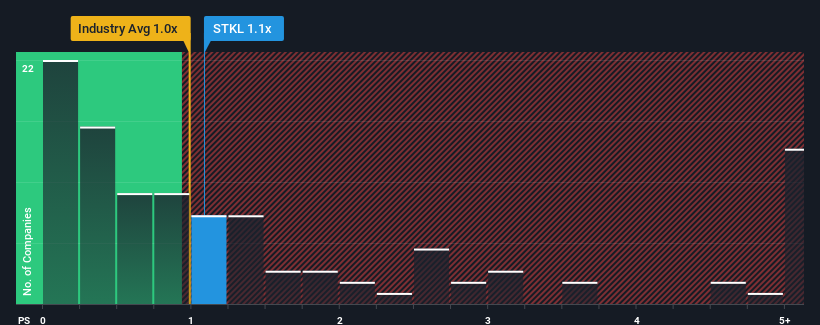

There wouldn't be many who think SunOpta Inc.'s (NASDAQ:STKL) price-to-sales (or "P/S") ratio of 1.1x is worth a mention when the median P/S for the Food industry in the United States is similar at about 1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

NasdaqGS:STKL Price to Sales Ratio vs Industry August 9th 2024

What Does SunOpta's Recent Performance Look Like?

SunOpta certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Keen to find out how analysts think SunOpta's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The P/S?

There's an inherent assumption that a company should be matching the industry for P/S ratios like SunOpta's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. Still, revenue has fallen 17% in total from three years ago, which is quite disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 11% during the coming year according to the seven analysts following the company. That's shaping up to be materially higher than the 2.9% growth forecast for the broader industry.

With this in consideration, we find it intriguing that SunOpta's P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that SunOpta currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

Having said that, be aware SunOpta is showing 1 warning sign in our investment analysis, you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. Still, revenue has fallen 17% in total from three years ago, which is quite disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. Still, revenue has fallen 17% in total from three years ago, which is quite disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

如果我們回顧過去一年的營收增長,該公司的增長率爲驚人的30%。然而,總的營收比三年前下降了17%,這非常令人失望。因此,我們不得不承認公司在增長營收方面做得不好。

如果我們回顧過去一年的營收增長,該公司的增長率爲驚人的30%。然而,總的營收比三年前下降了17%,這非常令人失望。因此,我們不得不承認公司在增長營收方面做得不好。