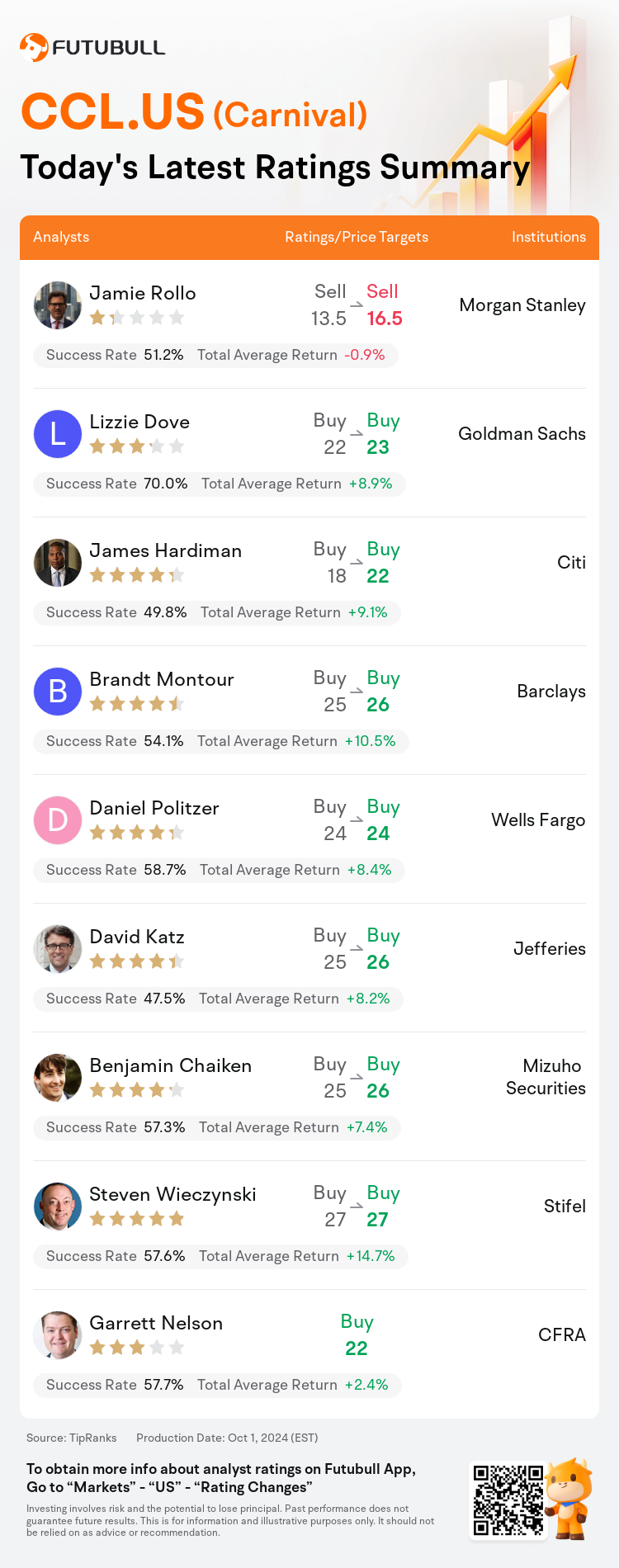

On Oct 01, major Wall Street analysts update their ratings for $Carnival (CCL.US)$, with price targets ranging from $16.5 to $27.

Morgan Stanley analyst Jamie Rollo maintains with a sell rating, and adjusts the target price from $13.5 to $16.5.

Goldman Sachs analyst Lizzie Dove maintains with a buy rating, and adjusts the target price from $22 to $23.

Citi analyst James Hardiman maintains with a buy rating, and adjusts the target price from $18 to $22.

Citi analyst James Hardiman maintains with a buy rating, and adjusts the target price from $18 to $22.

Barclays analyst Brandt Montour maintains with a buy rating, and adjusts the target price from $25 to $26.

Wells Fargo analyst Daniel Politzer maintains with a buy rating, and maintains the target price at $24.

Furthermore, according to the comprehensive report, the opinions of $Carnival (CCL.US)$'s main analysts recently are as follows:

Following Carnival's Q3 report, the forecasted EPS for FY24, FY25, and FY26 has been increased by 8%, 13%, and 12%, respectively. It's observed that the cruise booking environment is outperforming other travel segments, and Carnival benefits from favorable fuel and currency conditions. However, its asset-heavy model combined with high operational and financial leverage makes it more vulnerable to economic slowdowns compared to other companies being monitored.

Carnival's recent quarterly report and subsequent guidance for the fourth quarter may not meet all expectations, yet the optimistic signals from underlying demand factors and management's commentary suggest that the potential for growth by 2025 remains unshaken. The company's performance this quarter, despite not being the most straightforward example of exceeding expectations, demonstrated another period of strong fundamental metrics.

Carnival has shown 'better than expected' incremental margins, and the ability to achieve revenue and EBITDA rates significantly surpassing those of 2019 in the second and third quarters indicates potential for an enhanced overall business margin profile. With Carnival now set to leverage additional revenue over a more efficient cost structure, the strengthening of incremental margins is viewed as an underrecognized aspect of the company's narrative.

