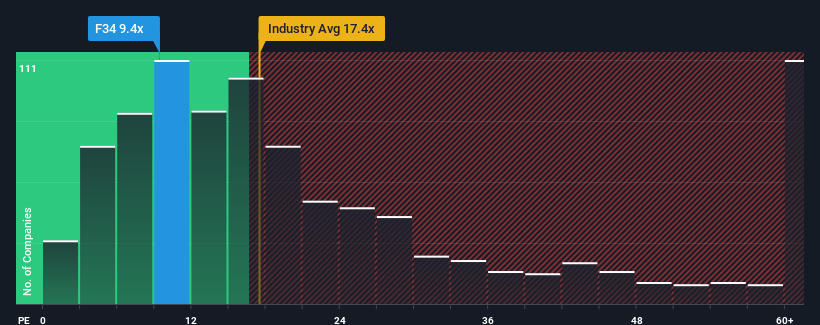

Wilmar International Limited's (SGX:F34) price-to-earnings (or "P/E") ratio of 9.4x might make it look like a buy right now compared to the market in Singapore, where around half of the companies have P/E ratios above 12x and even P/E's above 22x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Wilmar International has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

SGX:F34 Price to Earnings Ratio vs Industry June 10th 2024 Want the full picture on analyst estimates for the company? Then our free report on Wilmar International will help you uncover what's on the horizon.

How Is Wilmar International's Growth Trending?

Wilmar International's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Retrospectively, the last year delivered a frustrating 36% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 7.6% per year as estimated by the analysts watching the company. With the market predicted to deliver 8.5% growth each year, the company is positioned for a comparable earnings result.

With this information, we find it odd that Wilmar International is trading at a P/E lower than the market. It may be that most investors are not convinced the company can achieve future growth expectations.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Wilmar International's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Wilmar International (1 is concerning) you should be aware of.

You might be able to find a better investment than Wilmar International. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Wilmar International Limited(SGX:F34)的市盈率爲9.4x,與新加坡市場上市盈率在12x以上的公司約半數和22x以上的公司相比,似乎具有購買價值。然而,低市盈率背後可能有其原因,需要進一步調查以判斷是否合理。