The AEM Holdings Ltd. (SGX:AWX) share price has fared very poorly over the last month, falling by a substantial 33%. For any long-term shareholders, the last month ends a year to forget by locking in a 61% share price decline.

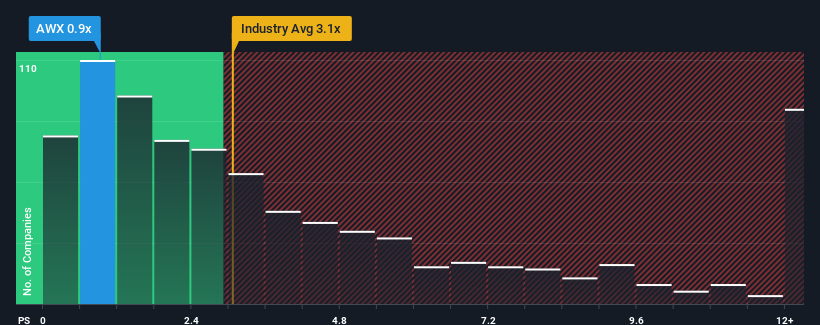

Even after such a large drop in price, it's still not a stretch to say that AEM Holdings' price-to-sales (or "P/S") ratio of 0.9x right now seems quite "middle-of-the-road" compared to the Semiconductor industry in Singapore, where the median P/S ratio is around 0.8x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

How AEM Holdings Has Been Performing

With revenue that's retreating more than the industry's average of late, AEM Holdings has been very sluggish. One possibility is that the P/S is moderate because investors think the company's revenue trend will eventually fall in line with most others in the industry. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Want the full picture on analyst estimates for the company? Then our free report on AEM Holdings will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, AEM Holdings would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, AEM Holdings would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 44% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 6.8% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 2.6% as estimated by the six analysts watching the company. Meanwhile, the broader industry is forecast to expand by 31%, which paints a poor picture.

With this information, we find it concerning that AEM Holdings is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

The Bottom Line On AEM Holdings' P/S

With its share price dropping off a cliff, the P/S for AEM Holdings looks to be in line with the rest of the Semiconductor industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It appears that AEM Holdings currently trades on a higher than expected P/S for a company whose revenues are forecast to decline. With this in mind, we don't feel the current P/S is justified as declining revenues are unlikely to support a more positive sentiment for long. If we consider the revenue outlook, the P/S seems to indicate that potential investors may be paying a premium for the stock.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for AEM Holdings with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of AEM Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.