Here are the latest investment ratings and price targets for $Carnival (CCL.US)$ from 9 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

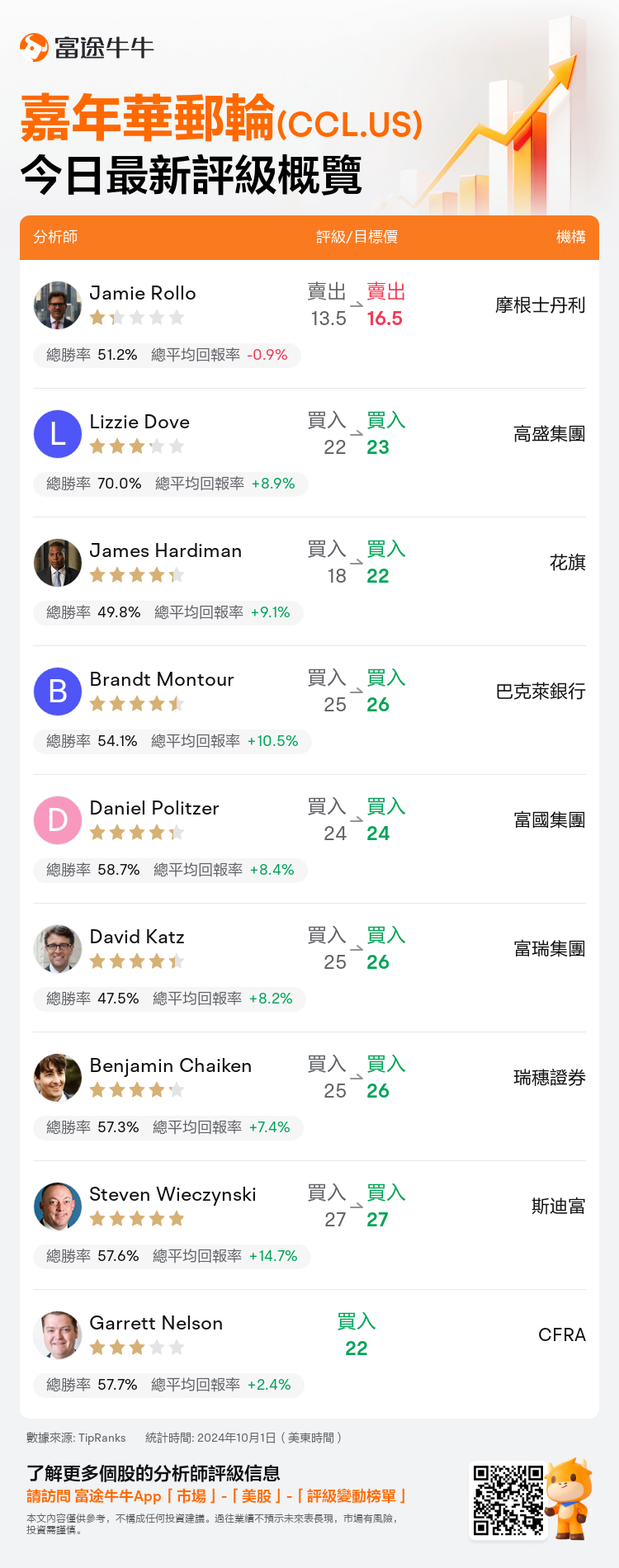

美東時間10月1日,多家華爾街大行更新了$嘉年華郵輪 (CCL.US)$的評級,目標價介於16.5美元至27美元。

摩根士丹利分析師Jamie Rollo維持賣出評級,並將目標價從13.5美元上調至16.5美元。

高盛集團分析師Lizzie Dove維持買入評級,並將目標價從22美元上調至23美元。

花旗分析師James Hardiman維持買入評級,並將目標價從18美元上調至22美元。

花旗分析師James Hardiman維持買入評級,並將目標價從18美元上調至22美元。

巴克萊銀行分析師Brandt Montour維持買入評級,並將目標價從25美元上調至26美元。

富國集團分析師Daniel Politzer維持買入評級,維持目標價24美元。

此外,綜合報道,$嘉年華郵輪 (CCL.US)$近期主要分析師觀點如下:

繼嘉年華發布第三季度報告後,24財年、25財年和26財年的預測每股收益分別增長了8%、13%和12%。據觀察,郵輪預訂環境的表現優於其他旅行細分市場,嘉年華受益於有利的燃料和貨幣條件。但是,與其他受監控的公司相比,其資產密集型模式加上高運營和財務槓桿率使其更容易受到經濟放緩的影響。

嘉年華最近的季度報告和隨後的第四季度指引可能無法滿足所有預期,但來自潛在需求因素的樂觀信號和管理層的評論表明,到2025年,增長潛力仍未動搖。該公司本季度的業績儘管不是超出預期的最直接例子,但顯示出又一個強勁的基本面指標。

嘉年華的增量利潤率 「好於預期」,第二和第三季度實現收入和息稅折舊攤銷前利潤率大幅超過2019年的能力,這表明整體業務利潤率有可能提高。隨着嘉年華現在準備利用額外收入來實現更有效的成本結構,增量利潤率的提高被視爲該公司敘事中一個未被充分認識的方面。

以下爲今日9位分析師對$嘉年華郵輪 (CCL.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。