On September 17, Cui Dongshu released an analysis of the national charging pile market in August 2024.

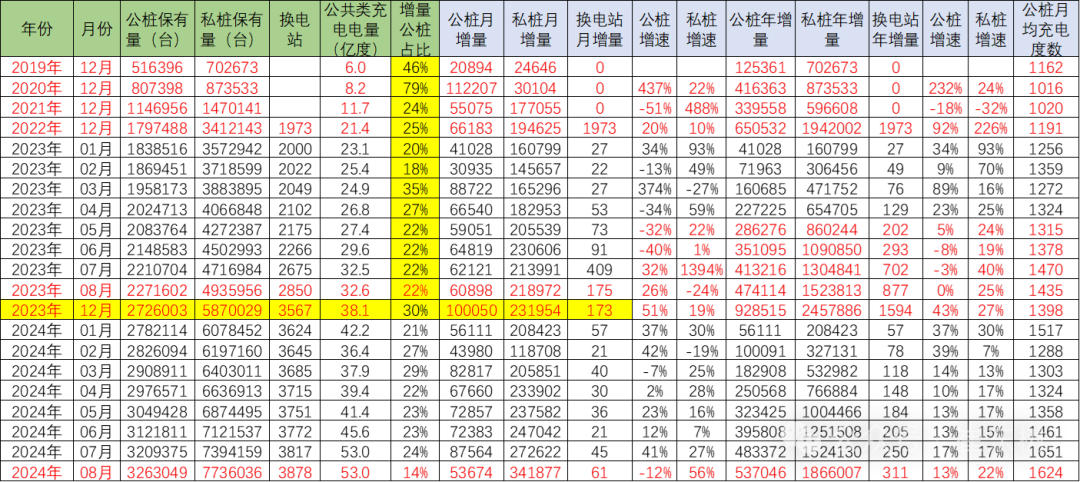

According to the data analysis of the China Charging Alliance organized by the China Passenger Car Association, the total number of public charging piles in August 2024 reached 3.26 million, an increase of 0.0536 million from the previous month, with a growth rate slower than the same period last year; the annual cumulative increase of public piles in 2024 reached 0.54 million, with a growth rate of 13% year-on-year. Currently, there are 7.74 million private charging piles, an increase of 0.342 million from the previous month, with a growth rate faster than August 2023 by 56%; the annual cumulative increase of private piles in 2024 reached 1.87 million, with a growth rate of 22% year-on-year. The charging volume of public piles reached 5.3 billion kWh, showing good growth compared to the same period, with an average monthly charge of 1624 kWh per pile, which is an improvement from 1435 kWh in August last year.

In recent years, China's charging infrastructure has developed rapidly and has become the world's largest, most widely-serviced, and most comprehensive charging infrastructure system in terms of the variety and types of chargers. Currently, according to the calculation of 1 public charging pile equals 3 private ones, China's ratio of electric vehicle chargers in 2024 market is already 1:1, far exceeding that of other countries in the world.

Currently, there are still problems that need to be addressed to improve the charging infrastructure. These include the issue of inadequate layout, unreasonable structure, outdated charging infrastructure technology, uneven service distribution, and lack of regulation. In some low-tier cities, the rate of electric vehicle purchase regret has increased. However, with the continuous increase in scale and the small adjustment difficulty, the potential for improvement of electric vehicles is huge.

The moderate development of charging piles has resulted in low utilization rates and an overall negative operating profit for charging facility operations. Currently, the ratio of the incremental pure electric passenger cars to public charging piles is 1.5:1. If one public charging pile serves at least three cars, then the ratio of the pure electric passenger car charging system is basically 1:1, which is relatively good.

From the perspective of the operation of charging companies, the performance of top operators is relatively strong. GAC New Energy's charging piles averaged 6384 kWh of charging in August, performing well every month. Nio's charging piles reached around 10196 kWh. In contrast, the average monthly charging of some old charging piles is only slightly above 100 kWh, while the average monthly charging of major charging companies is at the level of thousands of kWh, resulting in extremely large differences in charging volume efficiency, ranging from several times to tens of times. Tesla's monthly data remains stable and very good. In view of the rapid growth trend of future new energy vehicles, especially electric vehicles, it is necessary to further build a high-quality charging infrastructure system, update old low-power AC piles, increase the upgrade of high-power DC fast charging, and better meet the needs of the people in purchasing and using new energy vehicles, to promote the green and low-carbon transformation of transportation and the construction of modern infrastructure systems.

