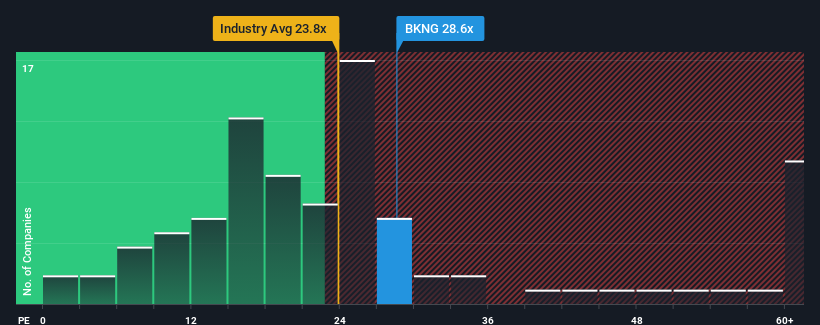

Booking Holdings Inc.'s (NASDAQ:BKNG) price-to-earnings (or "P/E") ratio of 28.6x might make it look like a strong sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times have been pleasing for Booking Holdings as its earnings have risen in spite of the market's earnings going into reverse. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors' willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

NasdaqGS:BKNG Price to Earnings Ratio vs Industry October 11th 2024 Want the full picture on analyst estimates for the company? Then our free report on Booking Holdings will help you uncover what's on the horizon.

Is There Enough Growth For Booking Holdings?

The only time you'd be truly comfortable seeing a P/E as steep as Booking Holdings' is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered an exceptional 24% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 1,385% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 19% per annum as estimated by the analysts watching the company. That's shaping up to be materially higher than the 10% each year growth forecast for the broader market.

With this information, we can see why Booking Holdings is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Booking Holdings' P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Booking Holdings maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Booking Holdings that you should be aware of.

If you're unsure about the strength of Booking Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 24% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 1,385% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Retrospectively, the last year delivered an exceptional 24% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 1,385% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

回顧過去一年爲公司的底線帶來了異常的24%增長。最近強勁的業績也意味着在過去三年裏EPS總計增長了1,385%。因此,股東們可能會對這些中期盈利增長率表示歡迎。

回顧過去一年爲公司的底線帶來了異常的24%增長。最近強勁的業績也意味着在過去三年裏EPS總計增長了1,385%。因此,股東們可能會對這些中期盈利增長率表示歡迎。