Wilhelmina International, Inc. (NASDAQ:WHLM) shares have had a horrible month, losing 28% after a relatively good period beforehand. Indeed, the recent drop has reduced its annual gain to a relatively sedate 8.8% over the last twelve months.

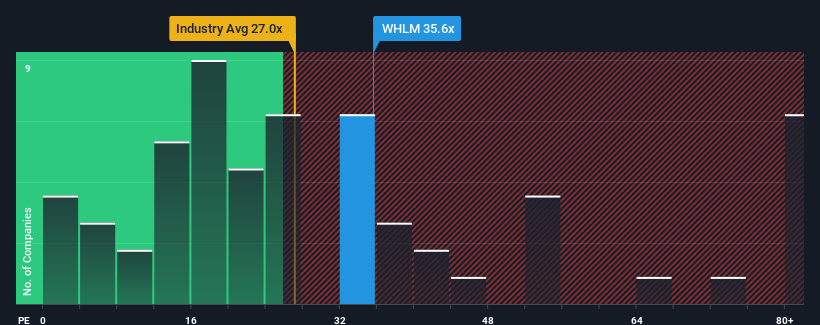

Even after such a large drop in price, given close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may still consider Wilhelmina International as a stock to avoid entirely with its 35.6x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For example, consider that Wilhelmina International's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NasdaqCM:WHLM Price to Earnings Ratio vs Industry September 25th 2024 Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Wilhelmina International will help you shine a light on its historical performance.

Is There Enough Growth For Wilhelmina International?

In order to justify its P/E ratio, Wilhelmina International would need to produce outstanding growth well in excess of the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 69%. As a result, earnings from three years ago have also fallen 83% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to grow by 15% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Wilhelmina International is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Bottom Line On Wilhelmina International's P/E

A significant share price dive has done very little to deflate Wilhelmina International's very lofty P/E. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Wilhelmina International currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Before you take the next step, you should know about the 3 warning signs for Wilhelmina International (1 shouldn't be ignored!) that we have uncovered.

If these risks are making you reconsider your opinion on Wilhelmina International, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/E ratio, Wilhelmina International would need to produce outstanding growth well in excess of the market.

In order to justify its P/E ratio, Wilhelmina International would need to produce outstanding growth well in excess of the market.

爲了證明其市盈率,wilhelmina國際需要產生遠遠超過市場的傑出增長。

爲了證明其市盈率,wilhelmina國際需要產生遠遠超過市場的傑出增長。