With 5.9% One-year Returns, Institutional Owners May Ignore Starbucks Corporation's (NASDAQ:SBUX) 3.2% Stock Price Decline

With 5.9% One-year Returns, Institutional Owners May Ignore Starbucks Corporation's (NASDAQ:SBUX) 3.2% Stock Price Decline

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index. Key Insights

主要見解

- Significantly high institutional ownership implies Starbucks' stock price is sensitive to their trading actions

- The top 25 shareholders own 45% of the company

- Recent purchases by insiders

- 機構持有大量股份意味着星巴克的股價對他們的交易行爲很敏感。

- 前25名股東擁有該公司的45%股份。

- 最近有內部人員購買。

A look at the shareholders of Starbucks Corporation (NASDAQ:SBUX) can tell us which group is most powerful. With 76% stake, institutions possess the maximum shares in the company. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

通過查看星巴克公司(NASDAQ: SBUX)的股東,我們可以知道哪個群體最有力量。機構持有最多的股份,佔有76%的股權。換句話說,這個群體將從他們對該公司的投資中獲得最多(或損失最多)。

Losing money on investments is something no shareholder enjoys, least of all institutional investors who saw their holdings value drop by 3.2% last week. However, the 5.9% one-year return to shareholders may have helped lessen their pain. They should, however, be mindful of further losses in the future.

在投資中虧錢是股東中沒有一個人願意經歷的,尤其是機構投資者上週看到他們的持股價值下跌了3.2%。然而,5.9%的股東一年回報率可能有助於減輕他們的痛苦。但是,他們應該謹記未來可能繼續虧損。

Let's take a closer look to see what the different types of shareholders can tell us about Starbucks.

讓我們更仔細地看看不同類型的股東能夠告訴我們關於星巴克的信息。

What Does The Institutional Ownership Tell Us About Starbucks?

機構持有量告訴我們星巴克的什麼?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

機構投資者通常將自己的回報與常見的指數回報進行比較。因此,他們通常會考慮購買包括在相關基準指數中的較大公司。

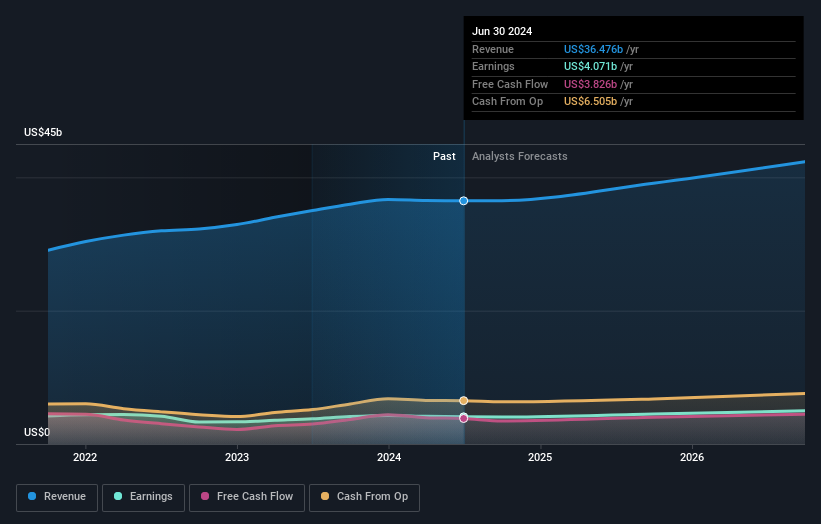

Starbucks already has institutions on the share registry. Indeed, they own a respectable stake in the company. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Starbucks' historic earnings and revenue below, but keep in mind there's always more to the story.

星巴克已經有機構參與股東註冊。實際上,他們在公司擁有相當大的股份。這意味着那些機構的分析師已經研究了這隻股票,並對其看好。但就像其他任何人一樣,他們也可能錯了。當多個機構擁有一支股票時,總有一種風險,即它們處於'擠爆交易'狀態。當這樣的交易失敗時,多方可能競相快速拋售股票。在一家沒有增長曆史的公司,這種風險更高。您可以在下面看到星巴克的歷史收益和營業收入,但請記住故事往往不止這些。

Since institutional investors own more than half the issued stock, the board will likely have to pay attention to their preferences. We note that hedge funds don't have a meaningful investment in Starbucks. The Vanguard Group, Inc. is currently the largest shareholder, with 9.7% of shares outstanding. BlackRock, Inc. is the second largest shareholder owning 7.0% of common stock, and State Street Global Advisors, Inc. holds about 4.0% of the company stock.

由於機構投資者擁有超過一半的已發行股票,董事會很可能需要關注他們的偏好。我們注意到對沖基金對星巴克沒有有意義的投資。Vanguard Group,Inc.目前是最大的股東,持有9.7%的已發行股票。BlackRock,Inc.是第二大股東,持有7.0%的普通股,而State Street Global Advisors,Inc.持有該公司股份的約4.0%。

Our studies suggest that the top 25 shareholders collectively control less than half of the company's shares, meaning that the company's shares are widely disseminated and there is no dominant shareholder.

我們的研究表明,前25大股東共控制了公司股份的不到一半,這意味着公司的股份廣泛分散,沒有主導股東。

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. There are plenty of analysts covering the stock, so it might be worth seeing what they are forecasting, too.

研究機構所有權是衡量和過濾股票預期性能的好方法。通過研究分析師的情緒,也可以實現同樣的效果。很多分析師都在關注該股票,看看他們的預測值得不值得。

Insider Ownership Of Starbucks

星巴克內部股權

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

內部人員的定義在不同國家可能會稍有不同,但董事會成員始終算入其中。公司管理負責經營業務,但即使首席執行官是董事會成員,他或她也必須對董事會負責。

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

大多數人認爲內部所有權是積極的,因爲它可以表示董事會與其他股東的利益相一致。但是,在某些場合下,這個團體的權力過於集中。

We can see that insiders own shares in Starbucks Corporation. The insiders have a meaningful stake worth US$2.2b. we sometimes take an interest in whether they have been buying or selling.

我們可以看到內部人員在星巴克公司擁有股份。 這些內部人員持有價值22億美元的重要股權。 我們有時對他們是否在買入或賣出感興趣。

General Public Ownership

一般大衆所有權

With a 22% ownership, the general public, mostly comprising of individual investors, have some degree of sway over Starbucks. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

總體而言,持有22%股份的普通大衆,大部分是個人投資者,對星巴克具有一定程度的影響力。 儘管這個群體不能決定一切,但確實對公司的運營產生了真實的影響。

Next Steps:

下一步:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. For example, we've discovered 2 warning signs for Starbucks (1 is a bit concerning!) that you should be aware of before investing here.

在考慮擁有公司的不同群體時是非常值得的,但還有其他更重要的因素。例如,我們已經發現了星巴克的2個警示信號(其中1個有點令人擔憂!),在投資之前你應該注意這些。

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

如果您希望了解分析師在未來增長方面的預測,請務必不要錯過這份免費報告。

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

注:本文中的數據是使用最後一個財務報表日期結束的爲期12個月的數據計算的。這可能與全年年度報告數據不一致。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。