The Kroger Co. (NYSE:KR) On An Uptrend: Could Fundamentals Be Driving The Stock?

The Kroger Co. (NYSE:KR) On An Uptrend: Could Fundamentals Be Driving The Stock?

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity Kroger's (NYSE:KR) stock up by 9.2% over the past three months. As most would know, long-term fundamentals have a strong correlation with market price movements, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Specifically, we decided to study Kroger's ROE in this article.

Kroger(紐交所: KR)股價在過去三個月上漲了9.2%。 衆所周知,長期基本面與市場價格走勢存在很強的相關性,因此我們決定今天查看該公司的關鍵財務指標,以判斷其是否在最近的價格波動中扮演了任何角色。 具體來說,我們決定在本文中研究Kroger的roe。

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

roe,即淨資產收益率,是一種評估公司如何有效地從股東手中獲取投資回報的有用工具。換句話說,它是一種盈利能力比率,衡量公司股東提供的資本的回報率。

How Do You Calculate Return On Equity?

怎樣計算ROE?

The formula for return on equity is:

權益回報率的計算公式是:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

淨資產收益率 = 淨利潤(從持續經營中獲得)÷ 股東權益

So, based on the above formula, the ROE for Kroger is:

因此,根據上述公式,Kroger的roe爲:

22% = US$2.8b ÷ US$13b (Based on the trailing twelve months to August 2024).

22% = 280億美元 ÷ 1300億美元(基於截至2024年8月的過去十二個月)。

The 'return' refers to a company's earnings over the last year. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.22.

「回報」指的是公司過去一年的收益。這意味着,對於每1美元股東的投資,公司能賺取0.22美元的利潤。

What Is The Relationship Between ROE And Earnings Growth?

ROE與盈利增長之間的關係是什麼?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

到目前爲止,我們已經了解到roe是衡量公司利潤產生效率的指標。根據公司選擇再投資或「保留」其利潤的比例,我們隨後可以評估公司未來利潤的能力。其他條件都相同的情況下,roe和利潤保留率都較高的公司通常比沒有這些特徵的公司有更高的增長速度。

A Side By Side comparison of Kroger's Earnings Growth And 22% ROE

Kroger的盈利增長和22%ROE的並列比較

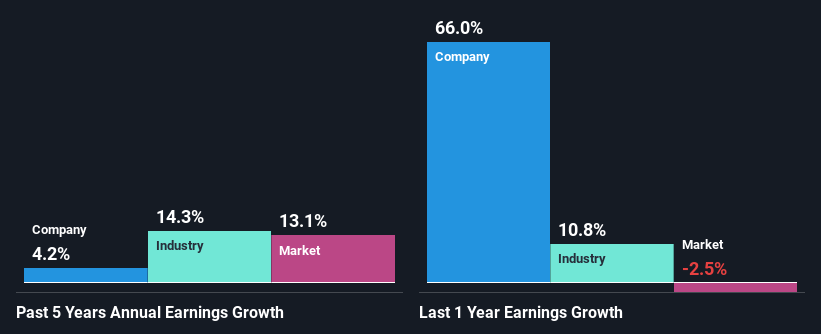

To begin with, Kroger seems to have a respectable ROE. Further, the company's ROE compares quite favorably to the industry average of 11%. Despite this, Kroger's five year net income growth was quite low averaging at only 4.2%. This is generally not the case as when a company has a high rate of return it should usually also have a high earnings growth rate. Such a scenario is likely to take place when a company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

首先,Kroger的ROE似乎相當可觀。此外,該公司的ROE與行業平均水平相比非常有優勢,爲11%。儘管如此,Kroger在過去五年的淨利潤增長率相當低,平均只有4.2%。這通常情況下並不成立,因爲當一個公司的回報率很高時,通常也應該有較高的盈利增長率。這種情況通常發生在公司將其盈利的很大一部分作爲股息支付或面臨競爭壓力時。

As a next step, we compared Kroger's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 14% in the same period.

作爲下一步,我們將Kroger的淨利潤增長率與行業進行了比較,很遺憾地發現該公司的增長率低於同期行業的平均增長率14%。

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is KR fairly valued? This infographic on the company's intrinsic value has everything you need to know.

給公司附加價值的基礎很大程度上取決於其盈利增長。投資者需要判斷的是,預期的盈利增長,或者缺乏盈利增長,是否已經融入股價中。然後這有助於他們判斷股票是面臨光明還是暗淡的未來。KR是否定價合理?關於公司內在價值的信息圖表包含了你需要了解的一切。

Is Kroger Efficiently Re-investing Its Profits?

Kroger有效地重新投資其利潤嗎?

Despite having a normal three-year median payout ratio of 34% (or a retention ratio of 66% over the past three years, Kroger has seen very little growth in earnings as we saw above. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

儘管Kroger過去三年的中位數支付比率爲34%(或過去三年的留存比率爲66%),盈利增長卻非常有限,正如我們上文所看到的。因此,這裏可能還有其他因素在起作用,這些因素可能潛在地妨礙了增長。例如,該業務曾面臨一些不利因素。

In addition, Kroger has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 28%. As a result, Kroger's ROE is not expected to change by much either, which we inferred from the analyst estimate of 19% for future ROE.

此外,Kroger至少十年來一直在支付股息,這表明即使以犧牲業務增長爲代價,維持股息支付對管理層來說更爲重要。根據最新的分析師估計,我們發現公司未來三年的股息支付比率預計將穩定在28%左右。因此,預計Kroger的roe也不會有太大的變化,這是我們從分析師對未來roe的預測中得出的結論,預計爲19%。

Conclusion

結論

On the whole, we do feel that Kroger has some positive attributes. Although, we are disappointed to see a lack of growth in earnings even in spite of a high ROE and and a high reinvestment rate. We believe that there might be some outside factors that could be having a negative impact on the business. We also studied the latest analyst forecasts and found that the company's earnings growth is expected be similar to its current growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

總體而言,我們確實認爲Kroger具有一些積極的特點。儘管ROE和高再投資率都很高,但我們對利潤的增長缺乏滿意,甚至沒有增長。我們相信可能存在一些外部因素對業務產生負面影響。我們還研究了最新的分析師預測,發現公司的盈利增長預計與目前的增長率相似。要了解更多關於公司最新的分析師預測,請查看這份分析師預測的可視化。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。