanks數據顯示,該分析師近一年總勝率為79.1%,總平均回報率為14.3%。

此外,綜合報道,$WR柏克利 (WRB.US)$近期主要分析師觀點如下:

此外,綜合報道,$WR柏克利 (WRB.US)$近期主要分析師觀點如下:

根據Q3的業績結果,市場對W. R.伯克利的估值預期有所提高,認識到與同行相比,它歷史上一直保持着明顯的溢價。這可歸因於其長期成功地以超過其他表現優異的同行的速度增加股本。

公司第三季度的業績表現穩健,即使在災難損失增加的情況下,合併比率仍然強勁。儘管費用比率有所上升,這歸因於增長計劃和技術投資,而且與之前的增長速度相比,保費增長略有放緩,但管理層仍對業務各領域的增長前景持樂觀態度。

在W.R.伯克利公佈第三季度運營每股收益爲93美分後,超過了預期的90美分估計和92美分的共識預測,人們認爲這是一個穩健的季度,儘管與同行相比可能略顯遜色,由於淨保費增長不足且費率上漲幅度適中。有跡象顯示汽車和其他責任保險涵蓋範圍的費率提升,但很難預見保險公司組合內的費率是否能夠足夠提升以實現預期的第四季度10%-15%的增長。似乎共識觀點與這一看法一致。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。