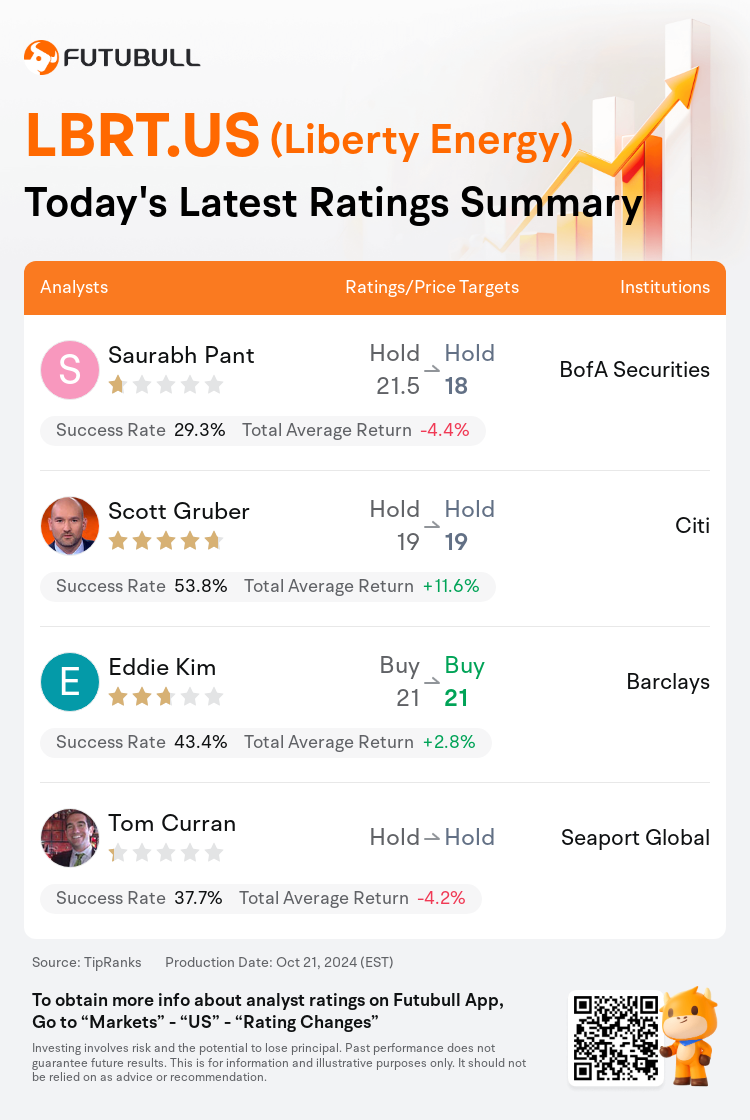

On Oct 21, major Wall Street analysts update their ratings for $Liberty Energy (LBRT.US)$, with price targets ranging from $18 to $21.

BofA Securities analyst Saurabh Pant maintains with a hold rating, and adjusts the target price from $21.5 to $18.

Citi analyst Scott Gruber maintains with a hold rating, and maintains the target price at $19.

Barclays analyst Eddie Kim maintains with a buy rating, and maintains the target price at $21.

Barclays analyst Eddie Kim maintains with a buy rating, and maintains the target price at $21.

Seaport Global analyst Tom Curran maintains with a hold rating.

Furthermore, according to the comprehensive report, the opinions of $Liberty Energy (LBRT.US)$'s main analysts recently are as follows:

Pricing challenges in the frac sector have extended to top-tier pumpers and equipment, which is reflected in Liberty Energy's recognition of 'slowing activity pressuring pricing inconsistent with [its] anticipated future demand.' It is anticipated that Liberty's realized pricing may face further weakening prior to an improvement.

Liberty Energy experienced a challenging quarter, missing Q3 EBITDA expectations by 5% and forecasting Q4 results that are 25% below the consensus. This has resulted in management losing some credibility with investors.

The intensification of the downcycle is evidenced by Liberty Energy idling two fleets and experiencing margin compression due to pricing concessions. Seasonal improvements are anticipated in the first half of 2025, although exploration and production companies are expected to persist in seeking pricing concessions amidst oil price uncertainties. A more rapid decline in EBITDA compared to capital expenditures has led to a reduced free cash flow estimate for Liberty in 2025, which suggests a modest yield at the present stock price. Furthermore, with the first quarter facing seasonal working capital challenges, the company's capacity to repurchase shares may be constrained in the near term without resorting to leveraging its balance sheet.

Liberty Energy's reported EBITDA fell short of expectations, indicating a subdued forecast for frac activity and pricing towards the end of 2024. Despite a less optimistic view on the company's second half outlook and its lowered free cash flow profile, the anticipated update on Liberty Power Innovations in early 2025 is seen as a potential catalyst for the company's stock.

Liberty Energy's Q4 guidance and comments indicating price headwinds were described as 'lackluster.' Nonetheless, expectations are set for enhanced performance in the first half of 2025 after a seasonal decrease in Q4.

Here are the latest investment ratings and price targets for $Liberty Energy (LBRT.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間10月21日,多家華爾街大行更新了$Liberty Energy (LBRT.US)$的評級,目標價介於18美元至21美元。

美銀證券分析師Saurabh Pant維持持有評級,並將目標價從21.5美元下調至18美元。

花旗分析師Scott Gruber維持持有評級,維持目標價19美元。

巴克萊銀行分析師Eddie Kim維持買入評級,維持目標價21美元。

巴克萊銀行分析師Eddie Kim維持買入評級,維持目標價21美元。

Seaport Global分析師Tom Curran維持持有評級。

此外,綜合報道,$Liberty Energy (LBRT.US)$近期主要分析師觀點如下:

板塊中的定價挑戰已擴展到一線泵商和設備上,這反映在liberty energy對「放緩的活動對定價造成的不穩定壓力,與[其]預期的未來需求不一致」的認識中。預計liberty的實現定價可能會在改善之前面臨進一步的走弱。

Liberty Energy度過了艱難的一個季度,Q3的EBITDA預期下降了5%,並預測Q4的業績將低於共識25%。這導致管理層在投資者中失去了一些信譽。

通過liberty energy閒置兩個車隊和因定價讓步導致的邊際擠壓,下行週期的加劇得到了證明。預計2025年上半年會有季節性改善,儘管勘探和生產公司預計會在石油價格不確定性下繼續尋求定價讓步。與資本支出相比,EBITDA的更快下降導致2025年liberty的自由現金流預估降低,這表明目前股價具有一定的收益率。此外,隨着第一季度面臨季節性營運資金挑戰,公司回購股份的能力可能在短期內受到限制,而無需藉助其資產負債表的槓桿。

liberty energy報告的EBITDA低於預期,表明2024年末對板塊活動和定價的預測疲軟。儘管對公司下半年展望更爲悲觀,並且自由現金流狀況下調,但預計2025年初liberty power innovations的最新消息被視爲公司股份的潛在催化劑。

liberty energy的Q4指引和表明價格阻力的評論被描述爲「平淡無奇」。儘管如此,人們預期在Q4後的季節性下降之後,2025年上半年會有業績表現提升。

以下爲今日4位分析師對$Liberty Energy (LBRT.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。