本报告研究对象是2023年供应链计划及APS解决方案市场。该市场中,全球厂商供应链计划和APS两层的产品形态相对清晰,例如,Blue Yonder的Luminate Planning、SAP的IBP(Integrated Business Planning)为供应链计划解决方案;SAP PP/DS(Production Planning and Detailed Scheduling)、西门子Opcenter APS、Asprova APS则是聚焦生产制造层面的APS解决方案。

本报告研究对象是2023年供应链计划及APS解决方案市场。该市场中,全球厂商供应链计划和APS两层的产品形态相对清晰,例如,Blue Yonder的Luminate Planning、SAP的IBP(Integrated Business Planning)为供应链计划解决方案;SAP PP/DS(Production Planning and Detailed Scheduling)、西门子Opcenter APS、Asprova APS则是聚焦生产制造层面的APS解决方案。報告數據顯示,2023 年中國供應鏈計劃及APS解決方案件市場(不含硬件收入)總規模達到17.6 億元人民幣,年增長率爲29.2%,仍然是核心工業軟件中增速最高的市場。

智通財經APP獲悉,IDC發佈報告針對2023年中國供應鏈計劃及APS市場的規模、增長速度、主要玩家、市場與技術的發展趨勢等內容進行了詳細研究。報告數據顯示,2023 年中國供應鏈計劃及APS解決方案件市場(不含硬件收入)總規模達到17.6 億元人民幣,年增長率爲29.2%,仍然是核心工業軟件中增速最高的市場。

保持較高增速的主要影響因素是中國市場供應鏈計劃需求持續釋放,市場供給能力也在持續提升,較低的滲透率和市場基數也是其前提條件。IDC預測,該市場未來幾年仍會保持較高增長速度,但市場格局尚未固化,處於早期跑馬圈地階段。

本報告研究對象是2023年供應鏈計劃及APS解決方案市場。該市場中,全球廠商供應鏈計劃和APS兩層的產品形態相對清晰,例如,Blue Yonder的Luminate Planning、SAP的IBP(Integrated Business Planning)爲供應鏈計劃解決方案;SAP PP/DS(Production Planning and Detailed Scheduling)、西門子Opcenter APS、Asprova APS則是聚焦生產製造層面的APS解決方案。

本報告研究對象是2023年供應鏈計劃及APS解決方案市場。該市場中,全球廠商供應鏈計劃和APS兩層的產品形態相對清晰,例如,Blue Yonder的Luminate Planning、SAP的IBP(Integrated Business Planning)爲供應鏈計劃解決方案;SAP PP/DS(Production Planning and Detailed Scheduling)、西門子Opcenter APS、Asprova APS則是聚焦生產製造層面的APS解決方案。

中國市場本土廠商市場定位及產品形態仍在迭代進化中,悠樺林、漢得信息、杉數科技提供包括供應鏈計劃及APS在內的一體化解決方案,金蝶、藍幸專注於供應鏈計劃層,美雲智數則聚焦在生產製造層的APS。供應鏈層和製造層計劃相互覆蓋、深度相關,產品邊界正在逐漸模糊,一體化的整體解決方案是正在發生的趨勢,基於此現狀和趨勢,本次研究目標包括這兩部分在內的整體解決方案市場。

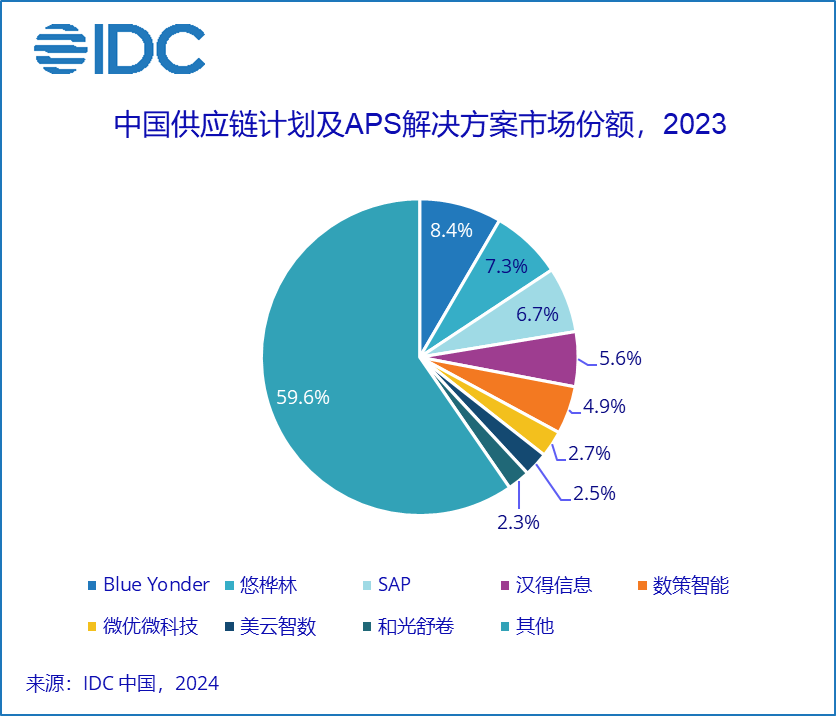

從競爭格局來看,Blue Yonder、悠樺林和SAP在2023年中國供應鏈計劃及APS解決方案市場排名前三。其中,Blue Yonder延續其在中國市場的良好口碑以及高科技電子行業解決方案的深厚積累,以8.4%的市場份額排名第一;悠樺林憑藉其在新能源、家電、食品飲料、裝備製造、整車及零部件等多個行業的探索和積累,以7.3%的市場份額排名第二,與去年相比上升一位;SAP憑藉其最廣泛的客戶群,提供從企業資源管理到供應鏈計劃的端到端集成方案,以6.7%的市場份額排名第三。

漢得信息(300170.SZ)、數策智能、微優微科技、美雲智數、和光舒捲分列第四到第八。其他典型服務商達索系統、杉數科技、西門子、金蝶(00268)、藍幸、谷鬥、o9、永凱、第四範式(06682)、創新奇智(02121)、商簡、不工、清智優化等都在各自領域有不錯的表現。

IDC報告指出, 2023年主要市場變化包括雲廠商或重塑工業軟件生態,IPO收緊,融資困難,併購機會出現等。IDC在報告中建議,技術服務商應重點關注顧問稀缺問題、紮實交付每一個項目、向高價值的供應鏈計劃端延伸等趨勢。

IDC中國製造行業高級研究經理杜雁澤表示,IDC將供應鏈計劃及APS定位成繼ERP、MES、PLM之後,中國製造和零售企業必備的數字化「第四件套」,是企業業務規模化之後持續健康增長的重要支撐。隨着製造企業業務瓶頸從工廠內部向供應鏈端轉移,市場機會在顯著變多,但廠商感受卻兩極分化:在APS生產端排產方向競爭白熱化,在價值和客單價更高的供應鏈計劃端高質量供給卻供不應求。儘管優秀顧問匱乏、客戶數據基礎薄弱、供需方認知不匹配等挑戰仍然存在,但該市場仍然以近三成的年增速快速成長,整體市場未來可期。