Roku (NASDAQ:ROKU) Shareholders Have Endured a 87% Loss From Investing in the Stock Three Years Ago

Roku (NASDAQ:ROKU) Shareholders Have Endured a 87% Loss From Investing in the Stock Three Years Ago

As every investor would know, not every swing hits the sweet spot. But you want to avoid the really big losses like the plague. So take a moment to sympathize with the long term shareholders of Roku, Inc. (NASDAQ:ROKU), who have seen the share price tank a massive 87% over a three year period. That'd be enough to cause even the strongest minds some disquiet. Furthermore, it's down 16% in about a quarter. That's not much fun for holders. We really hope anyone holding through that price crash has a diversified portfolio. Even when you lose money, you don't have to lose the lesson.

股市投資者都知道,股票市場並非總是充滿機會。但我們要儘量避免大幅度虧損的情況。所以爲長揸Roku, Inc. (納斯達克:ROKU) 股票的股東感到惋惜。股票價格在過去的三年中大幅縮水,其跌幅高達87%。這足以讓即使最堅強的投資者也會感到不安。不僅如此,在上個季度裏,其跌幅也達到了16%。這對持有人來說並不好過。我們真正希望那些在價格暴跌期間一直持有這隻股票的投資者有一個多元化的投資組合。即使你虧了錢,也不要失去教訓。

It's worthwhile assessing if the company's economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let's do just that.

值得評估公司的經濟狀況是否與這些不盡如人意的股東回報同時發展並步調一致,或者兩者之間是否存在差異。因此,讓我們來看看。

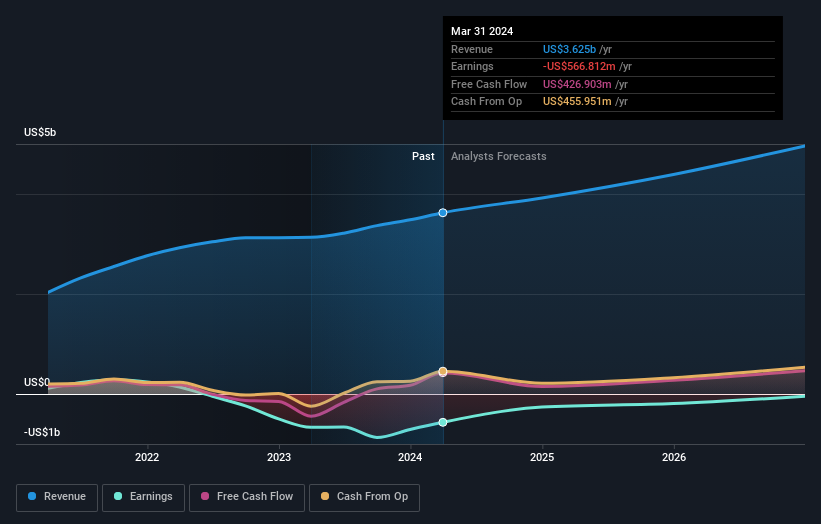

Given that Roku didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

考慮到Roku在過去的十二個月裏沒有實現盈利,我們將重點關注其營收增長情況以便快速了解其業務發展。在公司沒有盈利的情況下,我們通常希望看到良好的營收增長。可以想象,快速的營收增長,當持續下去時,通常會帶來快速的利潤增長。在過去的三年中,Roku實現了年複合15%的營收增長率。這是相當不錯的頂線增長率。因此,很難相信其每年下跌23% 的股價是由於營收造成的。更有可能的是市場對營收成本感到驚恐。這也是爲什麼投資者需要多元化的原因。即使一個虧損的公司實現了營收增長,也可能未能爲股東創造價值。

In the last three years, Roku saw its revenue grow by 15% per year, compound. That's a pretty good rate of top-line growth. So it's hard to believe the share price decline of 23% per year is due to the revenue. More likely, the market was spooked by the cost of that revenue. This is exactly why investors need to diversify - even when a loss making company grows revenue, it can fail to deliver for shareholders.

在過去的三年中,Roku的營收年複合增長率爲15%。這是一個相當不錯的頂線增長率。因此,很難相信其每年下跌23% 的股價是由於營收造成的。更有可能的是市場對營收成本感到驚恐。這也是爲什麼投資者需要多元化的原因。即使一個虧損的公司實現了營收增長,也可能未能爲股東創造價值。

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

下圖顯示了收益和營收隨時間變化的情況(如果你點擊圖像,可以看到更多細節):

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. So it makes a lot of sense to check out what analysts think Roku will earn in the future (free profit forecasts).

我們喜歡看到內部人在過去的十二個月裏購買了股票。即使如此,未來的盈利對於當前股東是否賺錢來說更加重要。因此,仔細了解分析師對Roku未來收益的預測(免費的利潤預測)是很有道理的。

A Different Perspective

不同的觀點

Investors in Roku had a tough year, with a total loss of 15%, against a market gain of about 25%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 2 warning signs for Roku that you should be aware of before investing here.

Roku的投資者度過了艱難的一年,遭受了15%的總虧損,而市場的收益約爲25%。然而,請記住,即使最好的股票有時也會在十二個月的時間內跑輸市場。遺憾的是,去年的表現標誌着一個不好的時期,股東面臨着每年總虧損7%的局面。我們知道巴隆·羅斯柴爾德曾說過投資者應該在“街頭流血時購買”,但我們警告投資者首先確保他們正在購買的是高質量的企業。我發現長期股價作爲企業績效的代理非常有趣。但是,要真正獲得洞察力,我們還需要考慮其他信息。例如,我們已經發現了Roku的2個警示信號,您在投資之前應該了解到這些信號。

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of undervalued small cap companies that insiders are buying.

還有很多其他的公司,公司的內部人士正在購買股票。你可能不想錯過這個免費的小市值公司的低估列表。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者,發送電子郵件至editorial-team (at) simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者發送電子郵件至editorial-team@simplywallst.com。

譯文內容由第三人軟體翻譯。