Standard Chartered believes that the US stock and bond markets, the US economy are not so fragile; inflation deviation from target is basically unrelated to base effects; economic data is mixed, which cannot prove that the unemployment rate will rise significantly; starting with a 50 basis points rate cut may exacerbate market overpricing, and it will be very difficult to guide the market's expectations for slowing down or pausing rate cuts in the future; the accuracy of measuring real interest rates is low, not the Fed's top consideration at the moment.

During the regular trading hours of US stocks on Tuesday, September 17th, the pricing in the federal funds futures market indicates that investors' probability of a 50 basis point rate cut by the Federal Reserve on Wednesday has exceeded 60%, compared to only around 30% a week ago. At the same time, the probability of a 25 basis point rate cut is less than 40% as expected by investors.

Although most market participants expect the Federal Reserve to start with an extraordinary and significant 50 basis point rate cut, Steve Englander, the G10 FX research head and global head of North America Strategy at Standard Chartered Bank, still maintains his forecast that the Fed will only cut rates by 25 basis points. He believes that, based on recent economic data, a 50 basis point rate cut is not likely to become a reality, as inflation data does not support inflation rapidly falling back to the Fed's target of 2%.

Englander points out that recent reports from The Wall Street Journal and the Financial Times have implied that some members of the Federal Open Market Committee (FOMC) may initially propose a 50 basis point rate cut. Some market participants believe that these reports are efforts by FOMC members to reduce the surprise of a 50 basis point cut. However, it is currently unclear whether these reports reflect informal comments from Fed officials during the FOMC's blackout period before the meeting.

In his recent report, Englander lists seven reasons supporting a 50 basis point rate cut and refutes each one.

Reason 1: The Federal Reserve cannot disappoint the asset markets.

According to Englander's report, as of Monday, September 16th, US stocks had declined 1.5% from their historical highs, but still increased by 26.5% compared to the same period last year. The 10-year US Treasury yield has dropped by 25 basis points since the beginning of September. Financial conditions were very accommodative before the release of the above-mentioned news reports. Even if the Fed indicates that a 50 basis point rate cut is 'not yet the right time', the asset markets are unlikely to be so fragile and be disappointed in this signal in the long term.

Reason 2: The US economy is very fragile, and if the rate cut is 25 basis points instead of 50 basis points, it will trigger an economic downturn spiral.

The report states that Standard Chartered has serious doubts about whether any economic model reflects the characteristics of an economy approaching the edge of a cliff as implied by the concerns mentioned above. A cliff-edge situation requires the eruption of an economic or market crisis, and the current situation appears to be calm.

Reason 3: The economy is clearly moving towards the 2% inflation target.

The report states that Standard Chartered opposes the use of the word "obviously" and agrees with the use of the phrase "most likely," while noting that this is only a prediction and the current data does not reflect it. Standard Chartered and the market consensus expect that the August core PCE in the United States will increase by 2.7% year-on-year. Standard Chartered believes that this indicator is unlikely to slow down significantly for the rest of this year, given the low monthly inflation rate at the end of last year. It is difficult for the year-on-year inflation growth rate to decline significantly before the end of the year. The Fed's achievement of its inflation target in the last mile may depend on how low the inflation rate is in the first quarter of next year.

Reason 4: Deviations from the inflation target are all due to base effects.

Standard Chartered believes that base effects are basically irrelevant because they reflect the situation a year ago, not the current one. The problem is that there has been a price increase in the first quarter for two consecutive years. Therefore, until the data for the first quarter of next year tells us whether the quarter-on-quarter inflation is low, we do not know if the recent two-year inflation is due to residual seasonal effects or coincidence. Only when the quarter-on-quarter inflation in the first quarter of next year remains under control is it possible to establish a path for inflation to decline from its current level.

Reason 5: If interest rates are not significantly reduced, the unemployment rate will rise significantly.

Standard Chartered believes that economic data remains mixed. There is limited evidence of large-scale layoffs. The U.S. economy is sluggish, but has not reached recession levels. If by the November or December FOMC meeting, the unemployment rate does indeed rise significantly from its current level, for example, to 4.5%, then a 50 basis point rate cut may be reasonable.

