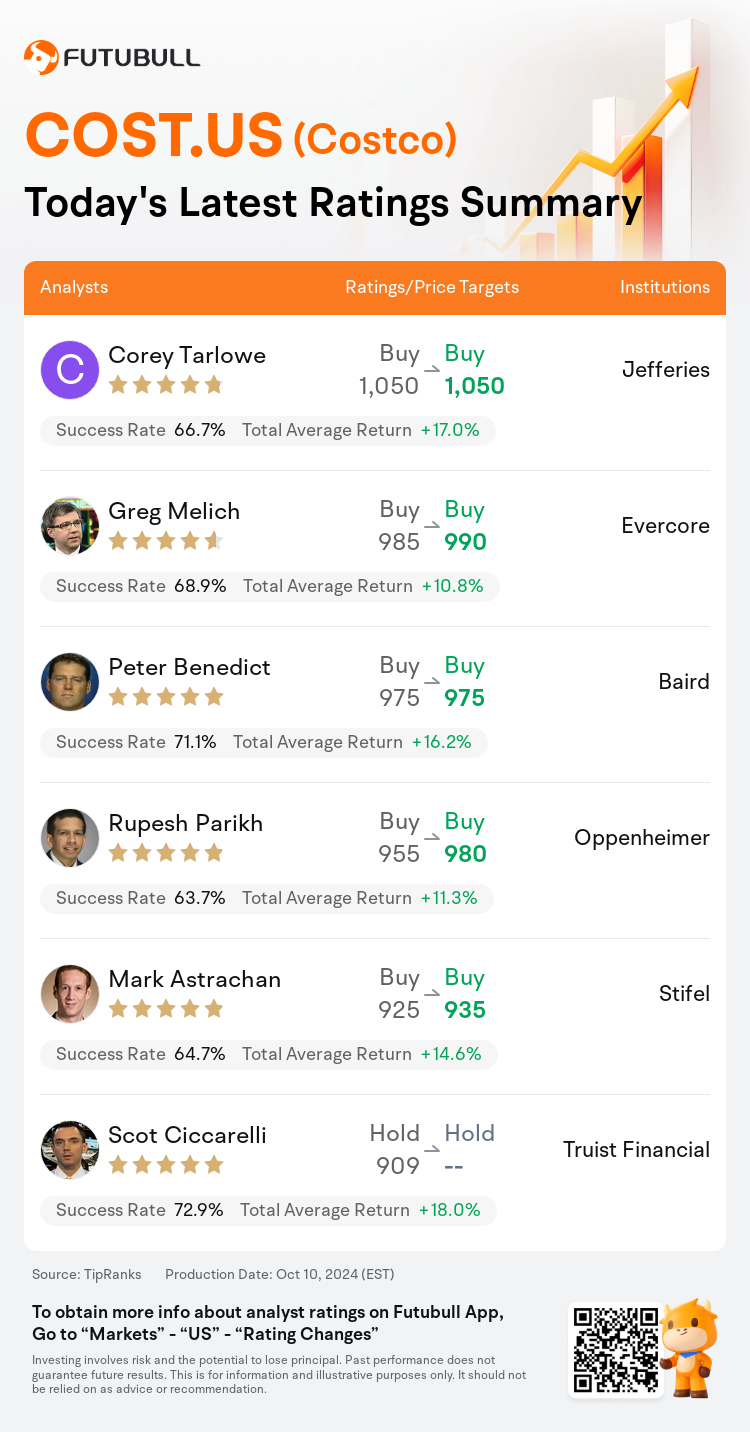

On Oct 10, major Wall Street analysts update their ratings for $Costco (COST.US)$, with price targets ranging from $935 to $1,050.

Jefferies analyst Corey Tarlowe maintains with a buy rating, and maintains the target price at $1,050.

Evercore analyst Greg Melich maintains with a buy rating, and adjusts the target price from $985 to $990.

Baird analyst Peter Benedict maintains with a buy rating, and maintains the target price at $975.

Baird analyst Peter Benedict maintains with a buy rating, and maintains the target price at $975.

Oppenheimer analyst Rupesh Parikh maintains with a buy rating, and adjusts the target price from $955 to $980.

Stifel analyst Mark Astrachan maintains with a buy rating, and adjusts the target price from $925 to $935.

Furthermore, according to the comprehensive report, the opinions of $Costco (COST.US)$'s main analysts recently are as follows:

Costco's U.S. and Global Core comparable sales growth of 9% in September demonstrates the company's capacity to attract members with its exceptional value, diverse product offerings, and convenience across multiple channels. Even after accounting for an approximate 200 basis point increase in U.S. sales attributed to Hurricane Helene and port strikes, the core growth of over 7% continues to outpace the broader U.S. retail sales figures significantly.

Costco's September adjusted U.S. comparable sales showed a 9.3% increase, attributed in part to an approximate 2 percentage point rise from unusual consumer behavior due to port strikes and Hurricane Helene. These figures align with positive observations during store evaluations. Notably, non-food categories have continued to perform well, particularly jewelry and gift cards, increasing in the low double-digit range. It is anticipated that Costco's robust top-line growth will continue throughout the year, supported by their exceptional merchandising capabilities and distinct value proposition. Additionally, it's suggested that Costco may experience a short-term increase in memberships as a result of more rigorous checks at the point of membership card verification.

Costco's total and U.S. core September comparable sales growth was reported at 8.9% and 7.3%, which include benefits from circumstances such as Hurricane Helene and port strikes, surpassing the consensus predictions of 6.2% and 5.9%. The company's traffic growth was robust, increasing by 7.2% globally and 7.6% in the U.S. This suggests that Costco's value proposition is effectively attracting customers, promoting frequent shopping visits, and gaining market share.

