Those Who Invested in Pool (NASDAQ:POOL) Five Years Ago Are up 95%

Those Who Invested in Pool (NASDAQ:POOL) Five Years Ago Are up 95%

Over half a decade, Pool managed to grow its earnings per share at 14% a year. So the EPS growth rate is rather close to the annualized share price gain of 13% per year. Therefore one could conclude that sentiment towards the shares hasn't morphed very much. In fact, the share price seems to largely reflect the EPS growth.

Over half a decade, Pool managed to grow its earnings per share at 14% a year. So the EPS growth rate is rather close to the annualized share price gain of 13% per year. Therefore one could conclude that sentiment towards the shares hasn't morphed very much. In fact, the share price seems to largely reflect the EPS growth. The main point of investing for the long term is to make money. Furthermore, you'd generally like to see the share price rise faster than the market. But Pool Corporation (NASDAQ:POOL) has fallen short of that second goal, with a share price rise of 85% over five years, which is below the market return. Over the last twelve months the stock price has risen a very respectable 15%.

長期投資的主要目的是賺錢。此外,您通常希望看到股價比市場漲得更快。但是 Pool Corporation(納斯達克:POOL)在第二個目標上表現不佳,股價在五年內上漲了85%,低於市場回報。過去十二個月,股價上漲了非常可觀的15%。

Now it's worth having a look at the company's fundamentals too, because that will help us determine if the long term shareholder return has matched the performance of the underlying business.

現在值得更詳細地了解該公司的基本面,因爲這將幫助我們判斷長期股東回報是否與基礎業務的表現相匹配。

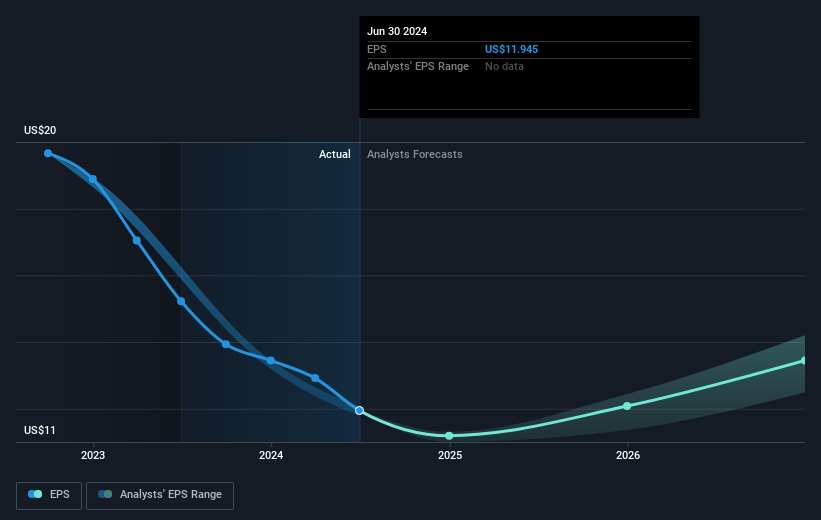

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

用本傑明·格雷厄姆的話來說:「短期市場是一臺投票機,但長期市場是一臺稱重機」。檢查市場情緒如何隨時間推移變化的一種方式是查看公司股價和每股收益(EPS)之間的相互作用。

Over half a decade, Pool managed to grow its earnings per share at 14% a year. So the EPS growth rate is rather close to the annualized share price gain of 13% per year. Therefore one could conclude that sentiment towards the shares hasn't morphed very much. In fact, the share price seems to largely reflect the EPS growth.

在半個多世紀時間裏,Pool 設法將每股收益年增長率提高到14%。因此,每股收益增長率與年化股價增幅13%非常接近。因此,人們可以得出結論,對股票的情緒變化並不大。事實上,股價似乎在很大程度上反映了每股收益的增長。

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

下圖顯示了EPS隨時間變化的情況(點擊圖像以顯示確切值)。

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. It might be well worthwhile taking a look at our free report on Pool's earnings, revenue and cash flow.

值得一提的是,這位CEO的薪酬低於類似規模公司的中位數。但雖然CEO的報酬值得關注,真正重要的問題是公司未來是否能夠增長收益。查看Pool的收益、營業收入和現金流的免費報告可能非常值得一看。

What About Dividends?

那麼分紅怎麼樣呢?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Pool the TSR over the last 5 years was 95%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

考慮任何給定股票的總股東回報以及股價回報是很重要的。TSR是一個計算回報的方法,考慮了現金分紅的價值(假設收到的任何股息都被再投資)以及任何減價增資和剝離計算值。因此,對於支付慷慨分紅的公司,TSR往往比股價回報高得多。我們注意到,Pool過去5年的TSR爲95%,比上面提到的股價回報要好。這在很大程度上是其分紅支付的結果!

A Different Perspective

不同的觀點

Pool shareholders gained a total return of 16% during the year. Unfortunately this falls short of the market return. On the bright side, that's still a gain, and it's actually better than the average return of 14% over half a decade This could indicate that the company is winning over new investors, as it pursues its strategy. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for Pool you should know about.

Pool股東在該年度獲得了16%的總回報。不幸的是,這低於市場回報。但好消息是,這仍然是一項收益,實際上比過去半個世紀的平均回報14%更好。這可能表明公司正在贏得新投資者的青睞,因爲它執行其策略。我發現長期以來觀察股價作爲業績代理很有趣。但爲了真正獲得洞察,我們也需要考慮其他信息。例如,考慮風險。每家公司都有風險,我們已經發現Pool有1個警示標誌,您應該知道。

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

如果您願意查看另一家公司(具有潛在的更好財務狀況),請不要錯過這個免費的公司列表,證明它們可以增長收益。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。