Despite an already strong run, MediaCo Holding Inc. (NASDAQ:MDIA) shares have been powering on, with a gain of 102% in the last thirty days. The last month tops off a massive increase of 168% in the last year.

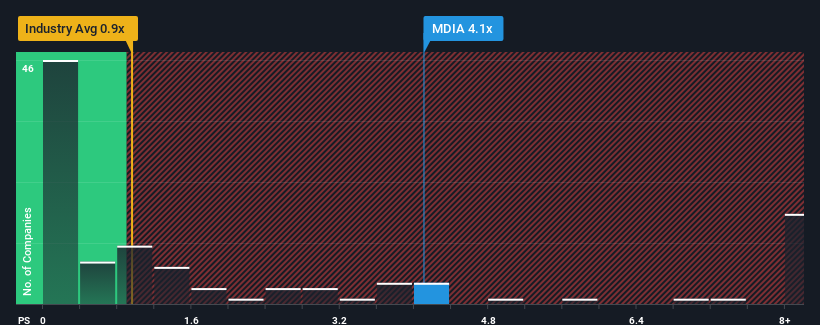

After such a large jump in price, given around half the companies in the United States' Media industry have price-to-sales ratios (or "P/S") below 0.9x, you may consider MediaCo Holding as a stock to avoid entirely with its 4.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

NasdaqCM:MDIA Price to Sales Ratio vs Industry June 16th 2024

How MediaCo Holding Has Been Performing

For instance, MediaCo Holding's receding revenue in recent times would have to be some food for thought. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on MediaCo Holding's earnings, revenue and cash flow.

Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as MediaCo Holding's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered a frustrating 16% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 15% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

In contrast to the company, the rest of the industry is expected to grow by 4.6% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this information, we find it concerning that MediaCo Holding is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What We Can Learn From MediaCo Holding's P/S?

Shares in MediaCo Holding have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that MediaCo Holding currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

And what about other risks? Every company has them, and we've spotted 3 warning signs for MediaCo Holding you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

The only time you'd be truly comfortable seeing a P/S as steep as MediaCo Holding's is when the company's growth is on track to outshine the industry decidedly.

The only time you'd be truly comfortable seeing a P/S as steep as MediaCo Holding's is when the company's growth is on track to outshine the industry decidedly.

當公司的增長有望顯著勝過行業時,您唯一會真正感到自在的情況就是市銷率與Mediaco Holding一樣高。

當公司的增長有望顯著勝過行業時,您唯一會真正感到自在的情況就是市銷率與Mediaco Holding一樣高。