Source: Wall Street News

Authors: Li Dan, Fang Jiayao

The Dow's big rebound on Friday continued to fall for two weeks. The NASDAQ stopped falling more than 1% in the intraday period, and all surged in May; Nvidia rose 2% at the beginning of the market and then turned down; Apple rose five times, rising more than 13% in May; Dell recorded the biggest decline in history after the earnings report, chip stock Maywell Technology closed down more than 10%, and Gap rose more than 28% to record the biggest one-day gain in nearly half a year. China's stock index fell more than 1%, Xiaopeng Motors closed down 4%, Tencent's US stock fell more than 2%, and Krypton rose more than 2%.

After the PCE was announced, the decline in US bond yields accelerated, and the two-year yield hit a one-week low; the US dollar index fell monthly for the first time in May; crude oil and gold and silver rose in the intraday period and returned to a decline after a new high. Ethereum rose nearly 20% in May. The offshore renminbi fell 200 points in the intraday period and fell to 7.26. Crude oil fell three times in a row, closing close to a three-month low. May recorded its biggest monthly decline in the year. Gold fell to a one-week high and continued to rise for three months. Futures rose more than 10% in May. Lunzinc fell more than 3%, and Luntong fell to a three-week low and still rose for two months. Lunxi rose nearly 6% in May and continued to rise for half a year.

The inflation index favored by the Federal Reserve brought benefits from cooling inflation. Roughly as Wall Street expected, the growth rate was slightly slower than the previous month. The US core PCE price index rose 0.2% month-on-month in April, the lowest growth rate this year. The year-on-year growth rate of the index slowed to a three-year low of nearly 2.8%. However, the PCE report also showed that actual consumer spending did not increase month-on-month in April but fell 0.1%, increasing the signs that the US economy is slow.

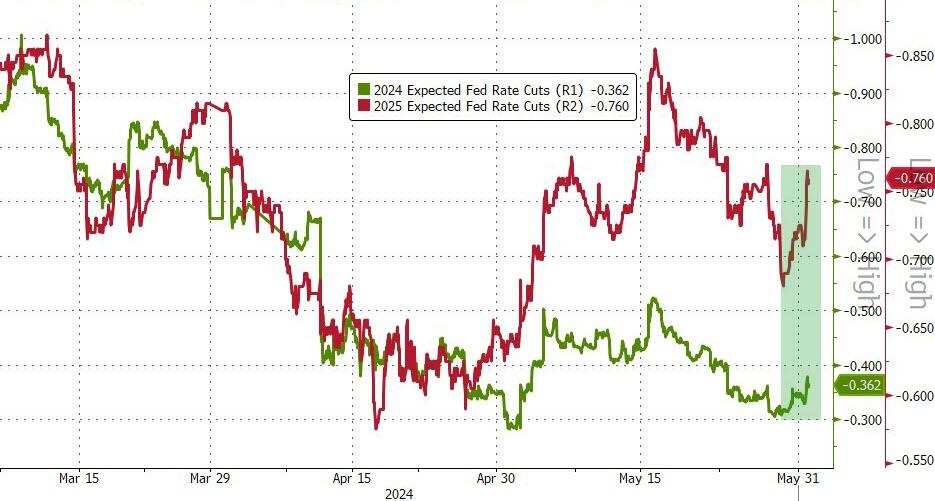

Commentary said that the PCE report added hope that the Fed would have room to cut interest rates this year, relieved Wall Street, which was nervous about the prospects of cutting interest rates after inflation heats up in the first three months of this year. Consumer spending, however, fell unexpectedly. Traders believe that for the Federal Reserve, which relies on data, this report should be “not too bad,” “slightly constructive,” and “slightly dovish.” Nick Timiraos, known as the new “Federal Reserve News Agency,” commented that the report largely met market expectations and was unlikely to change the Federal Reserve's existing wait-and-see position.

After PCE data was released, swap contract pricing showed that investors still expect the Federal Reserve to cut interest rates at least once this year; US Treasury bond prices continued to accelerate the intraday decline on Thursday. Benchmark 10-year US Treasury yields broke 4.50%, leveling off all increases since poor demand for two-year and five-year treasury tenders this Tuesday. Interest rate sensitive two-year US Treasury yields fell back to a one-week low, all falling more than 10 basis points from the four-week highs each set on Wednesday.

Technology stocks once again weighed down on US stocks, and the three major stock indexes fell sharply for a while. The chip stock index fell by more than 3% in the intraday market. Maiwell Technology, the leading component stock, benefited from AI demand and data center revenue surged 87% in the first fiscal quarter, but other businesses dragged down profits. Nvidia opened high and low in early trading and did not successfully turn up. Quarterly results failed to impress investors, Dell plummeted by more than 20% in the intraday market, leading the decline in AI concept stocks. Dell's highly anticipated backlog of AI server business orders increased 30% month-on-month to US$3.8 billion in the first fiscal quarter. The company's operating profit did not increase but declined during the quarter, causing analysts to doubt that the actual profit margin for AI servers was zero.

