On Monday, the US interest rate futures market finally saw a significant moment of 100% pricing for the Fed's interest rate cut in September by traders betting on when the Fed would cut rates. Driven by this, the spot gold price climbed to a new historic high for the first time in two months, and US stocks and bond prices rose across the board.

On July 17th, Caixin reported that on Monday, the US interest rate futures market finally saw a significant moment of 100% pricing for the Fed's interest rate cut in September by traders betting on when the Fed would cut rates.

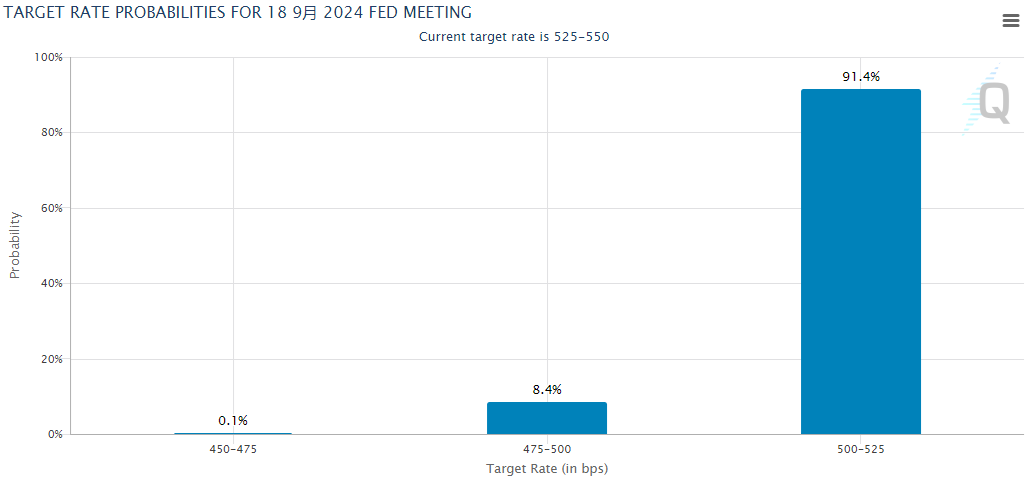

According to the CME Group's FedWatch tool, traders are currently forecasting a 91.4% probability that the Fed will cut the federal funds rate target range to 5.0%-5.25% (25 basis points) after its September interest rate meeting, and an 8.4% probability of cutting the rate to 4.75%-5% (a cumulative 50 basis points cut in July and September) and even an extremely remote possibility of a cumulative 75 basis point cut in July and September...

The widespread upsurge in rate cut expectations injected another shot of adrenaline into the market overnight - driven by this, the spot gold price climbed to a new historic high for the first time in two months, and US stocks and bond prices rose across the board. The S&P 500 index hit its 38th new high of the year while the Dow also rose more than 740 points in a single day and bond yields generally fell.

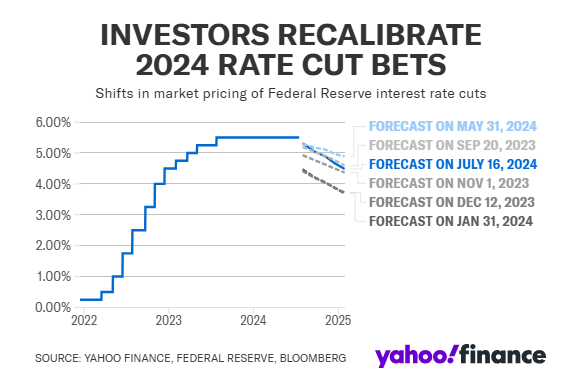

In fact, from the current situation, a cumulative three rate cuts by the Fed in the second half of this year are no longer a small probability event: the probability expectation of the rate swap market is already as high as 60%. If this scenario does occur, the Fed's move in June to reduce the number of rate cuts from 3 times to 1 time in the dot plot for the year seems like a "pointless change"...

So why has rate-cut expectations for the Fed suddenly surged recently?

The reasons behind it are obviously manifold - the most obvious is undoubtedly the change in tone by Fed officials. As we have previously reported, a series of indicators such as US economic, employment and inflation have shown a downward trend since the second quarter, and most of them actually support the Fed's early rate cut in the second half of the year. The reason why expectations of a rate cut have not changed much in the past few months is perhaps also due to the frequent "hawkish" talk by Fed officials, who have remained resilient.

Based on a number of speeches by Fed Chairman Powell over the past week, his attitude has obviously undergone a marked dovish shift. Powell reiterated on Monday that recent inflation data "does reinforce to some extent our confidence that inflation is returning to our symmetric 2 percent objective," and policymakers are now focused on full employment and price stability, rather than the former.

Economic data clearly still supports the above changes in Fed rate expectations - especially the two key indicators of non-farm employment and CPI released earlier this month. In terms of employment data, although the US unemployment rate remained relatively low at 4.1% in June, it has risen slightly each month for the past three months, and it was at a low of 3.4% in early 2023. The rise in unemployment has triggered a signal for the 'Sam rule' and has raised concerns about the risk of an economic recession.

In the field of inflation, after an unexpected rise in the first quarter, US inflation has remained moderate in the second quarter. The core Consumer Price Index (CPI), excluding volatile energy and food prices, rose only 0.1% month-on-month in June, the smallest increase since August 2021. The rise in rents in particular shows the long-awaited slowdown, which is expected to continue.

Given the combination of these two factors: the change in central bank rhetoric and data performance, it is no wonder that many well-known figures on Wall Street have recently changed their forecasts to bet on an earlier rate cut by the Fed. Many well-known figures such as Jan Hatzius, chief economist at Goldman Sachs, Mohamed El-Erian, dean of Cambridge's Queen's College, and Neil Dutta, chief economist at Renaissance Macro Research, have all recently pointed out that the risks of waiting for a rate cut by the Fed are increasing.

Hatzius said in a report released on Monday, "We believe there is a case for cutting rates as early as the July 30-31 FOMC meeting. If the reason for cutting rates is clear, why wait another seven weeks to cut rates?"

Morgan Stanley recently released a research report stating that the current monetary policy looks like it is only about half as tight in real interest rates as during Volcker's tightening in the 1980s, but inflation is only about a third of the 1980s - about 9% then compared with about 3% now. This should alone make investors worried about the Fed's overly tight monetary policy.

Of course, the mainstream market forecast still believes that the probability of the Fed rashly cutting rates at the meeting at the end of July - only two weeks away - is still relatively low at about 7.2%. Nevertheless, the Fed may still adjust its statement in the July monetary policy meeting to emphasize the improvement in inflation data, and Powell may give a speech at the global central bank annual meeting in Jackson Hole, Wyoming at the end of August that conveys a clear signal for September.

In any case, as the second half of the year approaches, it appears that the footsteps of the Federal Reserve's interest rate cut are getting closer. And in the next few months, we can also wait and see how the "interest rate trading" around the Fed's policy shift and the "Trump trading" around the US election will resonate and clash.

Editor/Somer