What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Ergo, when we looked at the ROCE trends at TJX Companies (NYSE:TJX), we liked what we saw.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for TJX Companies:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.30 = US$6.0b ÷ (US$30b - US$10b) (Based on the trailing twelve months to May 2024).

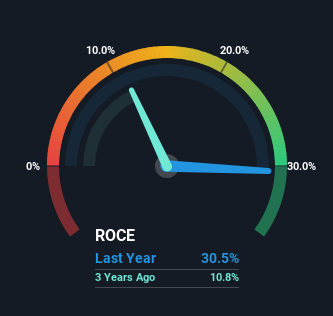

Thus, TJX Companies has an ROCE of 30%. That's a fantastic return and not only that, it outpaces the average of 13% earned by companies in a similar industry.

NYSE:TJX Return on Capital Employed June 16th 2024

Above you can see how the current ROCE for TJX Companies compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering TJX Companies for free.

What The Trend Of ROCE Can Tell Us

It's hard not to be impressed by TJX Companies' returns on capital. The company has employed 23% more capital in the last five years, and the returns on that capital have remained stable at 30%. Now considering ROCE is an attractive 30%, this combination is actually pretty appealing because it means the business can consistently put money to work and generate these high returns. You'll see this when looking at well operated businesses or favorable business models.

Our Take On TJX Companies' ROCE

In short, we'd argue TJX Companies has the makings of a multi-bagger since its been able to compound its capital at very profitable rates of return. And long term investors would be thrilled with the 119% return they've received over the last five years. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

TJX Companies does have some risks though, and we've spotted 1 warning sign for TJX Companies that you might be interested in.