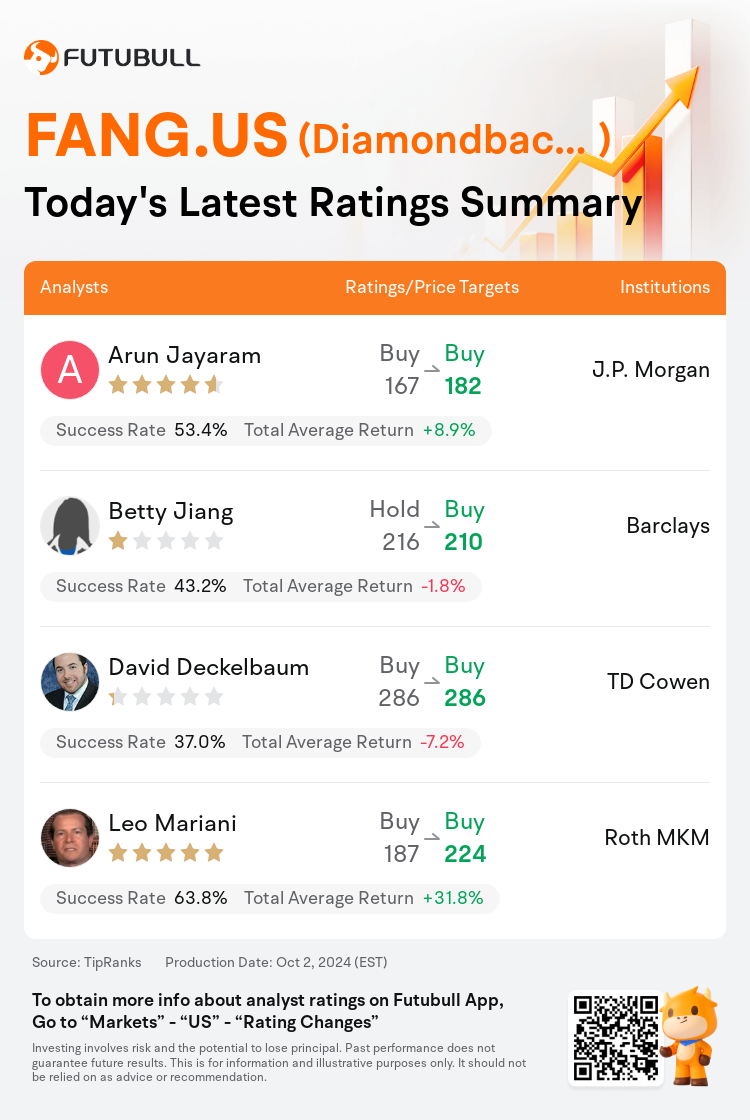

On Oct 02, major Wall Street analysts update their ratings for $Diamondback Energy (FANG.US)$, with price targets ranging from $182 to $286.

J.P. Morgan analyst Arun Jayaram maintains with a buy rating, and adjusts the target price from $167 to $182.

Barclays analyst Betty Jiang upgrades to a buy rating, and adjusts the target price from $216 to $210.

TD Cowen analyst David Deckelbaum maintains with a buy rating, and maintains the target price at $286.

TD Cowen analyst David Deckelbaum maintains with a buy rating, and maintains the target price at $286.

Roth MKM analyst Leo Mariani maintains with a buy rating, and adjusts the target price from $187 to $224.

Furthermore, according to the comprehensive report, the opinions of $Diamondback Energy (FANG.US)$'s main analysts recently are as follows:

In an oil macro environment that may remain challenged in the near term due to the pending return of OPEC+ barrels, Diamondback Energy is positioned as a relative outperformer. This is attributed to its advantageous placement at the low end of the cost curve in the Midland Basin, which enables dividend coverage below $45 per barrel.

Diamondback Energy is perceived to have one of the most promising sequences of positive events in the upcoming quarters with the complete integration of Endeavor. It is anticipated that the company will announce a 2025 program that will surpass initial capital efficiency estimates. The recent decrease in share price, partly due to liquidity events from Endeavor sellers, is seen as an opportune moment for investors to consider entering the market.

Adjustments in the exploration and production sector's estimates reflect revised commodity price assumptions and the investment landscape. The belief is that if operational efficiency improvements continue and service expenses decrease further, exploration and production companies could maintain enhanced capital efficiency through 2025, potentially counteracting the effects of resource maturity.

Amid a global trend of monetary easing, there's a possibility that energy commodities and related equities may not participate due to challenging fundamentals and a potential imbalance projected for 2025. Nevertheless, it's suggested not to go against the central banks' policies, indicating that there may be more positive than negative risks in the crude oil market. As the quarter concludes, it is anticipated that forthcoming updates may reveal lower than expected near-term estimates.

