Here's Why TE Connectivity (NYSE:TEL) Has Caught The Eye Of Investors

Here's Why TE Connectivity (NYSE:TEL) Has Caught The Eye Of Investors

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While TE Connectivity may have maintained EBIT margins over the last year, revenue has fallen. Suffice it to say that is not a great sign of growth.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While TE Connectivity may have maintained EBIT margins over the last year, revenue has fallen. Suffice it to say that is not a great sign of growth. It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

許多投資者,特別是那些沒有經驗的投資者,通常會買入那些有好故事的公司的股票,即使這些公司虧損。有時這些故事會矇蔽投資者的頭腦,導致他們基於情感而非公司基本面的價值進行投資。虧損公司總是在爭分奪秒地努力達成財務可持續性,因此投資這些公司的投資者可能承擔了比他們應承擔的更多風險。

In contrast to all that, many investors prefer to focus on companies like TE Connectivity (NYSE:TEL), which has not only revenues, but also profits. While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

與這些相比,許多投資者更喜歡關注像是泰科電子(紐交所:TEL)這樣不僅有營業收入,而且有利潤的公司。雖然這並不一定意味着它被低估,但業務的盈利能力足以引起一些讚賞 - 尤其是如果它正在增長。

TE Connectivity's Earnings Per Share Are Growing

TE Connectivity的每股收益正在增長

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That makes EPS growth an attractive quality for any company. Impressively, TE Connectivity has grown EPS by 30% per year, compound, in the last three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

如果你相信市場甚至稍有效率,那麼從長期來看,你會期待公司的股價跟隨其每股收益(EPS)的表現。這使得EPS增長對於任何公司來說都是一種吸引力。令人印象深刻的是,泰科電子在過去三年中以每年30%的複合增長率增長了EPS。如果這樣的增長持續到未來,那麼股東將有很多值得高興的事。

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While TE Connectivity may have maintained EBIT margins over the last year, revenue has fallen. Suffice it to say that is not a great sign of growth.

認真考慮營業收入增長和利潤前利息和稅前利潤(EBIT)利潤率可以幫助了解最近利潤增長的可持續性。雖然泰科電子可能在過去一年裏保持了EBIT利潤率,但營業收入卻有所下降。可以說這並不是增長的好跡象。

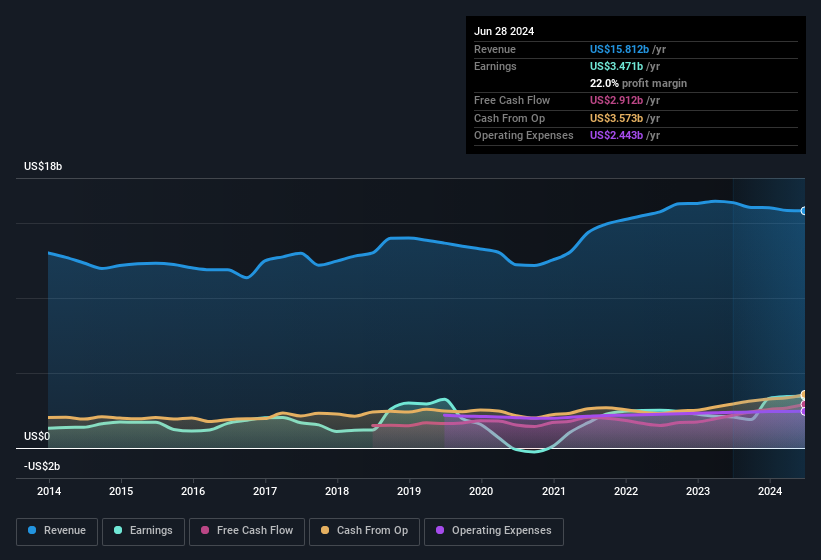

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

下面的圖表顯示了公司的營業收入和收益是如何隨時間變化的。要查看實際數字,請單擊圖表。

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for TE Connectivity's future profits.

你不會開車盯着後視鏡,所以你可能更感興趣的是這份免費報告,顯示了對泰科電子未來利潤的分析師預測。

Are TE Connectivity Insiders Aligned With All Shareholders?

TE Connectivity的內部人是否與所有股東保持一致?

We would not expect to see insiders owning a large percentage of a US$46b company like TE Connectivity. But we do take comfort from the fact that they are investors in the company. Holding US$72m worth of stock in the company is no laughing matter and insiders will be committed in delivering the best outcomes for shareholders. This should keep them focused on creating long term value for shareholders.

我們不會指望內部持有像泰科電子這樣價值460億美元的公司中很大比例的股份。但他們是公司的投資者這一事實讓我們感到安心。持有公司價值7200萬美元的股票絕非鬧着玩的事情,內部持有者將致力於爲股東帶來最佳業績。這應該讓他們專注於爲股東創造長期價值。

Does TE Connectivity Deserve A Spot On Your Watchlist?

TE Connectivity是否值得加入您的自選?

If you believe that share price follows earnings per share you should definitely be delving further into TE Connectivity's strong EPS growth. Further, the high level of insider ownership is impressive and suggests that the management appreciates the EPS growth and has faith in TE Connectivity's continuing strength. Fast growth and confident insiders should be enough to warrant further research, so it would seem that it's a good stock to follow. You still need to take note of risks, for example - TE Connectivity has 1 warning sign we think you should be aware of.

如果你相信股價會跟隨每股收益走勢,那麼你一定要深入研究泰科電子強勁的每股收益增長。此外,高比例的內部持股令人印象深刻,並表明管理層重視每股收益增長,並對泰科電子持續的實力表示信心。快速增長和自信的內部持有者足以值得進一步研究,因此看起來這是一支值得關注的好股票。你仍需要注意風險,例如- 泰科電子有1個我們認爲你應該注意的警告信號。

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a tailored list of companies which have demonstrated growth backed by significant insider holdings.

總是有可能買入未增長收益並且內部人員不買入股票的股票表現良好。但是對於那些認爲這些重要指數的人,我們鼓勵您查看具有這些功能的公司。您可以訪問定製列表,其中列出了已經展示出增長並得到內幕人員認可的公司。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文討論的內部交易是指在相關司法管轄區中報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。