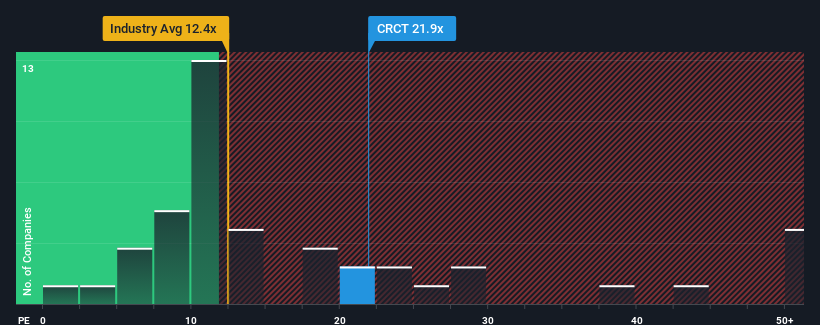

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider Cricut, Inc. (NASDAQ:CRCT) as a stock to potentially avoid with its 21.9x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Cricut certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

NasdaqGS:CRCT Price to Earnings Ratio vs Industry September 28th 2024 Although there are no analyst estimates available for Cricut, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

Is There Enough Growth For Cricut?

In order to justify its P/E ratio, Cricut would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 68% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Comparing that to the market, which is predicted to deliver 15% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's alarming that Cricut's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Cricut's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Cricut currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 3 warning signs for Cricut (1 can't be ignored!) that you need to take into consideration.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

當美國近一半的公司市盈率低於18倍時,您可能會考慮避開 Cricut, Inc. (納斯達克: CRCT) 這支股票,因爲它的市盈率爲 21.9倍。儘管如此,我們需要深入挖掘,以判斷這高市盈率是否存在合理的基礎。

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 68% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen a very unpleasant 68% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

回顧過去一年,公司底線取得了異常的40%增長。然而,這還不夠,因爲最近三年出現了累計68%的EPS大幅下降。因此,股東對中期盈利增長率感到悲觀。

回顧過去一年,公司底線取得了異常的40%增長。然而,這還不夠,因爲最近三年出現了累計68%的EPS大幅下降。因此,股東對中期盈利增長率感到悲觀。