Some Johnson Controls International Plc (NYSE:JCI) Analysts Just Made A Major Cut To Next Year's Estimates

Some Johnson Controls International Plc (NYSE:JCI) Analysts Just Made A Major Cut To Next Year's Estimates

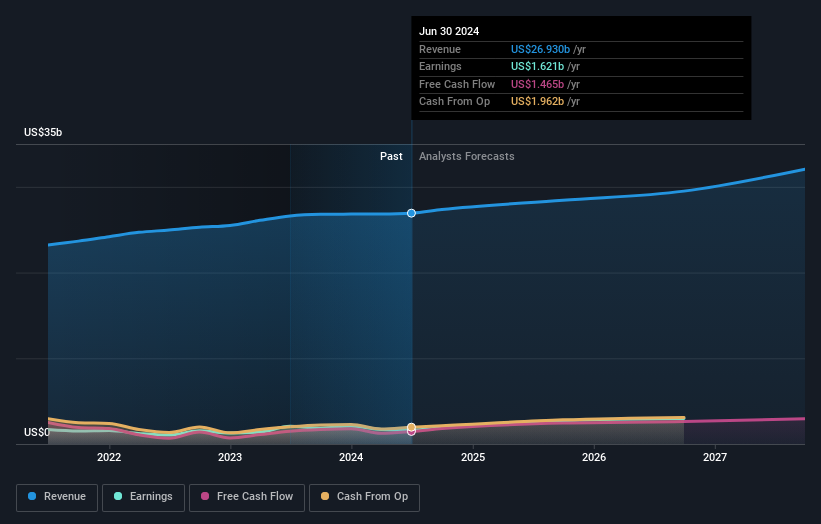

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 7.9% annualised revenue decline to the end of 2025. That is a notable change from historical growth of 3.6% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.3% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Johnson Controls International is expected to lag the wider industry.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 7.9% annualised revenue decline to the end of 2025. That is a notable change from historical growth of 3.6% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.3% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Johnson Controls International is expected to lag the wider industry. The analysts covering Johnson Controls International plc (NYSE:JCI) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for next year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon.

覆蓋江森自控國際股份有限公司(紐交所:JCI)的分析師今天向股東們傳遞了一劑負面情緒,通過對明年財務預測進行了大幅修訂。營業收入和每股收益(EPS)預測均下調,分析師們看到了地平線上的暗雲。

Following the latest downgrade, the current consensus, from the ten analysts covering Johnson Controls International, is for revenues of US$24b in 2025, which would reflect an uneasy 9.7% reduction in Johnson Controls International's sales over the past 12 months. Per-share earnings are expected to bounce 50% to US$3.65. Before this latest update, the analysts had been forecasting revenues of US$29b and earnings per share (EPS) of US$4.18 in 2025. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a real cut to earnings per share numbers as well.

在最新的下調之後,覆蓋江森自控國際的十位分析師目前普遍預計其2025年營業額爲240億美元,這將反映出江森自控國際在過去12個月銷售額下跌了9.7%。每股收益預計將增長50%,達到3.65美元。在此次最新更新之前,分析師們一直在預測江森自控國際2025年的營業額爲290億美元,每股收益(EPS)爲4.18美元。看起來分析師們的情緒大幅下降,對營收預期有明顯下調,對每股收益數字也有實質性的下調。

Analysts made no major changes to their price target of US$80.87, suggesting the downgrades are not expected to have a long-term impact on Johnson Controls International's valuation.

分析師們沒有對80.87美元的目標股價做出重大變化,這表明預期這些下調不會對江森自控國際的估值產生長期影響。

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 7.9% annualised revenue decline to the end of 2025. That is a notable change from historical growth of 3.6% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.3% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Johnson Controls International is expected to lag the wider industry.

現在來看更大的畫面,我們可以通過將這些預測與過去表現和行業增長預期進行對比來理解。我們將強調銷售預計將出現逆轉,預計到2025年底將出現7.9%的年化營收下降。這與過去五年的3.6%歷史增長形成了明顯的變化。將此與我們的數據進行對比,數據顯示同行業的其他公司預計年均營收增長5.3%。因此,儘管其營收預計將下降,但這片烏雲並沒有銀膜——預計江森自控國際將落後於更廣泛的行業。

The Bottom Line

最重要的事情是分析師增加了它對下一年每股虧損的估計。令人欣慰的是,營收預測未發生重大變化,業務仍有望比整個行業增長更快。共識價格目標穩定在28.50美元,最新估計不足以對價格目標產生影響。

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Johnson Controls International's revenues are expected to grow slower than the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on Johnson Controls International after the downgrade.

最重要的一點是,分析師削減了每股收益的預期,預計業務狀況將明顯下滑。不幸的是,分析師還下調了他們的營業收入預期,而行業數據顯示,預計江森自控的營業收入增速將低於整個市場。我們也很驚訝地看到,價格目標保持不變。然而,業務狀況惡化(假設預測準確!)可能是股價的領先指標,因此我們不會因爲降級後的江森自控而對投資者更加謹慎而責怪他們。

There might be good reason for analyst bearishness towards Johnson Controls International, like recent substantial insider selling. Learn more, and discover the 3 other risks we've identified, for free on our platform here.

分析師對江森自控可能持悲觀態度,比如最近大量內部人士的賣出行爲等。在我們的平台上免費了解更多,並發現我們已經確定的其他3個風險。

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

當然,看到公司管理層投入大量資金投資股票的情況與分析師是否對其評級下調一樣有用。因此,您還可以搜索此處的高內部所有權股票的免費列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。