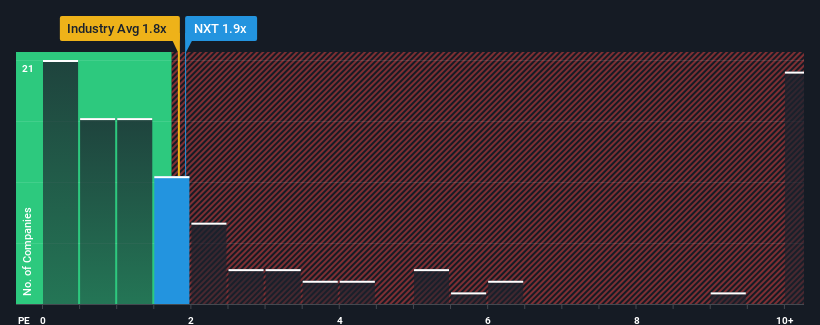

There wouldn't be many who think Nextracker Inc.'s (NASDAQ:NXT) price-to-sales (or "P/S") ratio of 1.9x is worth a mention when the median P/S for the Electrical industry in the United States is similar at about 1.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

NasdaqGS:NXT Price to Sales Ratio vs Industry October 6th 2024

What Does Nextracker's Recent Performance Look Like?

Nextracker certainly has been doing a good job lately as it's been growing revenue more than most other companies. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Nextracker.

Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Nextracker's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 39%. Pleasingly, revenue has also lifted 121% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 9.4% each year during the coming three years according to the analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 18% per annum, which is noticeably more attractive.

With this information, we find it interesting that Nextracker is trading at a fairly similar P/S compared to the industry. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

When you consider that Nextracker's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Nextracker with six simple checks on some of these key factors.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue growth, the company posted a terrific increase of 39%. Pleasingly, revenue has also lifted 121% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

If we review the last year of revenue growth, the company posted a terrific increase of 39%. Pleasingly, revenue has also lifted 121% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

如果我們回顧過去一年的營業收入增長,公司實現了驚人的39%增長。令人高興的是,營業收入也比三年前整體增長了121%,這要歸功於過去12個月的增長。因此,可以說公司最近的營業收入增長表現非常出色。

如果我們回顧過去一年的營業收入增長,公司實現了驚人的39%增長。令人高興的是,營業收入也比三年前整體增長了121%,這要歸功於過去12個月的增長。因此,可以說公司最近的營業收入增長表現非常出色。