由于严厉打击密码共享行为,以及推出价格较低的嵌入广告式流媒体订阅服务,奈飞近几个季度的业绩增速以及用户扩张步伐一直非常强劲。但随着该公司准备在周四美股收盘后公布第三季度业绩,且在业绩公布前奈飞股价持续上涨意味着市场预期也在不断提高,一些分析师担心这些积极的催化剂可能将难以推动奈飞业绩超过市场予以的苛刻预期。

由于严厉打击密码共享行为,以及推出价格较低的嵌入广告式流媒体订阅服务,奈飞近几个季度的业绩增速以及用户扩张步伐一直非常强劲。但随着该公司准备在周四美股收盘后公布第三季度业绩,且在业绩公布前奈飞股价持续上涨意味着市场预期也在不断提高,一些分析师担心这些积极的催化剂可能将难以推动奈飞业绩超过市场予以的苛刻预期。Due to the password crackdown campaign, a new ad support layer has been launched, causing Netflix's stock price to continue to soar, but the average target price from Wall Street analysts implies only a remaining 3% upside for the stock price.

Streaming giant $Netflix (NFLX.US)$ On October 17th, after the U.S. market closes (Friday morning Beijing time), the streaming giant will announce its third-quarter performance up to September. Analysts generally expect the company's revenue and global subscription base to continue expanding. Ahead of the financial report release, the stock price of this streaming giant has surged by nearly 340% since hitting a temporary low in May 2022, reaching an all-time high earlier this month, marking an "epic increase" for the stock, with the current price still hovering near its historical peak.

However, after experiencing a "lightning-fast expansion" that increased its market cap by as much as $230 billion, Wall Street analysts' price expectations indicate that the peak figure of Netflix's stock price may be approaching. According to the institutions' compilation, the average target price of analysts implies that the stock price of this streaming giant in the next 12 months has only 3% upside potential left.

Due to the severe crackdown on password sharing behavior, as well as the introduction of a lower-priced embedded advertising-based streaming subscription service, Netflix's performance growth rate and user expansion pace have been very strong in recent quarters. However, as the company prepares to announce its third-quarter results after the Thursday's US stock market close, and with Netflix's stock price continuing to rise before the financial results are released, indicating that market expectations are also continuously rising, some analysts are concerned that these positive catalysts may struggle to drive Netflix's performance beyond the market's already high expectations.

Due to the severe crackdown on password sharing behavior, as well as the introduction of a lower-priced embedded advertising-based streaming subscription service, Netflix's performance growth rate and user expansion pace have been very strong in recent quarters. However, as the company prepares to announce its third-quarter results after the Thursday's US stock market close, and with Netflix's stock price continuing to rise before the financial results are released, indicating that market expectations are also continuously rising, some analysts are concerned that these positive catalysts may struggle to drive Netflix's performance beyond the market's already high expectations.

Analyst Kannan Venkateswaran from Barclays Bank wrote in a report that Netflix has had a "very impressive" execution period, but it "has to rely more on new growth drivers to maintain double-digit revenue growth rates, some of which, like the paid-share initiatives, may drive future performance growth". However, this analyst recently downgraded the stock rating to "shareholding", stating that investors' expectations for Netflix's revenue growth seem overly optimistic.

Statistical data compiled by institutions shows that after a long rebound, Netflix's stock price is currently less than 3% away from the average target price of analysts for the next 12 months, which means that Wall Street believes the stock will not rise further in the next 12 months. The data shows that this relatively pessimistic expectation ranks it among the bottom 20 stocks in the Nasdaq 100 index component stocks in terms of implied return.

