Travelite Holdings' (SGX:BCZ) Sluggish Earnings Might Be Just The Beginning Of Its Problems

Travelite Holdings' (SGX:BCZ) Sluggish Earnings Might Be Just The Beginning Of Its Problems

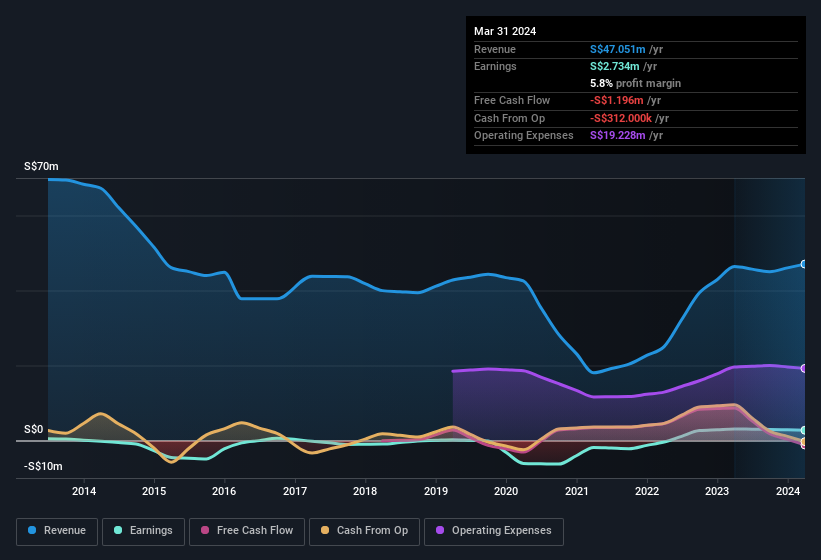

A lackluster earnings announcement from Travelite Holdings Ltd. (SGX:BCZ) last week didn't sink the stock price. However, we believe that investors should be aware of some underlying factors which may be of concern.

上週毅馬(新加坡交易所:BCZ)發佈的表現平淡的業績公告並未拖累股價。然而,我們認爲投資者應該注意一些可能令人擔憂的潛在因素。

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Travelite Holdings increased the number of shares on issue by 50% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Travelite Holdings' historical EPS growth by clicking on this link.

爲了了解每股收益的潛在回報能力,必須考慮公司使股東持股比例降低的程度。事實上,毅馬通過發行新股,在過去12個月內發行股票數量增加了50%。因此,現在每股股份獲得的利潤較小。若因淨利潤而忽略稀釋就好像因爲有一塊比較大的比薩而喜悅,但卻忽略了這個比薩現在被分割成了更多的小塊。請點擊此鏈接查看毅馬歷史每股收益增長情況。

A Look At The Impact Of Travelite Holdings' Dilution On Its Earnings Per Share (EPS)

毅馬稀釋對其每股收益(EPS)的影響

Three years ago, Travelite Holdings lost money. And even focusing only on the last twelve months, we see profit is down 12%. Sadly, earnings per share fell further, down a full 12% in that time. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

三年前,毅馬虧損。即使只關注過去12個月,我們也能看到利潤下降了12%。不幸的是,這段時間內收益進一步下降了整整12%。因此,您可以很明顯地看到稀釋對股東產生了相當大的影響。每股收益長期來看,如果毅馬的收益

In the long term, if Travelite Holdings' earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

注:我們始終建議投資者檢查資產負債表的健康狀況。單擊此處,以查看毅馬的資產負債表分析。每股收益請注意:我們始終建議投資者檢查資產負債表的強度。單擊此處,進入我們對萬集科技資產負債表的分析。

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Travelite Holdings.

我們對毅馬的利潤表現的看法

Our Take On Travelite Holdings' Profit Performance

毅馬今年發行了股票,這意味着其每股收益表現落後於淨利潤增長。因此,我們認爲毅馬的法定收益可能是判斷其潛在盈利能力的不良指標,並可能給投資者過於樂觀的印象。不幸的是,過去12個月其每股收益下降了。總之,如果您想全面了解該公司,必須考慮不止上述因素。如果您想了解毅馬作爲業務的更多內容,則應注意其面臨的任何風險。例如,我們已經確定了毅馬的3個警告信號(其中2個不太令人滿意)。

Travelite Holdings issued shares during the year, and that means its EPS performance lags its net income growth. For this reason, we think that Travelite Holdings' statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. Sadly, its EPS was down over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you'd like to know more about Travelite Holdings as a business, it's important to be aware of any risks it's facing. For instance, we've identified 3 warning signs for Travelite Holdings (2 don't sit too well with us) you should be familiar with.

這個備註只看了一個揭示毅馬利潤本質的因素。但是,如果您能夠集中您的注意力在細節上,就會有更多發現。有些人認爲高股本回報率是高質量業務的一個好跡象。因此,您可能希望查看具有高股本回報率的公司的免費收藏,或具有高內部所有權的股票清單。

This note has only looked at a single factor that sheds light on the nature of Travelite Holdings' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

請使用moomoo賬號登錄查看

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者,發送電子郵件至editorial-team (at) simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。