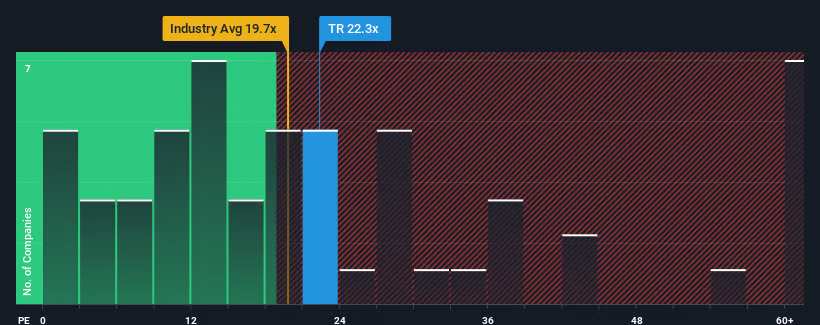

With a price-to-earnings (or "P/E") ratio of 22.3x Tootsie Roll Industries, Inc. (NYSE:TR) may be sending bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 10x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Tootsie Roll Industries has been doing a good job lately as it's been growing earnings at a solid pace. It might be that many expect the respectable earnings performance to beat most other companies over the coming period, which has increased investors' willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:TR Price to Earnings Ratio vs Industry August 27th 2024 Although there are no analyst estimates available for Tootsie Roll Industries, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

Is There Enough Growth For Tootsie Roll Industries?

In order to justify its P/E ratio, Tootsie Roll Industries would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 21% last year. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 15% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we can see why Tootsie Roll Industries is trading at such a high P/E compared to the market. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Tootsie Roll Industries maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Tootsie Roll Industries with six simple checks on some of these key factors.

If you're unsure about the strength of Tootsie Roll Industries' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

由于Tootsie Roll Industries, Inc. (纽交所: TR)的市盈率为22.3倍,这可能在此刻 发出了看跌信号,因为几乎一半的美国公司市盈率低于18倍,甚至低于10倍的情况并不罕见。尽管如此,我们需要更深入的挖掘来判断这种高市盈率是否有理性的依据。

最近Tootsie Roll Industries的业绩增长非常不错。很可能许多人预计在未来一段时间内 ,这家公司将击败大多数其他公司的尊贵业绩,从而增加了投资者为这只股票付出高价的意愿。真的希望如此,否则你将为无特殊原因付出相当可观的代价。

纽交所: TR 市盈率与行业 板块对比 2024年8月27日 尽管目前没有关于Tootsie Roll Industries的分析师预测,但可以通过查看这个免费的数据丰富的可视化工具了解该公司在盈利、营业收入和现金流方面的情况。

Tootsie Roll Industries有足够的增长来证明其市盈率吗?为了证明其市盈率,Tootsie Roll Industries需要产生超过市场的印象深刻的增长。

Taking a look back first, we see that the company grew earnings per share by an impressive 21% last year. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Taking a look back first, we see that the company grew earnings per share by an impressive 21% last year. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

首先回顾一下,我们可以看到该公司去年每股收益增长了惊人的21%。近三年来,EPS也出现了出色的65%的整体增长,得益于其短期业绩。因此,股东可能会对中期收益增长率感到满意。

首先回顾一下,我们可以看到该公司去年每股收益增长了惊人的21%。近三年来,EPS也出现了出色的65%的整体增长,得益于其短期业绩。因此,股东可能会对中期收益增长率感到满意。