Charging infrastructure provides charging and battery swapping services for electric vehicles and is an important transportation and energy integration class infrastructure.

The number of public charging piles increased by 0.34 million in 2021, and the number of private charging piles increased by 0.6 million, YoY decreases of 18% and 32%, respectively.

Public charging piles increased by 0.65 million in 2022, and private charging piles increased by 1.94 million, YoY growth rates of 92% and 226%, respectively.

Public charging piles increased by 0.93 million in 2023, a growth rate of 43% YoY. The number of private charging piles increased by 2.457 million at the end of 2023 compared to July, with a growth rate of 27% YoY.

In August 2024, the total number of public charging stations reached 3.26 million, an increase of 0.0536 million from the previous month, slower than the same period last year. The cumulative increase in public charging stations in 2024 was 0.54 million, with a year-on-year growth rate of 13%. Currently, there are 7.74 million private charging stations, with an increase of 0.342 million in August compared to the previous month, a growth rate of 56% faster than August 2023. The cumulative increase in private charging stations in 2024 was 1.87 million, with a year-on-year growth rate of 22%. The charging volume of public charging stations was 5.3 billion kilowatt-hours, showing good growth compared to the same period last year, with an average monthly charging of 1624 kilowatt-hours per station, showing good growth compared to August last year (1435 kilowatt-hours).

Charging stations are mainly for private use. According to surveys, charging is generally done through private charging stations, shared charging stations, and public charging stations in residential areas or companies, with each accounting for between 22% and 26%, reaching a total of about 75%. Some respondents who have insufficient access to charging stations outside their residential areas charge at public charging stations on the roadside, while others charge at public charging stations in places such as malls and cinemas.

From January to August 2024, the number of public charging stations increased by 0.537 million compared to the end of 2023, with a fast growth rate of 13%.

From January to August 2024, the number of public charging stations in Guangdong increased by 0.06 million, with a market share of 19%. In the same period last year, the increment was 0.12 million, with a market share of 22%. This year, the market share has declined.

There are huge differences in the situation of public charging stations in various regions, mainly due to larger charging station scales in more developed cities. Charging stations in Guangdong, Jiangsu, Zhejiang, Shanghai, and Beijing are built relatively well.

From January to August 2024, the number of charging stations in Shandong increased by approximately 0.038 million, while Sichuan saw an increase of around 0.03 million, indicating a rapid growth in market share.

Beijing has about 0.14 million public charging stations, with an increase of 0.011 million this year. The scale is already large and still growing steadily, similar to the situation in Shanghai.

Currently, China’s public charging stations fare better than Europe and the US in terms of charging outlets to electric vehicle ratio, but there is a problem of low utilization rate. Firstly, coverage is inadequate. Currently, 10% of the service areas along the highway have not been covered, and the coverage rate of charging infrastructure in rural areas is less than 5%. Secondly, the structure is unreasonable. 99% of the charging facilities are still fast and slow charging, and 64% of the public DC charging stations are still low-voltage charging stations with 750V or less power, which cannot support the development of higher-voltage ultra-fast charging of 800V and above. From a micro level, firstly, the operation and maintenance cost is high. The proportion of mute equipment has exceeded 30%, the digitization level is low, and it has increased the difficulty and cost of operation and maintenance management. Secondly, the quality of traditional air-cooling equipment is poor. The equipment life span is only 3-5 years, and the operator will face replacement before the return of investment. Thirdly, the service quality is poor. The proportion of zombie charging stations reaching 10%, plus the failure to charge, has intensified users’ charging anxiety.

Our country's charging station operators can be roughly divided into four types: 1) Integrated enterprises in the production, manufacturing, and investment operation of charging stations, mainly using heavy asset models and focusing on the operation of their own assets, while also collaborating with other operators and third-party platforms. This includes StarCharge (a subsidiary of Wanbang Digital), TELD (Qingdao TGOOD Electric), Wanma Aichong (Zhejiang Wanma), Putian New Energy, Shanghai Yiw Energy, and Shenzhen Chedianwang (participated by Shenzhen Clou Electronics). 2) Self-built charging networks by power grid companies, including State Grid (State Grid Electric Vehicle Service Co., Ltd.) and Southern Power Grid (Southern Power Grid Electric Vehicle Service Co., Ltd.). 3) Large vehicle manufacturer groups with self-built charging networks, including Tesla, NIO Inc., Xiaopeng, SAIC AnYue, and GAC Energy. Some of these enterprises outsource the construction and operation of their charging networks to asset-based charging operators and third-party charging service providers. 4) Third-party charging network operators, such as Yunquick, Xiaojue Charging (a subsidiary of Didi Chuxing), and Shenzhen Hui Neng, mainly adopting a light asset model, focusing on the large and dispersed market of charging stations, and providing SaaS services for regional operators, essentially serving as IT service providers.

