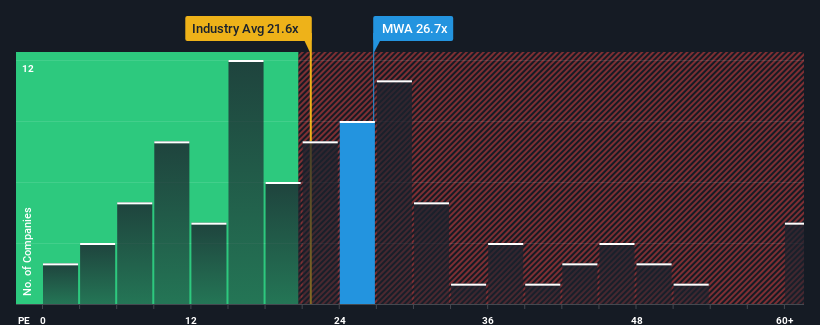

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider Mueller Water Products, Inc. (NYSE:MWA) as a stock to potentially avoid with its 26.7x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Mueller Water Products certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors' willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:MWA Price to Earnings Ratio vs Industry September 25th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Mueller Water Products.

How Is Mueller Water Products' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Mueller Water Products' is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 64%. The strong recent performance means it was also able to grow EPS by 59% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 33% as estimated by the five analysts watching the company. That's shaping up to be materially higher than the 15% growth forecast for the broader market.

In light of this, it's understandable that Mueller Water Products' P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Mueller Water Products' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Mueller Water Products with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on Mueller Water Products, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

當美國近一半的公司市盈率低於18倍時,您可能要考慮避免買入Mueller Water Products,Inc.(紐交所:MWA)股票,因爲它的市盈率爲26.7倍。然而,市盈率可能之所以高,需要進一步調查來判斷是否合理。

最近Mueller Water Products確實表現不錯,盈利增長爲正,而大多數其他公司的盈利卻在下滑。看起來很多人在期待該公司繼續抵禦更廣泛市場的逆境,這增加了投資者願意爲該股票支付更高價格。希望事情是這樣,否則你支付了一個相當高的價格,卻沒有特別的原因。

紐交所:MWA市盈率與行業板塊2024年9月25日對比 如果您想了解分析師預測的未來走勢,您應該查看我們關於Mueller Water Products的免費報告。

Mueller Water Products的增長趨勢如何?

您唯一會真正舒適看到像Mueller Water Products這樣高的市盈率,是當公司的增長正朝着超越市場的方向發展。

If we review the last year of earnings growth, the company posted a terrific increase of 64%. The strong recent performance means it was also able to grow EPS by 59% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

If we review the last year of earnings growth, the company posted a terrific increase of 64%. The strong recent performance means it was also able to grow EPS by 59% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

如果我們回顧過去一年的收益增長,該公司發佈了驚人的64%的增幅。最近的強勁表現意味着它在過去三年內總共增長了59%的每股收益。因此,股東可能會對那些中期收益增長率感到滿意。

如果我們回顧過去一年的收益增長,該公司發佈了驚人的64%的增幅。最近的強勁表現意味着它在過去三年內總共增長了59%的每股收益。因此,股東可能會對那些中期收益增長率感到滿意。