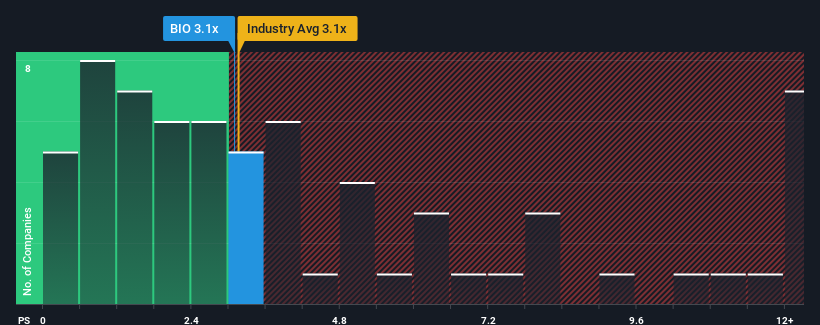

With a median price-to-sales (or "P/S") ratio of close to 3.1x in the Life Sciences industry in the United States, you could be forgiven for feeling indifferent about Bio-Rad Laboratories, Inc.'s (NYSE:BIO) P/S ratio, which comes in at about the same. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

NYSE:BIO Price to Sales Ratio vs Industry June 16th 2024

What Does Bio-Rad Laboratories' Recent Performance Look Like?

Bio-Rad Laboratories has been struggling lately as its revenue has declined faster than most other companies. It might be that many expect the dismal revenue performance to revert back to industry averages soon, which has kept the P/S from falling. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Want the full picture on analyst estimates for the company? Then our free report on Bio-Rad Laboratories will help you uncover what's on the horizon.

Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, Bio-Rad Laboratories would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 6.3% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 3.5% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 3.9% per annum as estimated by the five analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 6.9% per annum, which is noticeably more attractive.

In light of this, it's curious that Bio-Rad Laboratories' P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What We Can Learn From Bio-Rad Laboratories' P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

When you consider that Bio-Rad Laboratories' revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Bio-Rad Laboratories with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on Bio-Rad Laboratories, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com