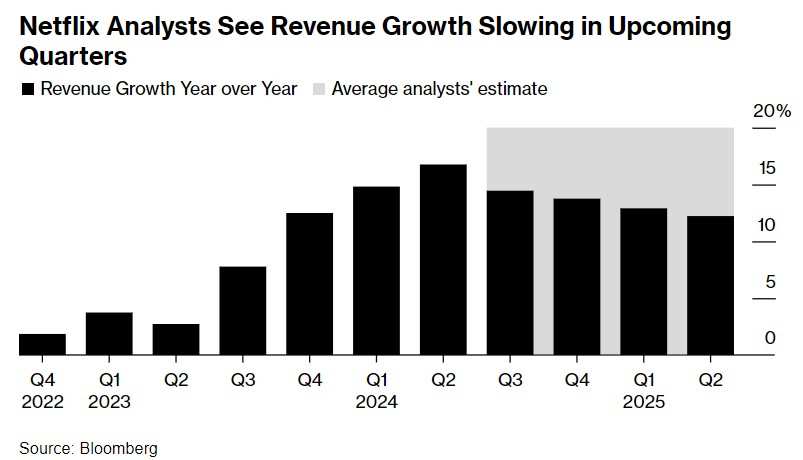

Analysts generally expect Netflix's third-quarter revenue to increase by 14% year-on-year, gradually slowing down in the following three quarters. This latest expectation is lower than the 17% growth rate of the previous quarter. Overall revenue and average revenue per subscriber have become key performance indicators for the company after a shift in the business model to offer multiple pricing tiers.

Meanwhile, analysts widely expect Netflix's global user base to reach 0.286 billion by the end of the third quarter, an increase of about 4 million from the previous quarter and over 300 million from the same period last year. Net income is expected to be $2.23 billion, a 33% year-on-year growth. Netflix had previously announced plans to stop reporting user data starting from 2025 and focus on financial indicators instead.

As Netflix's future revenue growth rate may slow down, the stock may start to appear too expensive to some investors. Netflix's expected PE ratio as high as 32x is higher than the 26x shown by the Nasdaq 100 Index, far exceeding other streaming service providers such as Disney with a 19x valuation and Paramount with only a 7x valuation.

Matthew Maley, Chief Market Strategist at Miller Tabak + Co. LLC., said: "Netflix's valuation does appear very expensive, so if the stock price continues to rise, they will have to increase the 'E' in 'P/E,' meaning the profit part. This implies that Netflix management will need to continue expanding advertising partnerships globally to significantly improve profitability."

According to Wall Street analysts bullish on Netflix stock price, Netflix still has many ways to drive performance growth. The most significant of these is raising subscription prices, especially for standard-tier subscriptions. Since introducing an ad-supported subscription model, Netflix has not raised the price of standard subscriptions for over two years. Expectations of price hikes, along with the continuous expansion of exclusive content libraries and increasing platform users, are driving investor optimism about Netflix's future revenue growth rate, a key expectation for long-term stock price increase.

However, this may alienate subscription customers sensitive to pricing, who have shown a willingness to cut other non-essential expenses such as online food delivery services, some unnecessary home and hobby items.

However, Thomas Martin, a senior portfolio manager at Globalt Investments, stated that Netflix has proven itself to have the most loyal subscriber base in the world, willing to pay more for the streaming service, thanks to many high-quality series like 'Stranger Things.' 'They have a lot of room to increase some subscription tiers and may not lose customers,' Martin said in an interview.

James Slattery, an analyst at Jefferies, agrees with this and maintains a 'buy' rating on the stock. In a report, he wrote, 'It must be acknowledged that Netflix has become a 'value' choice rather than the previously touted 'premium' subscription product.' He particularly points out that streaming competitors like Disney+, HBO Max, and Hulu have more expensive subscription services compared to Netflix.

However, raising prices may occasionally be a performance lever that technology companies rely on. Analyst Jason Bazin from Citigroup believes that Netflix announcing a price increase in the USA could significantly boost the stock price. However, as the market's expectations for Netflix's price increase next year weaken, and optimism about profit and revenue growth rates gradually diminish, the stock price surge may be short-lived. 'As investors' hopes for Netflix's 2025 earnings per share to reach as high as $25 are gradually dashed, we expect the stock price to ultimately decline,' analyst Bazin said.

Editor/Lambor