Unfortunately for some shareholders, the PLAYSTUDIOS, Inc. (NASDAQ:MYPS) share price has dived 29% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 61% share price decline.

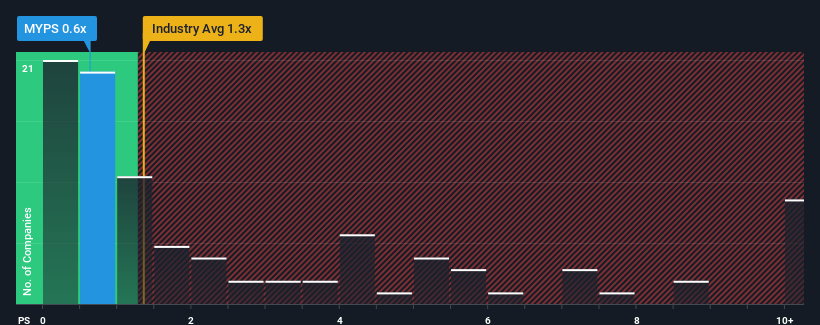

Since its price has dipped substantially, PLAYSTUDIOS may be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.6x, since almost half of all companies in the Entertainment industry in the United States have P/S ratios greater than 1.3x and even P/S higher than 5x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

NasdaqGM:MYPS Price to Sales Ratio vs Industry August 8th 2024

What Does PLAYSTUDIOS' Recent Performance Look Like?

PLAYSTUDIOS hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Keen to find out how analysts think PLAYSTUDIOS' future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Revenue Growth Forecasted For PLAYSTUDIOS?

PLAYSTUDIOS' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 1.9%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 8.9% overall rise in revenue. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next three years should bring diminished returns, with revenue decreasing 0.5% per year as estimated by the eight analysts watching the company. That's not great when the rest of the industry is expected to grow by 10% each year.

In light of this, it's understandable that PLAYSTUDIOS' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From PLAYSTUDIOS' P/S?

PLAYSTUDIOS' recently weak share price has pulled its P/S back below other Entertainment companies. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

With revenue forecasts that are inferior to the rest of the industry, it's no surprise that PLAYSTUDIOS' P/S is on the lower end of the spectrum. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless there's material change, it's hard to envision a situation where the stock price will rise drastically.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for PLAYSTUDIOS with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of PLAYSTUDIOS' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

PLAYSTUDIOS' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

PLAYSTUDIOS' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

PLAYSTUDIOS的市銷率對於一個預計交付有限增長並且重要的營業額表現較行業差的公司來說是典型的。

PLAYSTUDIOS的市銷率對於一個預計交付有限增長並且重要的營業額表現較行業差的公司來說是典型的。