The weather is good today The weather is good today.

According to Goldman Sachs, Taiwan Semiconductor may increase wafer prices by 5% in 2025 to achieve its gross margin target of 53%. The average selling price of 3nm wafers is expected to rise by 11% in the next two years, and the average selling price of 4nm wafers is expected to rise by 3%. The packaging price of CoWoS is expected to rise by 20%.

TOP20 US stock trading volume$Taiwan Semiconductor (TSM.US)$After the shareholder meeting, the new chairman of TSMC, Wei Che-Chia, hinted that the company is considering raising the prices of its AI chip manufacturing services, and said that he had discussed the issue with Huang Renxun, the founder and CEO of Nvidia.

Huang Renxun subsequently publicly acknowledged the value of TSMC in chip foundry, stating that "TSMC's wafer prices are indeed too low, and TSMC's contribution to the world and the technology industry is underestimated due to its low financial performance."

"TSMC's wafer prices are indeed too low, and TSMC's contribution to the world and the technology industry is underestimated due to its low financial performance."

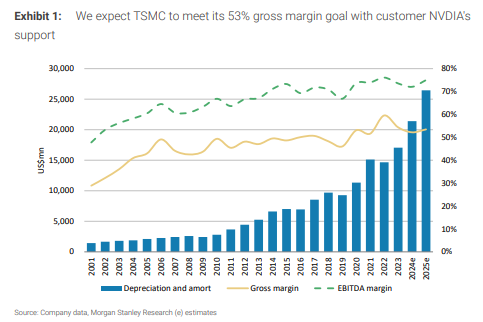

Based on this, on June 5th, the analysis team led by Morgan Stanley analyst Charlie Chan released a research report, predicting that TSMC may raise wafer prices by 5% in 2025 to maintain its gross margin at or above 53%, and stating that if Nvidia accepts the price increase, other key AI customers may also follow suit.

Given the price of NVIDIA chips and TSMC's important role in their production, Wei Zhejia said that it is normal to raise production costs, and "anyone at home could come up with this strategy."

In 2025, there may be a 5% increase, and the average selling price of 3nm wafers will rise by 11%.

Morgan Stanley believes that in order to achieve the target gross margin of 53% or above, TSMC may have to increase prices to pass on the high cost of US wafer plants.

The report stated that based on TSMC's history of raising prices by 10% in 2022 and 5% in 2023, a 5% increase in 2025 is "possible."

The report pointed out that Nvidia is TSMC's main customer, and its orders can account for 10% of the latter's revenue this year. If Nvidia accepts TSMC's plan to raise prices, it means that Nvidia's management recognizes the reliability of TSMC, and it is expected that other downstream chip manufacturers will follow suit in September or October this year.

Therefore, Morgan Stanley predicts that within the next two years, the average selling price of 3nm wafers will rise by 11%, the average selling price of 4nm wafers will rise by 3%, and the price of CoWoS packaging will rise by 20%.

Based on this, Morgan Stanley predicts that TSMC's gross margin will recover to 53-54% in 2025.

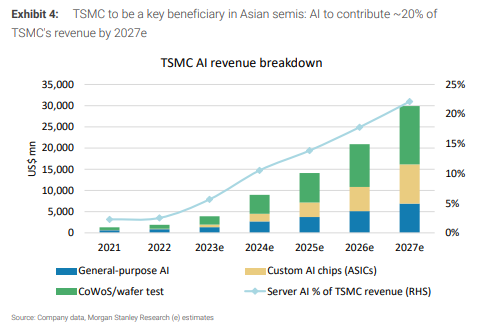

By 2025, AI revenue will contribute more than 20%.

At the same time, the demand for AI chips remains strong. The report predicts that TSMC will increase its CoWoS capacity by more than twice in 2024, and some packaging processes may even be outsourced to other backend foundries, and customer demand may be difficult to meet.

The report pointed out that under this trend, Morgan Stanley believes that TSMC will become a "long-term winner" in the AI trend-whether it is GPU or ASIC, cloud computing or edge AI, most of them need TSMC's cutting-edge foundry services, so the company has a great advantage in AI growth.

Morgan Stanley predicts that in 2024, the contribution of AI cloud business chip demand (excluding CPU) to TSMC's revenue will be 11%, and this number will increase to 20% by 2027. If the more extensive AI chip foundry business is taken into account, the contribution of AI business to TSMC's revenue will exceed 20% by 2025.

The report also stated that considering the possible factor of price increase, it raised TSMC's earnings per share expectations for 2026 by 6%, and raised its target price for the Taiwan stock (2330.TW) to TWD 980/share, which is still 9.8% higher than yesterday's closing price of TWD 894/share.

Since the beginning of this year, the US stock price of TSMC has risen cumulatively by 56.46%.

Editor/tolk