看涨期权(Call Option)是一种金融合约,赋予买方在特定时期内以特定价格购买股票、债券、商品或其他资产或工具的权利,但没有义务。看涨期权卖方则有义务在买方行使期权时出售该资产。看涨期权的买方在标的资产价格上涨时获利,而卖方则在标的资产价格下跌或期权到期时获利。看涨期权的收益取决于标的资产价格、执行价格、到期日和权利金等因素。当标的资产价格上涨时,看涨期权买方就会获利。如果标的资产的价格在到期时跌破执行价格,卖方将从溢价中获利,因为买方通常不会执行期权。在美股市场,每份看涨期权(call option)通常代表100股基础股票。因此,如果购买或卖出一份看涨期权合约,你实际上是购买或卖出100股相关股票的权利。

看涨期权(Call Option)是一种金融合约,赋予买方在特定时期内以特定价格购买股票、债券、商品或其他资产或工具的权利,但没有义务。看涨期权卖方则有义务在买方行使期权时出售该资产。看涨期权的买方在标的资产价格上涨时获利,而卖方则在标的资产价格下跌或期权到期时获利。看涨期权的收益取决于标的资产价格、执行价格、到期日和权利金等因素。当标的资产价格上涨时,看涨期权买方就会获利。如果标的资产的价格在到期时跌破执行价格,卖方将从溢价中获利,因为买方通常不会执行期权。在美股市场,每份看涨期权(call option)通常代表100股基础股票。因此,如果购买或卖出一份看涨期权合约,你实际上是购买或卖出100股相关股票的权利。“大道無形我有型”是知名投資人段永平的雪球ID,他以投資蘋果和貴州茅台聞名,其言論常引發熱議。記者梳理段永平最近的言論發現,他最近的帖子集中在對$蘋果 (AAPL.US)$股票走勢的看法和他的投資策略方面,包括賣出看漲期權,如果被行權,就賣出等價的看跌期權,等待回調。

針對蘋果股價,段永平表示,“目前這個價位可以考慮短期一些的了。其實我長短都會賣一些的。”段永平認爲,目前30年的國債利率是4.44%,相當於22.5倍的PE,這也是持有任何公司的機會成本。短期國債的利率是5.36%,相當於18.66倍的PE。“持有=買入,有點糾結了。”

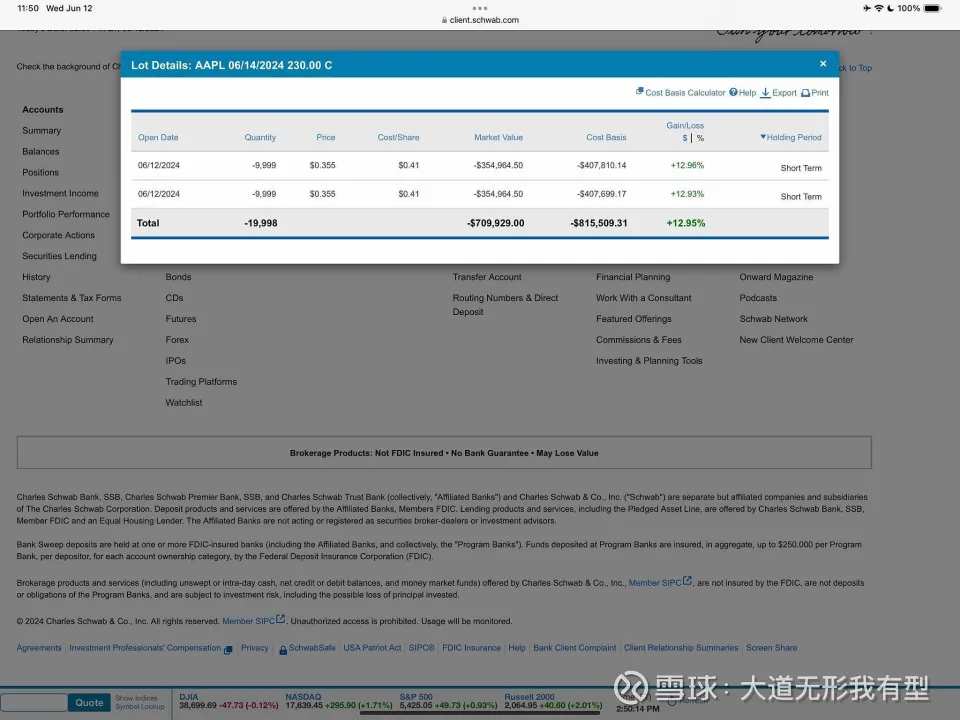

根據段永平貼出的交割單,他在2024年6月12日賣出了19998份蘋果公司2024年6月14日到期的230美元看漲期權,期權的價格爲0.355美元,總市場價值爲70.99萬美元,總成本爲81.55萬美元。

