RCM Technologies' (NASDAQ:RCMT) Solid Earnings May Rest On Weak Foundations

RCM Technologies' (NASDAQ:RCMT) Solid Earnings May Rest On Weak Foundations

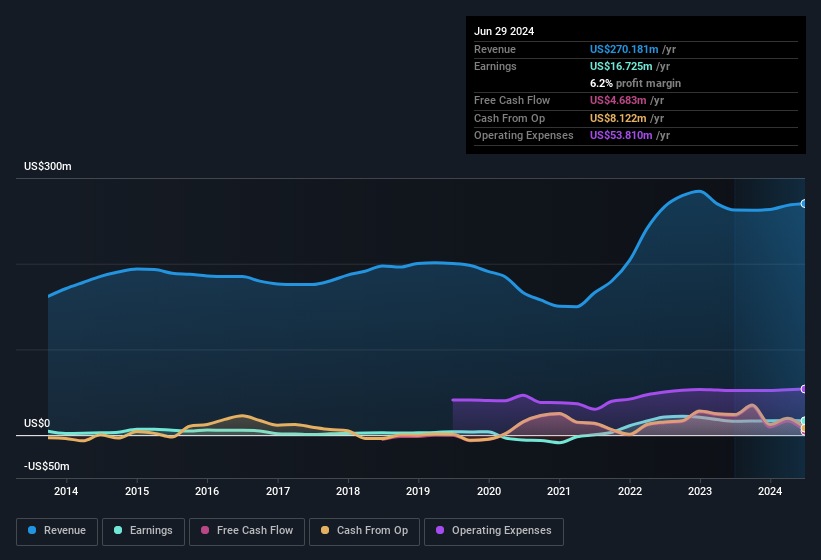

RCM Technologies, Inc.'s (NASDAQ:RCMT) robust recent earnings didn't do much to move the stock. We believe that shareholders have noticed some concerning factors beyond the statutory profit numbers.

RCm technologies, Inc.(納斯達克:RCMT)強勁的最新業績並沒有對股票產生太大影響。我們認爲,股東已經注意到了超出國家法定盈利數字的一些令人擔憂的因素。

A Closer Look At RCM Technologies' Earnings

RCm technologies業績的更深入分析

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. The ratio shows us how much a company's profit exceeds its FCF.

用於衡量公司如何將其利潤轉化爲自由現金流(FCF)的一個關鍵財務比率是預提帳戶。簡單地說,這個比率從淨利潤中減去FCF,然後將那個數字除以該期間公司的平均營運資產。該比率顯示了一個公司的利潤超過了其FCF的多少。

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

這意味着負的應計比率是一件好事,因爲它顯示公司帶來的自由現金流比其利潤所暗示的要多。雖然擁有正的應計比率不是問題,表明一定水平的非現金利潤,但高的應計比率可以說是一件壞事,因爲它表明紙面利潤與現金流不匹配。引用Lewellen和Resutek 2014年的一篇論文「具有更高應計的公司趨向於在未來盈利更少」。

RCM Technologies has an accrual ratio of 0.29 for the year to June 2024. Therefore, we know that it's free cashflow was significantly lower than its statutory profit, raising questions about how useful that profit figure really is. In fact, it had free cash flow of US$4.7m in the last year, which was a lot less than its statutory profit of US$16.7m. RCM Technologies shareholders will no doubt be hoping that its free cash flow bounces back next year, since it was down over the last twelve months. One positive for RCM Technologies shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

RCm technologies在2024年6月的年度計提比率爲0.29。因此,我們知道其自由現金流顯著低於其國家法定盈利,這引起了對該盈利數字實際有多有用的質疑。事實上,它在過去一年中的自由現金流爲470萬美元,遠低於其國家法定盈利的1670萬美元。RCm technologies股東無疑希望其自由現金流在明年反彈,因爲它在過去十二個月中下降了。RCm technologies股東的一個積極因素是,它的計提比率去年明顯改善,這表明它可能在未來恢復更強的現金轉換能力。如果情況確實如此,股東應該尋找相對於盈利改善的現金流。

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

這可能會讓您想知道分析師對未來盈利能力的預測。幸運的是,您可以單擊此處查看基於其估計的未來盈利能力的互動圖表。

Our Take On RCM Technologies' Profit Performance

我們對RCm technologies盈利業績的看法

RCM Technologies didn't convert much of its profit to free cash flow in the last year, which some investors may consider rather suboptimal. Because of this, we think that it may be that RCM Technologies' statutory profits are better than its underlying earnings power. But on the bright side, its earnings per share have grown at an extremely impressive rate over the last three years. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you want to do dive deeper into RCM Technologies, you'd also look into what risks it is currently facing. Case in point: We've spotted 2 warning signs for RCM Technologies you should be mindful of and 1 of these is a bit unpleasant.

在過去一年中,RCm technologies並沒有將其盈利轉化爲自由現金流,這可能對一些投資者來說是相當次優的。因此,我們認爲RCm technologies的法定盈利表現可能比其基本盈利能力更好。但好的方面是,其每股收益在過去三年中以極快的速度增長。歸根結底,要想正確理解公司,就必須考慮到不僅僅是以上因素。如果你想更深入地了解RCm technologies,你也應該了解它當前面臨的風險。例如,我們發現了2個RCm technologies警示標誌,你應該注意,其中一個有點不愉快。

This note has only looked at a single factor that sheds light on the nature of RCM Technologies' profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

這份說明只看了RCm technologies盈利性質的一個因素。但是還有很多其他方法可以了解你對一家公司的看法。例如,許多人認爲高股本回報率是股權的有利經濟指標,而其他人則喜歡「跟着錢走」並搜索內部人員正在購買的股票。儘管你可能需要做一些研究,但你可能會發現這個收集高股本回報率公司或者這個持有重要內幕人員的股票清單有用。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。