In the past two trading days, the prospect of a soft landing has received more boost, as the latest data shows that the consumer price index continues to slow down, and the retail sales, also known as the "terror data" in the United States, recorded a surprising surge in July; the operating income of products with 10-30 billion yuan in product structure were 401/1288/60 million yuan respectively.

Has the prospect of a soft landing really overwhelmed the narrative of recession?

Recently, the relief of favorable US economic data eased investors’ nerves. However, the prospects for economic and monetary policy are still extremely unclear, which means that the market may face more volatility.

In the past two trading days, the prospect of a soft landing has received more boost, as the latest data shows that the consumer price index continues to slow down, and the retail sales, also known as the "terror data" in the United States, recorded a surprising surge in July. However, some industry insiders pointed out that if you look closely, Thursday's retail sales report isn't as good as it seems.

The data from the US Department of Commerce shows that retail sales in July increased by 1% over the previous month, exceeding economists' expectations of 0.3%. But this is mainly due to the rebound in auto sales. In June, auto sales were hit by widespread cyber attacks on dealerships. If auto and related parts are not included, retail sales in July only increased by 0.4%.

At the same time, the industrial production data released by the Federal Reserve on Thursday showed weakness, with industrial output in July falling by 0.6% month-on-month. The Fed said interference caused by Hurricane Belle caused the figure to drop by about 0.3 percentage points. But even if this factor is excluded, the decline in July is worse than the expected -0.1%. Data from June was also revised downward.

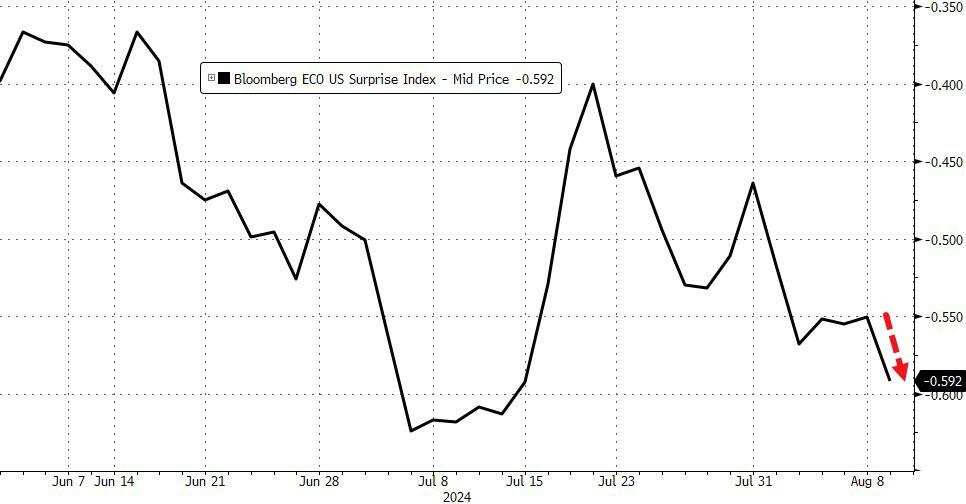

In fact, Zerohedge, a well-known financial blogger, vividly describes the overall performance of macro data in the United States yesterday:

The latest retail sales soared...This is due to a large number of historical revisions and a surge in auto sales...But auto production is experiencing its largest drop since the lockdown(undermining GDP expectations)...Home builder confidence is declining...Philadelphia Fed business prospects have plummeted...The New York Fed's manufacturing survey has been in contraction for the ninth consecutive month...Import and export price inflation is higher than expected...All of these are causing the US Economic Macro Surprise Index to fall to its lowest point in 2024...

