Last week saw the newest first-quarter earnings release from Lululemon Athletica Inc. (NASDAQ:LULU), an important milestone in the company's journey to build a stronger business. Lululemon Athletica reported US$2.2b in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of US$2.54 beat expectations, being 5.1% higher than what the analysts expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Lululemon Athletica after the latest results.

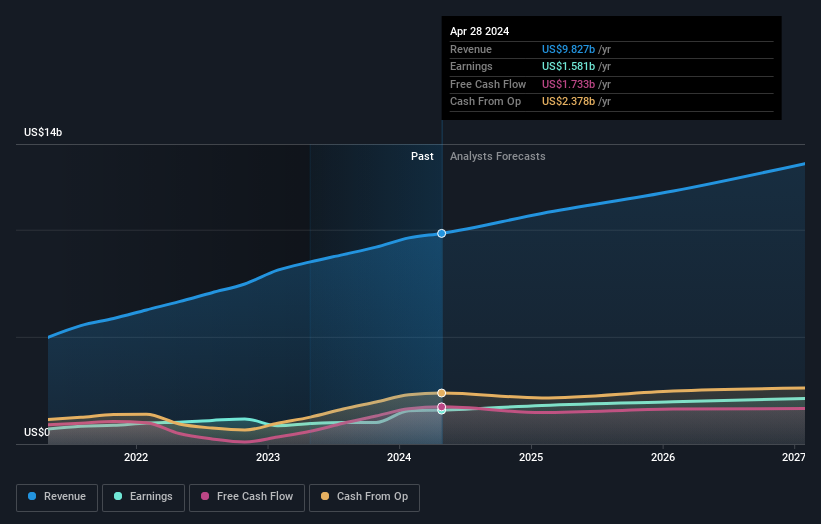

NasdaqGS:LULU Earnings and Revenue Growth June 8th 2024

Taking into account the latest results, the most recent consensus for Lululemon Athletica from 34 analysts is for revenues of US$10.8b in 2025. If met, it would imply a notable 9.5% increase on its revenue over the past 12 months. Per-share earnings are expected to grow 14% to US$14.39. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$10.8b and earnings per share (EPS) of US$14.19 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

With no major changes to earnings forecasts, the consensus price target fell 5.5% to US$405, suggesting that the analysts might have previously been hoping for an earnings upgrade. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Lululemon Athletica, with the most bullish analyst valuing it at US$525 and the most bearish at US$240 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Lululemon Athletica's past performance and to peers in the same industry. We would highlight that Lululemon Athletica's revenue growth is expected to slow, with the forecast 13% annualised growth rate until the end of 2025 being well below the historical 23% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.3% per year. So it's pretty clear that, while Lululemon Athletica's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Lululemon Athletica's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Lululemon Athletica. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Lululemon Athletica analysts - going out to 2027, and you can see them free on our platform here.

We also provide an overview of the Lululemon Athletica Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

上週,Lululemon Athletica Inc.(納斯達克股票代碼:LULU)發佈了最新的第一季度業績,這是該公司建立更強大業務過程中的一個重要里程碑。Lululemon Athletica公佈的收入爲22億美元,與分析師的預測大致一致,儘管2.54美元的法定每股收益(EPS)超出預期,比分析師的預期高出5.1%。對於投資者來說,盈利是一個重要時刻,因爲他們可以追蹤公司的業績,查看分析師對明年的預測,看看對公司的情緒是否發生了變化。讀者會很高興得知我們已經彙總了最新的法定預測,以了解分析師在最新業績公佈後是否改變了對Lululemon Athletica的看法。

納斯達克GS: LULU 2024年6月8日收益和收入增長

考慮到最新業績,34位分析師對Lululemon Athletica的最新共識是,2025年的收入爲108億美元。如果得到滿足,這意味着其收入在過去12個月中將顯著增長9.5%。每股收益預計將增長14%,至14.39美元。然而,在最新業績公佈之前,分析師曾預計2025年收入爲108億美元,每股收益(EPS)爲14.19美元。因此,很明顯,儘管分析師已經更新了估計,但在最新業績公佈後,對該業務的預期沒有重大變化。

由於收益預測沒有重大變化,共識目標股價下降了5.5%,至405美元,這表明分析師此前可能一直希望收益上調。但是,這並不是我們可以從這些數據中得出的唯一結論,因爲一些投資者在評估分析師目標股價時也喜歡考慮估計值的差異。對Lululemon Athletica的看法各不相同,最看漲的分析師將其估值爲525美元,最看跌的爲每股240美元。這是相當廣泛的估計,表明分析師正在預測該業務的各種可能結果。

這些估計很有趣,但是在查看預測與Lululemon Athletica過去的表現以及與同一行業的同行進行比較時,可以更粗略地描述一些細節。我們要強調的是,預計Lululemon Athletica的收入增長將放緩,預計到2025年底爲13%的年化增長率將遠低於過去五年中歷史上23%的年增長率。將其與業內其他有分析師報道的公司並列,預計這些公司的收入(總計)每年將增長6.3%。因此,很明顯,儘管預計Lululemon Athletica的收入增長將放緩,但預計其增長速度仍將超過該行業本身。

底線

要了解的最重要的一點是,市場情緒沒有重大變化,分析師再次確認該業務的表現符合他們先前的每股收益預期。幸運的是,他們還再次確認了收入數字,表明收入符合預期。此外,我們的數據表明,收入的增長速度預計將快於整個行業。共識目標股價大幅下降,最新業績似乎並未讓分析師放心,這導致對Lululemon Athletica未來估值的估計降低。

考慮到這一點,我們不會很快就Lululemon Athletica得出結論。長期盈利能力比明年的利潤重要得多。多位Lululemon Athletica分析師估計,到2027年,你可以在我們的平台上免費查看。

我們還在這裏概述了Lululemon Athletica董事會和首席執行官的薪酬和公司任期,以及內部人士是否一直在購買該股票。