Revenues Not Telling The Story For Indie Semiconductor, Inc. (NASDAQ:INDI) After Shares Rise 29%

Revenues Not Telling The Story For Indie Semiconductor, Inc. (NASDAQ:INDI) After Shares Rise 29%

indie Semiconductor could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

indie Semiconductor could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock. indie Semiconductor, Inc. (NASDAQ:INDI) shares have had a really impressive month, gaining 29% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 31% over that time.

自INDI股票在前一段時間經歷動盪期後,indie Semiconductor, Inc. (NASDAQ:INDI)股票在上個月有了非常好的表現,漲幅達到29%。然而,儘管過去一個月的收益不俗,但股票在過去的一年裏仍然下跌了31%。

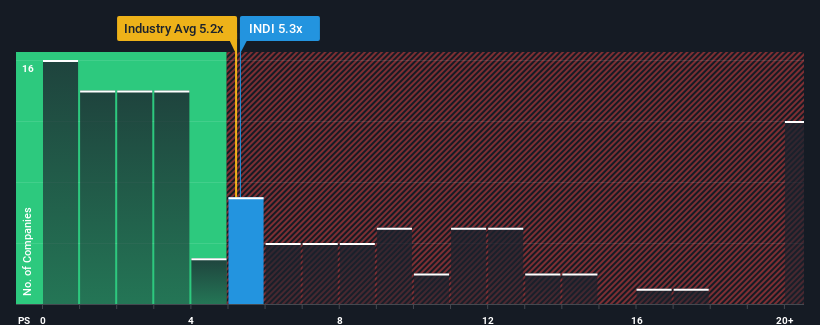

Although its price has surged higher, there still wouldn't be many who think indie Semiconductor's price-to-sales (or "P/S") ratio of 5.3x is worth a mention when the median P/S in the United States' Semiconductor industry is similar at about 5.2x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

儘管INDI股票的價格較高,但在美國半導體行業中的P/S中位數約爲5.2倍,因此其5.3倍的市銷率並不值得一提。雖然這可能不會引起任何人的注意,但如果市銷率沒有得到證明,投資者可能會錯失潛在機會或無視即將出現的失望。

NasdaqCM:INDI Price to Sales Ratio vs Industry June 11th 2024

NasdaqCM:INDI市銷率與業內比較於2024年6月11日。

How indie Semiconductor Has Been Performing

indie Semiconductor 近況表現。

indie Semiconductor could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

近來,indie Semiconductor的營收增長不如大多數其他公司,因此該公司運營狀況可能需要得到改善。如果運營狀況沒有得到改變,投資者可能會因過高的市銷率而遭受損失。

Keen to find out how analysts think indie Semiconductor's future stacks up against the industry? In that case, our free report is a great place to start.

想知道分析師們如何與業界競爭的嗎?那麼,我們的免費報告是一個很好的開始。

Do Revenue Forecasts Match The P/S Ratio?

營收預測與市銷率相符嗎?

The only time you'd be comfortable seeing a P/S like indie Semiconductor's is when the company's growth is tracking the industry closely.

只有當公司的發展和行業相吻合時,才能接受像indie Semiconductor這樣的市銷率。

Taking a look back first, we see that the company grew revenue by an impressive 82% last year. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

回顧過去,我們可以看到該公司去年營收增長了82%。令人驚歎的是,三年的營收增長已經成倍增長,部分原因是過去12個月的營收增長。因此,股東們將會對這些中期的營收增長率感到非常高興。

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 26% over the next year. With the industry predicted to deliver 40% growth, the company is positioned for a weaker revenue result.

展望未來,有八位分析師預測該公司的營收將在未來一年內增長26%。由於行業預計將實現40%的增長,因此該公司將面臨較弱的營收業績。

With this in mind, we find it intriguing that indie Semiconductor's P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

考慮到這一點,我們發現indie Semiconductor的市銷率與業內同行相差不大。看來大多數投資者忽略了相當有限的增長預期,並願意支付溢價來接觸股票。維持這些價格將很難實現,因爲這種營收增長水平可能會最終拖累股價。

What We Can Learn From indie Semiconductor's P/S?

從indie Semiconductor的市銷率中我們可以學到什麼?

indie Semiconductor appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

indie Semiconductor似乎又受到了青睞,強勁的價格上漲使得其市銷率與業內其他公司保持一致。我們認爲市銷率的作用不是作爲估值工具,而是用於衡量當前的投資者情緒和未來的預期。

When you consider that indie Semiconductor's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

當我們考慮到indie Semiconductor的營收增長預期與整個行業相比相對較弱時,很容易就可以看出爲什麼其當前的市銷率不符合預期。當我們看到營收前景相對於行業相對較弱的公司時,我們認爲股價有下跌的風險,從而將市銷率適度降低。這將爲股東的投資帶來風險,並使潛在投資者面臨支付不必要的溢價的危險。

We don't want to rain on the parade too much, but we did also find 2 warning signs for indie Semiconductor that you need to be mindful of.

爲了不過分影響股價,在此我們只發現了indie Semiconductor的2個警告信號。

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

當然,盈利良好,具有長期強勁盈利增長曆史的公司通常是較爲安全的選擇。因此,你可能希望查看這些具有合理市盈率和強勁盈利增長表現的其他公司的免費數據合集。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關注內容?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。