Those holding Huize Holding Limited (NASDAQ:HUIZ) shares would be relieved that the share price has rebounded 28% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 25% in the last twelve months.

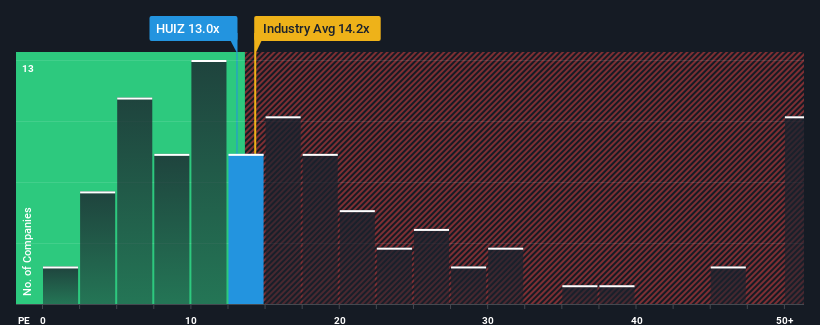

Although its price has surged higher, given about half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may still consider Huize Holding as an attractive investment with its 13x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

As an illustration, earnings have deteriorated at Huize Holding over the last year, which is not ideal at all. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NasdaqGM:HUIZ Price to Earnings Ratio vs Industry October 17th 2024 Although there are no analyst estimates available for Huize Holding, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

Does Growth Match The Low P/E?

Huize Holding's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Retrospectively, the last year delivered a frustrating 25% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 15% shows it's noticeably less attractive on an annualised basis.

With this information, we can see why Huize Holding is trading at a P/E lower than the market. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Bottom Line On Huize Holding's P/E

The latest share price surge wasn't enough to lift Huize Holding's P/E close to the market median. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Huize Holding maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Huize Holding that you should be aware of.

If these risks are making you reconsider your opinion on Huize Holding, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Huize Holding's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Huize Holding's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

慧擇控股的市盈率對於一家預計僅能提供有限增長,並且重要的是,表現比市場要差的公司來說是典型的。

慧擇控股的市盈率對於一家預計僅能提供有限增長,並且重要的是,表現比市場要差的公司來說是典型的。