看漲期權(Call Option)是一種金融合約,賦予買方在特定時期內以特定價格購買股票、債券、商品或其他資產或工具的權利,但沒有義務。看漲期權賣方則有義務在買方行使期權時出售該資產。看漲期權的買方在標的資產價格上漲時獲利,而賣方則在標的資產價格下跌或期權到期時獲利。看漲期權的收益取決於標的資產價格、執行價格、到期日和權利金等因素。當標的資產價格上漲時,看漲期權買方就會獲利。如果標的資產的價格在到期時跌破執行價格,賣方將從溢價中獲利,因爲買方通常不會執行期權。在美股市場,每份看漲期權(call option)通常代表100股基礎股票。因此,如果購買或賣出一份看漲期權合約,你實際上是購買或賣出100股相關股票的權利。

看漲期權(Call Option)是一種金融合約,賦予買方在特定時期內以特定價格購買股票、債券、商品或其他資產或工具的權利,但沒有義務。看漲期權賣方則有義務在買方行使期權時出售該資產。看漲期權的買方在標的資產價格上漲時獲利,而賣方則在標的資產價格下跌或期權到期時獲利。看漲期權的收益取決於標的資產價格、執行價格、到期日和權利金等因素。當標的資產價格上漲時,看漲期權買方就會獲利。如果標的資產的價格在到期時跌破執行價格,賣方將從溢價中獲利,因爲買方通常不會執行期權。在美股市場,每份看漲期權(call option)通常代表100股基礎股票。因此,如果購買或賣出一份看漲期權合約,你實際上是購買或賣出100股相關股票的權利。

值得注意的是,截至當地時間6月13日收盤,蘋果股價漲0.55%,報214.24美元/股,創歷史新高,總市值3.29萬億美元,以微弱的優勢反超微軟,重新奪回了全球市值第一的“寶座”。此前一交易日,蘋果股價盤中一度突破220美元/股,目前蘋果股價距離230美元的行權價仍有超過7%的漲幅。

在蘋果股價不斷創出新高的同時,段永平的另一“偏愛”貴州茅台近日則持續走低,對於有網友問其會否將蘋果換成貴州茅台時,段永平表示不會換貴州茅台,認爲其治理水平無法與蘋果相提並論。

段永平旗下的投資公司最新公佈的2024年第一季度13F報告顯示,其管理的13F證券總值爲141.96億美元,最大的持倉是蘋果,位列蘋果第十九大機構股東,持有股票數量爲6458萬股。前五大持倉裏,蘋果持倉比例78.01%,伯克希爾·哈撒韋公司持倉比例12.12%,谷歌持倉比例5.5%,阿里巴巴持倉比例2.98%,迪士尼持倉比例0.65%。

截至一季度末,蘋果公司的持股機構數4493家,其中增持機構爲1612家,較上期增長了8.04%;減持機構數2154家;有516家機構新進持有蘋果股票;同時也有452家機構選擇退出。機構持股總數爲912040.73萬股,相較上期減少了4.39%。機構持股佔比爲59.46%,環比上期(61.70%)下降。

在具體的機構持股明細中,Vanguard Group Inc仍然是最大的持股機構,持股數量爲131885.96萬股,持股市值爲2261.58億美元,佔比8.60%。BlackRock Inc緊隨其後,持股數量爲104191.94萬股,佔比6.79%。值得注意的是巴菲特的Berkshire Hathaway的持股數量減少了11619.16萬股,降幅達到了12.83%。

不過,二季度以來,蘋果股價持續上漲,截至目前,較階段低點最高漲幅超過30%。

分析師認爲,儘管蘋果的人工智能對用戶來說是一個巨大的進步,但對於投資者來說,其盈利潛力尚不明確。儘管蘋果公司在WWDC上發佈了新的AI系統Apple Intelligence,以及與OpenAI合作將ChatGPT-4.0集成到Siri中,引發了股價大幅上漲,但蘋果股票目前的價格仍然過高,存在泡沫。從蘋果公司的營收增長、EBIT利潤率、資本支出、加權平均資本成本(WACC)等方面進行分析,即使在非常樂觀的情況下,蘋果股票也存在12.5%的估值溢價。市場可能過於樂觀,主要原因是:忽略了AI集成帶來的數據安全風險,儘管Elon Musk的言論可能不會對蘋果的銷量造成重大影響,但用戶的擔憂依然存在。忽略了蘋果股票的股息收益率相對較低,以及公司股票回購的潛在增長空間有限。忽略了蘋果公司盈利增長的歷史週期性模式,以及公司向服務型收入轉變的可能性。

該分析也表示,他的分析模型存在一些風險,例如WACC假設可能過於保守,以及蘋果股票的EV/FCF倍數可能繼續上升。但是,即使考慮到這些風險,依然認爲蘋果股票目前的價格過高,因此維持對蘋果股票的“賣出”評級。

編輯/Jeffrey

市場熱點不斷,想加入投資行列,但覺得仲差少少知識同基本功?立即click參加投資教程,特邀用戶更可得到高達$2000驚喜獎賞>>

*活動對象:限年滿18歲以上,香港地區已註冊富途APP但未開立證券帳戶的特邀存量用戶參與