Here are the latest investment ratings and price targets for $Costco (COST.US)$ from 6 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

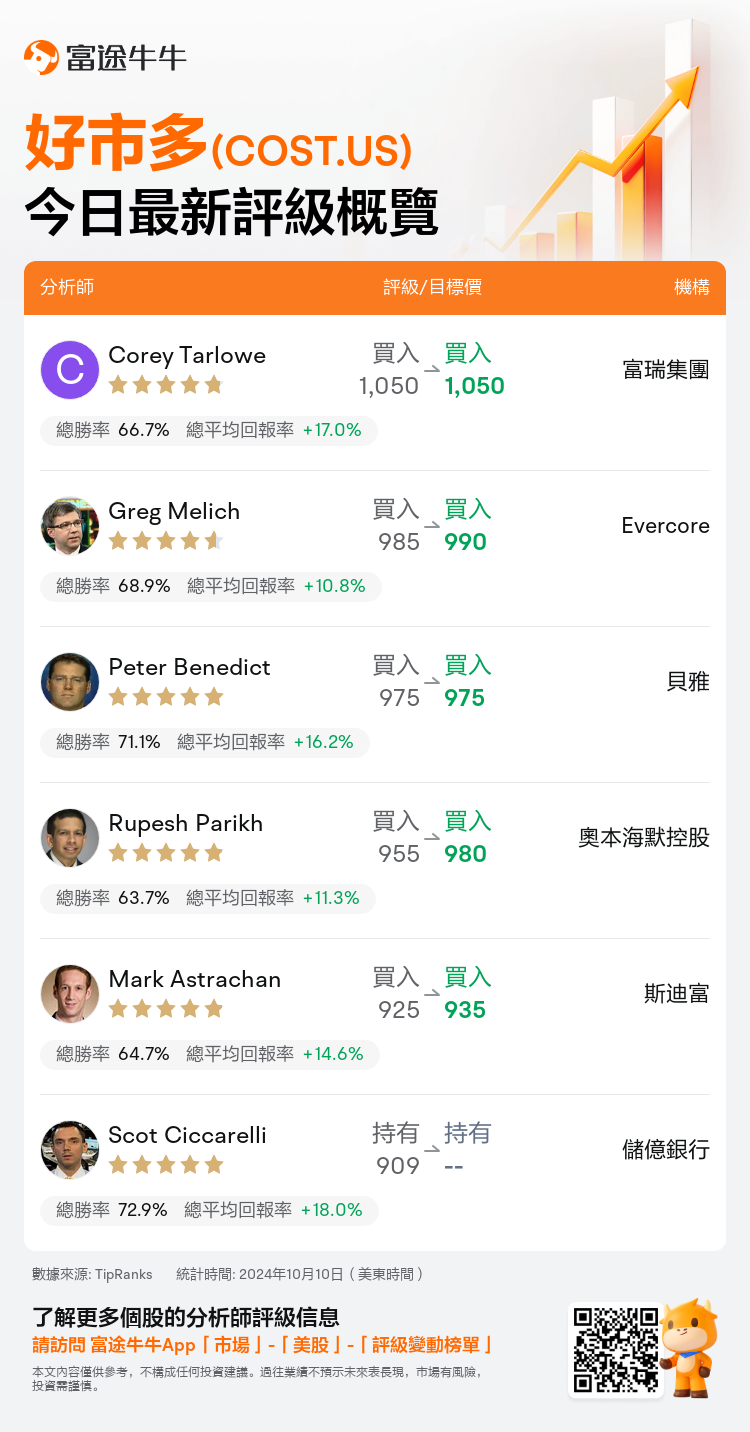

美東時間10月10日,多家華爾街大行更新了$好市多 (COST.US)$的評級,目標價介於935美元至1,050美元。

富瑞集團分析師Corey Tarlowe維持買入評級,維持目標價1,050美元。

Evercore分析師Greg Melich維持買入評級,並將目標價從985美元上調至990美元。

貝雅分析師Peter Benedict維持買入評級,維持目標價975美元。

貝雅分析師Peter Benedict維持買入評級,維持目標價975美元。

奧本海默控股分析師Rupesh Parikh維持買入評級,並將目標價從955美元上調至980美元。

斯迪富分析師Mark Astrachan維持買入評級,並將目標價從925美元上調至935美元。

此外,綜合報道,$好市多 (COST.US)$近期主要分析師觀點如下:

好市多在9月份的全美和全球核心可比銷售增長了9%,展示了公司吸引會員的能力,其獨特價值、多樣的產品選擇和跨多渠道方便性。即使考慮到由於颶風海倫和港口罷工而導致的美國銷售增長約200個點子,仍然超過7%的核心增長繼續明顯領先於更廣泛的美國零售銷售數據。

好市多9月份調整後的美國可比銷售增長率顯示爲9.3%,部分歸因於非正常消費行爲導致的約2個百分點增長,其中包括港口罷工和颶風海倫。這些數字與店鋪評估期間的積極觀察相符。值得注意的是,非食品類別持續表現良好,尤其是珠寶和禮品卡,增幅在低兩位數範圍內。預計好市多強勁的頂線增長將在全年持續,得益於其出色的商品陳列能力和獨特的價值主張。此外,有人認爲好市多可能會在會員卡驗證點進行更嚴格的檢查,導致會員數短期增加。

好市多9月份的總體和美國核心可比銷售增長率分別爲8.9%和7.3%,其中包括來自颶風海倫和港口罷工等情況的利益,超過了6.2%和5.9%的共識預測。公司的客流量增長強勁,全球增長率爲7.2%,美國爲7.6%。這表明好市多的價值主張有效吸引顧客,促進頻繁購物,並獲得市場份額。

以下爲今日6位分析師對$好市多 (COST.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。