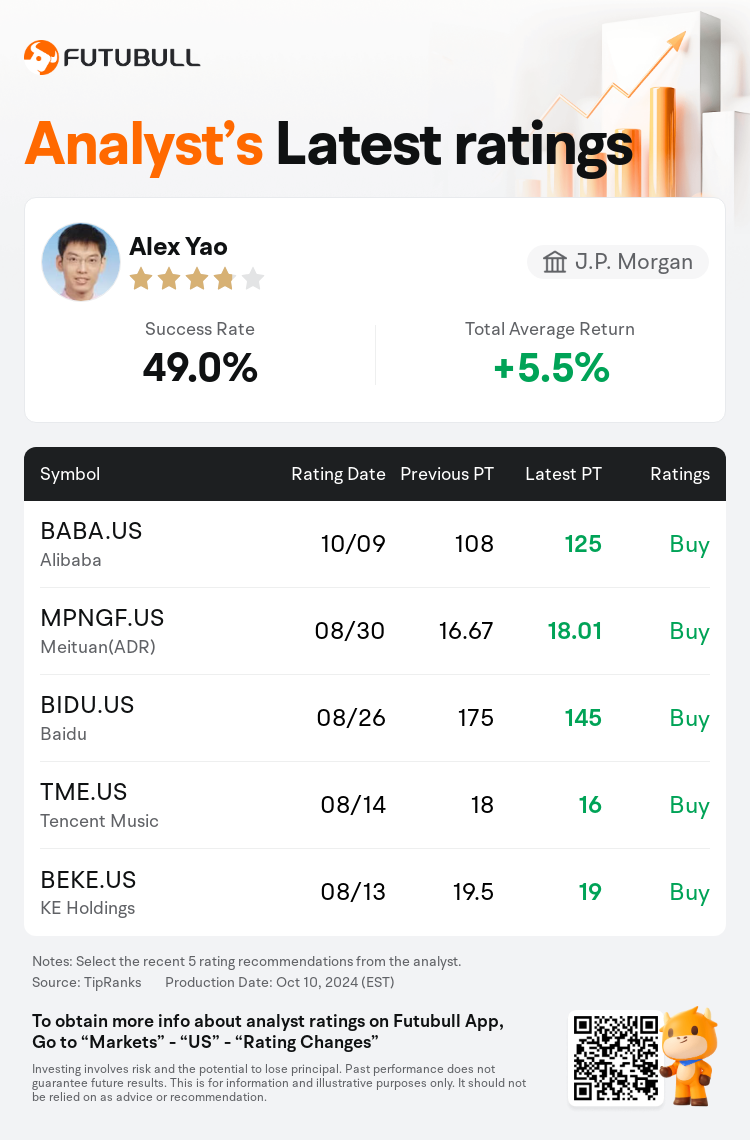

J.P. Morgan analyst Alex Yao maintains $Alibaba (BABA.US)$ with a buy rating, and adjusts the target price from $108 to $125.

According to TipRanks data, the analyst has a success rate of 49.0% and a total average return of 5.5% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Alibaba (BABA.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Alibaba (BABA.US)$'s main analysts recently are as follows:

Expectations are set for Alibaba to unveil its fiscal Q2 results in the early to mid-November period, with projections indicating a 6% annual increase in total revenue. It's anticipated that the core revenue from Taobao and Tmall will remain relatively unchanged from the previous year. The forecast also suggests a modest 1.8% year-over-year rise in customer management revenue from the China marketplaces, predicated on a mid-single digit percentage growth in gross merchandise value, or GMV, coupled with a slightly reduced blended take rate.

The firm maintains a cautious stance on Alibaba, influenced by subdued consumer spending and ongoing reinvestments that are expected to impact earnings. The anticipation is for the Gross Merchandise Value to rise by 4%-5% year over year, compared to the higher single digits seen in the first quarter. Additionally, projections include an acceleration of customer management revenue growth to 2%-3%, up from 0.6% in the previous quarter, potentially supported by software service fees.

Expectations are set for Alibaba's fiscal second quarter revenue and profit at its core platforms, Taobao and Tmall, to be challenged by a subdued consumption climate. However, it is suggested that investors look past these results in anticipation of forthcoming positive catalysts. Comparing the forward price-to-earnings multiples of the 'big 3' China e-commerce companies—Alibaba, PDD Holdings, and JD.com—Alibaba is viewed as the most promising of the trio.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

摩根大通分析師Alex Yao維持$阿里巴巴 (BABA.US)$買入評級,並將目標價從108美元上調至125美元。

根據TipRanks數據顯示,該分析師近一年總勝率為49.0%,總平均回報率為5.5%。

此外,綜合報道,$阿里巴巴 (BABA.US)$近期主要分析師觀點如下:

此外,綜合報道,$阿里巴巴 (BABA.US)$近期主要分析師觀點如下:

預計阿里巴巴將在11月初至中旬公佈其第二財季業績,預計總收入每年增長6%。預計淘寶和天貓的核心收入將與去年相比相對保持不變。該預測還表明,中國市場的客戶管理收入同比略有增長1.8%,前提是商品總值(GMV)的中等個位數百分比增長,加上混合收入略有下降。

受消費者支出疲軟和預計將影響收益的持續再投資的影響,該公司對阿里巴巴保持謹慎立場。預計商品總價值將同比增長4%-5%,而第一季度的個位數更高。此外,預測還包括客戶管理收入增長從上一季度的0.6%加速至2%-3%,這可能受到軟件服務費的支持。

預計阿里巴巴第二財季的收入和利潤將受到消費環境疲軟的挑戰,淘寶和天貓等核心平台的收入和利潤將受到挑戰。但是,有人認爲,投資者可以忽略這些業績,期待即將到來的積極催化劑。比較 「三大」 中國電子商務公司——阿里巴巴、PDD控股和京東的遠期市盈倍數——阿里巴巴被視爲這三家公司中最有前途的一家。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。