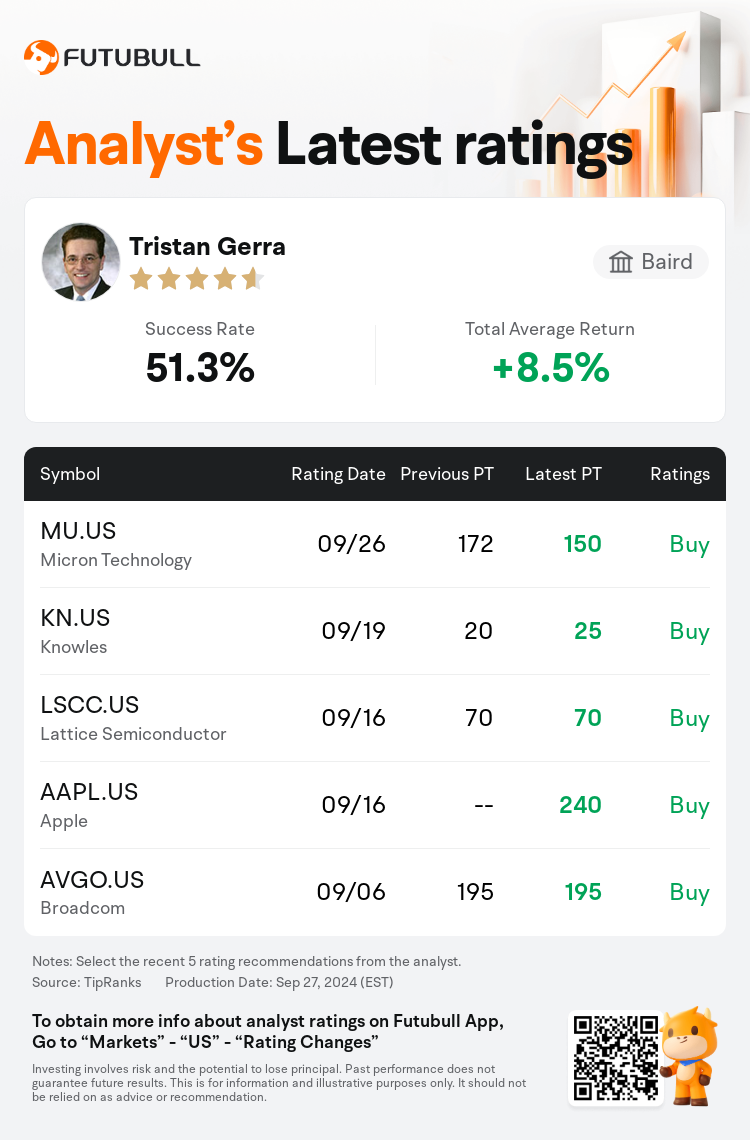

Baird analyst Tristan Gerra maintains $Micron Technology (MU.US)$ with a buy rating, and adjusts the target price from $172 to $150.

According to TipRanks data, the analyst has a success rate of 51.3% and a total average return of 8.5% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Micron Technology (MU.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Micron Technology (MU.US)$'s main analysts recently are as follows:

Micron delivered a robust quarter and outlook, which is particularly notable given the tempered recent expectations. The company provided EPS guidance that aligned with consensus estimates prior to recent negative adjustments. They reached their target of several hundred million in HBM sales for FY24 and are holding on to their projection of achieving several billion next year. Additionally, they expect to attain their desired DRAM market share—mid-20s—in HBM. However, the market forecast is perceived as overly optimistic. Management at Micron is performing well, yet the stock's valuation is considered high. It is suggested that there are more favorable risk-reward opportunities in other areas of AI and memory.

Micron has reported results that exceeded expectations and also raised future guidance, despite facing growing macroeconomic challenges. This performance is supported by robust demand in the data center sector, which is further bolstered by the company's growth in high-bandwidth memory sales that leverage artificial intelligence. Although a milder fiscal second quarter is anticipated due to seasonality, the projections for FY25 and FY26 earnings per share have been increased significantly.

Micron anticipates that its share of the High Bandwidth Memory (HBM) market will align with its general DRAM market share by the calendar year 2025, a central point of the investment thesis due to the belief that HBM can yield gross margins in the low-60% range and represent a 60% compound annual growth rate (CAGR). The view is that the stock remains undervalued and the potential of the HBM market has not been completely factored into its current pricing.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

贝雅分析师Tristan Gerra维持$美光科技 (MU.US)$买入评级,并将目标价从172美元下调至150美元。

根据TipRanks数据显示,该分析师近一年总胜率为51.3%,总平均回报率为8.5%。

此外,综合报道,$美光科技 (MU.US)$近期主要分析师观点如下:

此外,综合报道,$美光科技 (MU.US)$近期主要分析师观点如下:

Micron发布了强劲的季度业绩和展望,尤其值得注意的是在近期调整后的淡化预期下。该公司提供的每股收益指引与最近负面调整前的共识预期一致。他们实现了对FY24数亿美元HBm销售的目标,并保持了明年实现数十亿的预测。此外,他们期望在HBm中获得期望的DRAM市场份额——中期20多个百分点。然而,市场预测被视为过于乐观。Micron的管理层表现良好,但股价估值被认为过高。建议在人工智能和内存的其他领域中存在更有利的风险回报机会。

尽管面临日益严峻的宏观经济挑战,Micron已经报告了超出预期的业绩,并提高了未来的指引。这一表现得到了数据中心板块需求强劲支撑,该需求进一步得到了高带宽内存销售的增长的支持,而这些销售利用了人工智能。尽管由于季节性因素,预计较为温和地度过财政第二季度,但FY25和FY26每股收益的预测已大幅增加。

Micron预计其在日历年2025年前该公司High Bandwidth Memory (HBM)市场份额将与其整体DRAM市场份额一致,这是投资论点的一个核心,因为人们相信HBm可以实现低60%的毛利率,并代表着60%的复合年增长率。人们认为该股仍被低估,HBm市场的潜力尚未完全反映在其当前定价中。

提示:

TipRanks为独立第三方,提供金融分析师的分析数据,并计算分析师推荐的平均回报率和胜率。提供的信息并非投资建议,仅供参考。本文不对评级数据和报告的完整性与准确性做出认可、声明或保证。

TipRanks提供每位分析师的星级,分析师星级代表分析师所有推荐的过往表现,通过分析师的总胜率和平均回报率综合计算得出,星星越多,则该分析师过往表现越优异,最高为5颗星。

分析师总胜率为近一年分析师的评级成功次数占总评级次数的比率。评级的成功与否,取决于TipRanks的虚拟投资组合是否从该股票中产生正回报。

总平均回报率为基于分析师的初始评级创建虚拟投资组合,并根据评级变化对组合进行调整,在近一年中该投资组合所获得的回报率。