Reason 6: Making a mistake of 25 basis points in interest rate cuts is more serious than making a mistake of 50 basis points.

Standard Chartered report said that it disagrees with most of the discussions on risk management in the market. For the Fed, the question is whether it is a bigger mistake to cut 50 basis points when it should cut 25 basis points, or is it a bigger mistake to cut 25 basis points when it should cut 25 basis points. Standard Chartered believes that the Fed can provide a clear message while cutting 25 basis points, that is, the FOMC will closely monitor the reasonable conditions for cutting 50 basis points. If the unemployment rate rises to 4.5% in September, the market will be prepared for a 50 basis point cut. If the unemployment rate continues to rise in October and November, there may be a further 50 basis point cut. The market will be prepared, and the expectation of a 50 basis point rate cut will be reflected in the stock and bond markets before real action.

Starting a rate cut cycle with 50 basis points may exacerbate the market's overpricing of loose policies. If the unemployment rate remains below 4% and core PCE growth remains flat, there will be more market chaos. After starting with a 50 basis point rate cut, regardless of how the FOMC and Fed Chairman Powell state their positions, the market is likely to view this magnitude of rate cut as the norm. Guiding the market to judge the difficulty of cutting 50 basis points, 25 basis points, or suspending the rate cut will be very difficult. Standard Chartered believes that compared to accelerating rate hikes after the initial 25 basis point hike, slowing down the pace after the initial 50 basis point rate cut may bring much greater market uncertainty.

Reason 7: The real interest rate is too high and must be reduced immediately.

Standard Chartered noticed that Powell has stated that he relies on data and is skeptical of immeasurable factors. Under the most favorable conditions, the accuracy of sample measurement of the equilibrium real interest rate is low, and the real-time measurement accuracy is extremely low. Not long ago, the market had a heated discussion about the limited impact of the real interest rate on economic activity. Whether the real interest rate is at a neutral level or more than 50 basis points above in the 5-10 year period may be important, but Standard Chartered believes that this deviation is unlikely to have an impact on quarter-on-quarter or even year-on-year GDP. If the Fed is still uncertain about the final mile of the downward trend in inflation, the claim for real interest rates can only rank second or third.

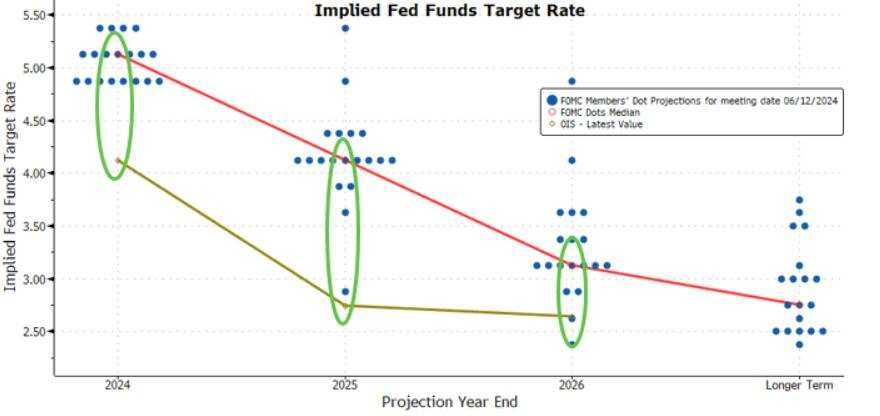

Englander also listed the two major risks of cutting interest rates by 50 basis points. First, the Fed's forecast may be wrong. The median rate forecast of Fed officials announced in June shows that FOMC's Fed decision-makers have reduced their forecast for three rate cuts this year to one. The Fed's goal is to send a clear signal of the medium-term policy direction. If expectations for inflation and unemployment are proven to be wrong, the Fed will be in a policy-making state similar to the stop-and-go policies of the 1970s.

The second risk is that some people may interpret the 50 basis point rate cut in September as an action influenced by political factors. For example, it is very likely that Trump will interpret a significant rate cut as the Fed secretly supporting the Democratic Party to boost confidence and asset markets. From the Fed's own perspective, it should not make decisions that can be seen as favorable to one party before the election, which would call into question the Fed's independence from political influence.

Editor/new