The domestic charging station operation industry faces four major competitive barriers: capital, site, grid capacity, and data resources. It is currently showing a Matthew effect, with an increase in market concentration among leading enterprises. The development scale of DC charging stations is large, and leading operators are performing well. GAC Energy's charging stations reached an average of 6384 kWh in August, with consistently strong monthly performance. NIO Inc.'s charging stations reached around 10196 kWh, while Tesla reached 3634 kWh, both consistently demonstrating strong monthly performance. Meanwhile, some older charging stations have an average monthly power consumption of only over 100 kWh, while the monthly power consumption of leading charging companies is at the level of thousands of kWh. The significant difference in power consumption results in massive differences in benefits. Tesla's monthly data remains stable and very good.

The charging station is divided into two categories: direct current (fast charge) and alternating current (slow charge). Direct current charging station: large in size, with high voltage, high power, and fast charging, requires higher demand on the power grid, usually built in highway service areas, bus stations, and other places, therefore the quantity is relatively small, accounting for about 20%. Alternating current charging station: relatively lower unit price, easier installation, often privately owned, therefore more in quantity and distributed widely, accounting for over 80%. In terms of technological development trend, the direct current station is gradually moving towards high-power development.

From an international perspective, the benefit of public dedicated charging stations is the best, and orderly charging effects are evident for fixed charging needs such as public transportation. The number and density of public DC charging stations are increasing globally. In China, the proportion of DC charging stations in the public network will exceed 42% in 2024. At the same time, the Middle East has become a rising 'new star' in DC charging: the proportion of DC charging stations increased by 7% in 2022, exceeding 21%; and the density of DC charging stations increased by 125%, reaching 1.3 DC charging stations per 100 kilometers of road. Both of the above data will further increase rapidly.

The ultimate charging experience should have three key features: first, worry-free charging. Providing one-click service, visual charging station status and intelligent guidance. Second, disturbance-free charging. The charging process is ultra-quiet, with no gun-jumping on the first charge. Third: worry-free charging. Vehicle and charging station cloud collaboration, anti-electromagnetic interference, guaranteeing personal health and property safety. The alternating current station has two major defects: one is unable to achieve grid interaction, can only supply energy in one direction, and does not support V2G evolution; the other is unable to achieve vehicle and charging station collaboration, and there is a lack of digital interconnectivity between them and information exchange. Compared with traditional AC stations, low-power direct current solutions can better achieve vehicle-grid interaction and digital experience, bringing Three major values: faster charging, not limited by the OBC, and charging speed increased by 3-5 times; long-term evolution, supporting plug-and-charge, point redemption settlement, V2G and other functions; massive deployment, under the same power conditions, it can achieve 3 times coverage and increase power utilization by 50%.

The national new energy development plan clearly proposes that private slow charging is the development trend and should account for more than 90%. Currently, private charging station development is slightly slow, which seriously affects the popularization of electric vehicles.

According to the survey, the satisfaction of self-owned charging station users in various aspects (such as charging station adequacy, reasonable layout, charging prices, and accurate settlement) is higher than that of other respondents.

Private charging stations are privately owned by vehicle owners to meet the needs of charging at home, and are usually built with the car. They have a large customer base and are the absolute main force of basic charging facilities.

The domestic retail sales of pure electric passenger vehicles in January-August 2024 were 3.8 million units, with 0.54 million new public charging stations and 1.87 million private charging stations. If the number of public charging stations is compared to private charging stations in a 1:1 ratio of user service quantity, the ratio of vehicles to charging stations is 1.45:1, and the number of charging stations is relatively sufficient. Here, the special case of plug-in hybrid charging less needs to be separated. That is, the demand characteristics of the Shanghai model, which only burns fuel and does not charge.

However, if we look at the functions in detail, according to the charging utilization rate of public charging stations being three times that of private charging stations, that is, a 3:1 relationship, the ratio of charging facilities to the sales volume of pure electric vehicles reaches 0.98, which is basically a 1:1 relationship. Due to the explosive increase in public charging stations, the overall ratio of vehicle-to-pile has reached a relatively reasonable level of 1:1.