Here are the latest investment ratings and price targets for $Diamondback Energy (FANG.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

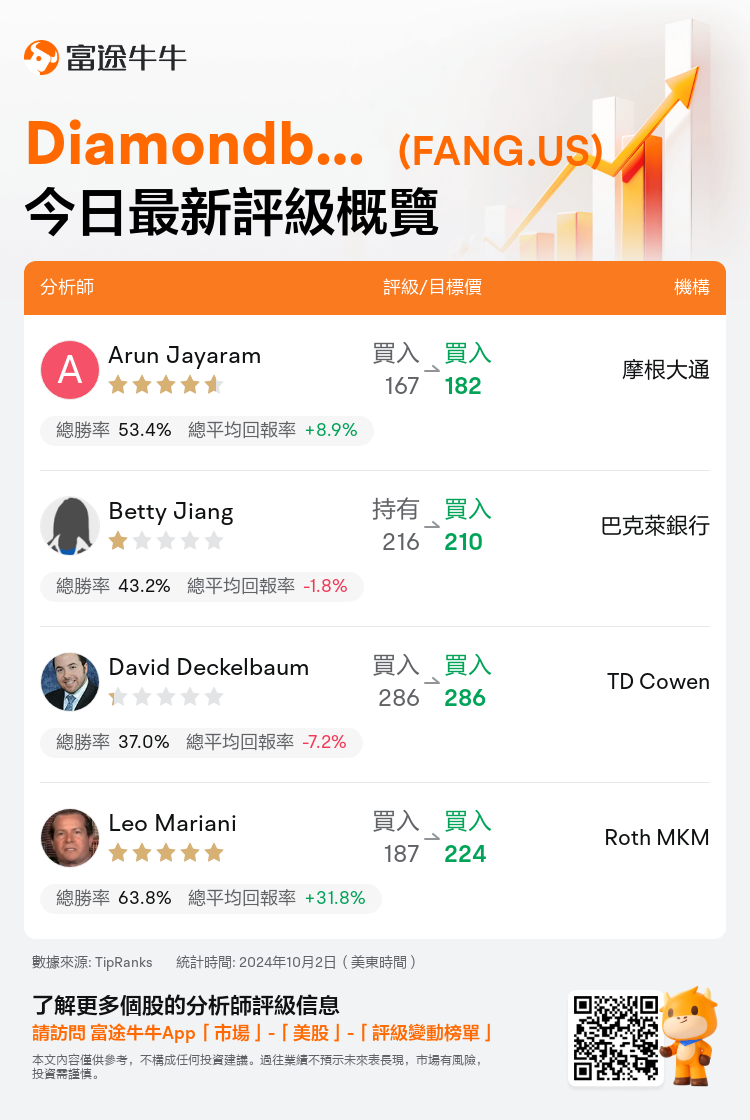

美東時間10月2日,多家華爾街大行更新了$Diamondback Energy (FANG.US)$的評級,目標價介於182美元至286美元。

摩根大通分析師Arun Jayaram維持買入評級,並將目標價從167美元上調至182美元。

巴克萊銀行分析師Betty Jiang上調至買入評級,並將目標價從216美元下調至210美元。

TD Cowen分析師David Deckelbaum維持買入評級,維持目標價286美元。

TD Cowen分析師David Deckelbaum維持買入評級,維持目標價286美元。

Roth MKM分析師Leo Mariani維持買入評級,並將目標價從187美元上調至224美元。

此外,綜合報道,$Diamondback Energy (FANG.US)$近期主要分析師觀點如下:

由於歐佩克+原油即將回歸,石油宏觀環境在短期內可能仍面臨挑戰,因此響尾蛇能源的表現相對跑贏大盤。這歸因於其在米德蘭盆地成本曲線低端的優勢地位,這使得股息覆蓋率低於每桶45美元。

隨着Endeavor的全面整合,Diamondback Energy被認爲是未來幾個季度中最有希望的一系列積極事件之一。預計該公司將宣佈一項2025年計劃,該計劃將超過最初的資本效率預期。最近股價下跌的部分原因是Endeavor賣家的流動性事件,這被視爲投資者考慮進入市場的好時機。

勘探和生產部門估計值的調整反映了修訂後的商品價格假設和投資格局。人們認爲,如果繼續提高運營效率,進一步降低服務費用,勘探和生產公司可以在2025年之前保持更高的資本效率,從而有可能抵消資源成熟度的影響。

在全球貨幣寬鬆趨勢中,由於基本面挑戰以及預計2025年可能出現失衡,能源大宗商品和相關股票可能無法參與。儘管如此,有人建議不要違背中央銀行的政策,這表明原油市場的正面風險可能大於負面風險。隨着本季度的結束,預計即將發佈的更新可能顯示低於預期的短期估計。

以下爲今日4位分析師對$Diamondback Energy (FANG.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。