Even After Rising 8.0% This Past Week, Lexicon Pharmaceuticals (NASDAQ:LXRX) Shareholders Are Still Down 69% Over the Past Five Years

Even After Rising 8.0% This Past Week, Lexicon Pharmaceuticals (NASDAQ:LXRX) Shareholders Are Still Down 69% Over the Past Five Years

Generally speaking long term investing is the way to go. But along the way some stocks are going to perform badly. For example the Lexicon Pharmaceuticals, Inc. (NASDAQ:LXRX) share price dropped 69% over five years. We certainly feel for shareholders who bought near the top. And we doubt long term believers are the only worried holders, since the stock price has declined 28% over the last twelve months. The falls have accelerated recently, with the share price down 23% in the last three months.

一般情況下,長期投資是首選。但在此過程中,某些股票可能表現不佳。例如,Lexicon Pharmaceuticals,Inc.(納斯達克股票代碼:LXRX)的股價在五年內下跌了69%。我們當然爲在高位買入的股東感到難過。我們認爲不僅是長期的支持者,股東們對股價下跌28%的情況也感到擔憂。近期跌幅有所加速,股價在過去三個月下跌了23%。

On a more encouraging note the company has added US$51m to its market cap in just the last 7 days, so let's see if we can determine what's driven the five-year loss for shareholders.

值得鼓勵的是,該公司在過去7天內已爲其市值增加了5100萬美元,因此讓我們看看我們是否可以確定是什麼導致了股東的五年損失。

We don't think Lexicon Pharmaceuticals' revenue of US$2,310,000 is enough to establish significant demand. This state of affairs suggests that venture capitalists won't provide funds on attractive terms. So it seems that the investors focused more on what could be, than paying attention to the current revenues (or lack thereof). It seems likely some shareholders believe that Lexicon Pharmaceuticals has the funding to invent a new product before too long.

我們認爲Lexicon Pharmaceuticals的營業收入231萬美元不足以建立顯着的需求。這種情況表明,風險投資家不會提供有吸引力的資金。因此,投資者更注重可能的事情,而不是關注當前的營業收入(或缺乏收入)。看起來,一些股東相信Lexicon Pharmaceuticals有足夠的資金在不久的將來發明新產品。

Companies that lack both meaningful revenue and profits are usually considered high risk. There is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets to raise equity. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies do very well over the long term, others become hyped up by promoters before eventually falling back down to earth, and going bankrupt (or being recapitalized). Lexicon Pharmaceuticals has already given some investors a taste of the bitter losses that high risk investing can cause.

通常被認爲缺乏顯着營業收入和利潤的公司是高風險的。他們通常有很大的機會需要更多的資金進行業務發展,使它們處於依靠資本市場來籌集股本的境地。因此,股價本身影響着股票的價值(因爲它決定了資本成本)。雖然有些此類公司的表現非常好,但其他公司則會受到推銷者的炒作,然後最終回到實際情況,破產或者被重組。Lexicon Pharmaceuticals已經讓一些投資者品嚐到了高風險投資所帶來的慘痛損失。

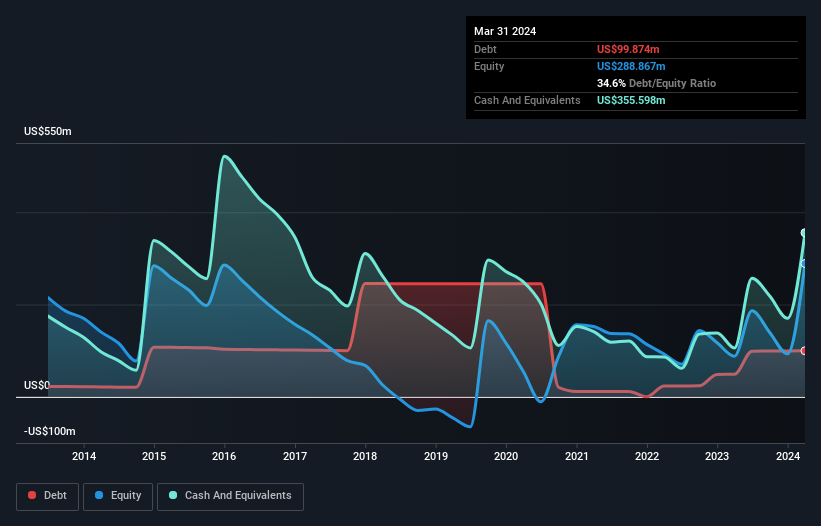

When it last reported its balance sheet in March 2024, Lexicon Pharmaceuticals had cash in excess of all liabilities of US$227m. While that's nothing to panic about, there is some possibility the company will raise more capital, especially if profits are not imminent. With the share price down 11% per year, over 5 years , it seems likely that the need for cash is weighing on investors' minds. You can see in the image below, how Lexicon Pharmaceuticals' cash levels have changed over time (click to see the values).

當Lexicon Pharmaceuticals在2024年3月最新報告資產負債表時,現金儲備超過所有負債的227美元。雖然這無需恐慌,但如果利潤未能及時實現,該公司有一定可能會籌集更多資金。隨着股價在過去5年中以每年11%的速度下跌,看起來需要現金的需求正在影響投資者的思維。您可以在下面的圖表中查看Lexicon Pharmaceuticals的現金水平如何隨時間變化(單擊以查看值)。

It can be extremely risky to invest in a company that doesn't even have revenue. There's no way to know its value easily. What if insiders are ditching the stock hand over fist? I would feel more nervous about the company if that were so. It costs nothing but a moment of your time to see if we are picking up on any insider selling.

投資沒有營收的公司可能非常危險。我們無法輕易地了解它的價值。如果內部人員大量拋售股票會怎麼樣呢?如果是這樣,我會對公司更加緊張。請花費一點時間,看看我們是否有內幕交易。

A Different Perspective

不同的觀點

Lexicon Pharmaceuticals shareholders are down 28% for the year, but the market itself is up 23%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 11% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Lexicon Pharmaceuticals better, we need to consider many other factors. Even so, be aware that Lexicon Pharmaceuticals is showing 4 warning signs in our investment analysis , you should know about...

Lexicon Pharmaceuticals的股東今年下降了28%,但市場本身上漲了23%。即使好股票的股價有時也會下跌,但在對業務的基本指標進行改進之前,我們希望看到業務表現得更好。不幸的是,去年的表現可能表明尚未解決的挑戰,因爲它比過去五年的年化損失11%更差。我們知道Baron Rothschild曾說過投資者應該“在街頭有血泊時買入”,但我們提醒投資者首先要確保他們正在購買高質量的企業。跟蹤長期的股價表現總是很有趣的,但要更好地了解Lexicon Pharmaceuticals,我們需要考慮許多其他因素。儘管如此,請注意,在我們的投資分析中,Lexicon Pharmaceuticals顯示出4個警告信號,您應該了解......

Lexicon Pharmaceuticals is not the only stock insiders are buying. So take a peek at this free list of small cap companies at attractive valuations which insiders have been buying.

Lexicon Pharmaceuticals並不是內部人員正在購買的唯一股票。所以來看看這個免費的小盤公司市值看起來很有吸引力,而內部人員一直在購買。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者,發送電子郵件至editorial-team (at) simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。