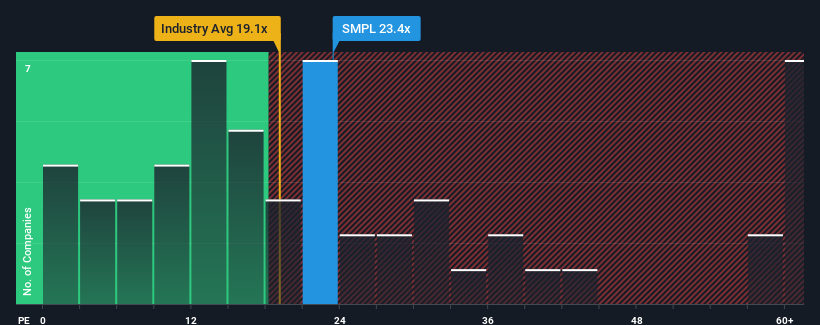

The Simply Good Foods Company's (NASDAQ:SMPL) price-to-earnings (or "P/E") ratio of 23.4x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Simply Good Foods has been doing quite well of late. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NasdaqCM:SMPL Price to Earnings Ratio vs Industry September 20th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Simply Good Foods.

Is There Enough Growth For Simply Good Foods?

The only time you'd be truly comfortable seeing a P/E as high as Simply Good Foods' is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 15% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 11% per annum as estimated by the ten analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 10% per annum, which is not materially different.

In light of this, it's curious that Simply Good Foods' P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Simply Good Foods currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Simply Good Foods with six simple checks.

If you're unsure about the strength of Simply Good Foods' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 15% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Retrospectively, the last year delivered an exceptional 15% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

回顧過去,去年爲公司的底線帶來了異常的15%增長。然而,EPS從三年前開始總體上幾乎沒有增長,這並不理想。因此,股東們可能不會對不穩定的中期增長率感到滿意。

回顧過去,去年爲公司的底線帶來了異常的15%增長。然而,EPS從三年前開始總體上幾乎沒有增長,這並不理想。因此,股東們可能不會對不穩定的中期增長率感到滿意。