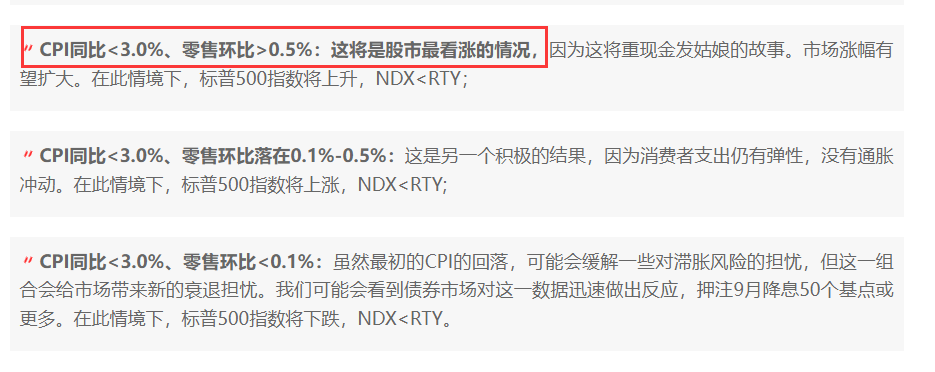

Of course, in the financial markets, people obviously didn't think too much about it last night, because a hot retail data was enough to make them feel happy. As we introduced in the preview before Wednesday, the performance of the two major indicators of CPI and retail sales this week fell into the most optimistic scenario made by JPMorgan:

In terms of stocks, the Dow rose more than 550 points overnight, and the Nasdaq and S&P 500 indices rose for the sixth consecutive trading day.

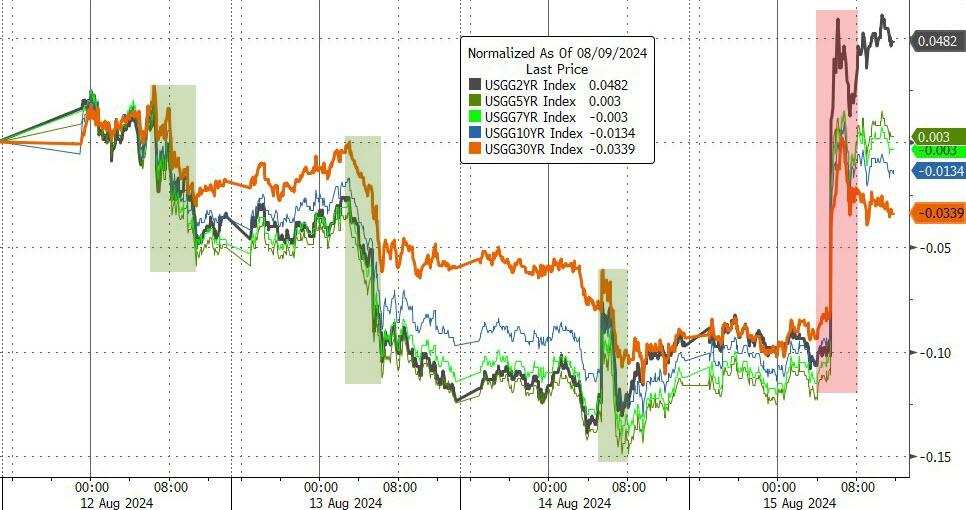

At the same time, strong US economic data also prompted traders to lower their expectations for a sharp cut in interest rates by the Federal Reserve this year. After the release of retail sales data, US bond yields soared, and the yield on the two-year US Treasury bonds sensitive to interest rate policies rose 12.7 basis points to 4.097% at the end of the session. The yield on 10-year US Treasury bonds rose 7.2 basis points to 3.912%.

Interest rate swap contracts show that traders further reduced their bets on a massive rate cut by the Federal Reserve in September, with pricing for the next month's rate cut of about 30 basis points. They now expect a total rate cut of 92 basis points in the remaining time in 2024, lower than the more than 100 basis points before the release of retail data.

Lindsay Rosner, the head of multiple fixed income departments at Goldman Sachs Asset Management, said:"The market is watching every data point closely and trading because we are nearing September, and a few months ago we were questioning when the Fed policy will really change. Trading around September is extremely crowded. You see this volatility because opinions on what the Fed can do are varied."

In any case, although this week's data shows that some worries about the prospects of an economic recession have been cooled down, it may not be the time for a complete turnaround. A comparison shows that although the US stock market has rebounded significantly in the past week, the magnitude of changes in bond yields and interest rate expectations is not large.

This means that the market may still encounter more disruptions similar to those experienced this summer. Recent experience shows how violent these disturbances can be: hawkish remarks from the Bank of Japan triggered a sharp rise in the yen, unwinding of arbitrage trades, and the most volatile week for stocks in years.

All of this reminds us that changes in monetary policy expectations can have huge chain reactions.

"Although Thursday's single-day increase was not small, it was relatively reasonable for us to recover a small part of the lost ground against the backdrop of the recent decline in yields," said Scott Pike, senior investment portfolio manager at Income Research & Management in Boston.

Editor/new