However, most sectors, led by energy, rebounded, and even some tech giants, such as Apple, tenaciously turned upward, supporting S&P to reverse the decline on Friday. Salesforce, which had a severe setback on Thursday after releasing poor earnings reports, led the Dow's constituent stocks. Although it declined on Friday, the overall gains of chip stocks and AI concept stocks remained unchanged in May. Dell still surged in double digits in May, and Nvidia rose nearly 30% throughout the month. Technology stocks driven by the AI boom were still a strong driver of the rise in US stocks in May.

In the foreign exchange market, after the PCE was announced, the decline in the US dollar index, which turned down in the intraday period, widened and reached a new low. May became the first month of decline this year, and the overall monthly decline in US bond yields partly reflected data such as the April CPI released in May showing the impact of cooling inflation. After PCE, most non-US currencies turned up in the intraday period. The yen has since returned to its decline, but it has not come close to the four-week low set on Wednesday. The offshore renminbi once smoothed out most of the intraday losses, then widened again and fell below 7.26.

Commodities generally declined. Interest rate cuts brought about by the US PCE failed to continue to support precious metals. After the PCE was announced, gold and silver first hit a new high and then fell. The intraday declines of New York futures and silver futures widened to more than 1% and 3%, respectively. London's basic metals continued to plummet. Zinc fell by more than 3%, and Lun Copper narrowly held the 10,000 US dollar mark. The analysis indicates that short-term copper demand is weak, offsetting speculative bets and causing copper prices to fall from a high point. China's May PMI data boom level declined somewhat on Friday. Demand for industrial products declined, and waste recycling increased refinery production, heightening market concerns about oversupply of copper.

After the PCE was announced, international crude oil rose and reached a new daily high, but expectations of interest rate cuts failed to continue to be boosted. Oil prices returned to a downward trend, falling for three days in a row, approaching the three-month low set a week ago, and uncertainty about demand continued to drag down the oil market. The US Energy Information Administration (EIA) announced on Friday that in March, US crude oil production rose to the highest level of 13.2 million barrels per day. Supply of petroleum products fell to 19.9 million b/d during the same period, and overall demand for petroleum products weakened. After the EIA data was released, crude oil declined at an accelerated pace, falling more than 1.6% in the intraday period. Some analysts pointed out that the decline in oil prices reflects the unease before the OPEC+ oil production policy meeting this Sunday. Although the market generally expects OPEC+ to extend current production cuts, they may also take unexpected measures.

The Dow rebounded on Friday and fell for two weeks after two consecutive weeks of earnings, Dell recorded the biggest decline in history. Maywell Technology fell more than 10%, and Gap rose more than 20%

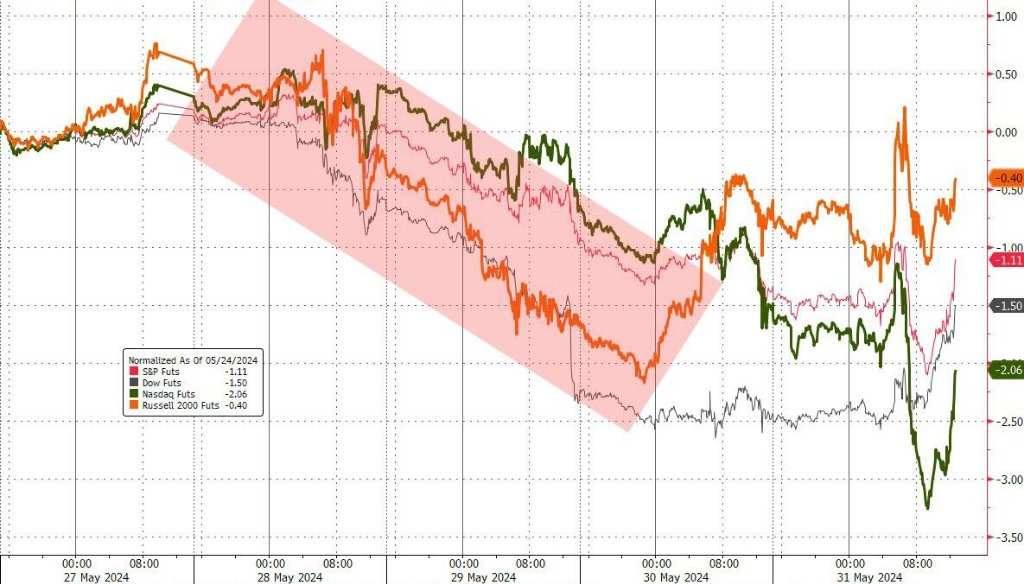

The three major US stock indexes collectively opened higher, with mixed intraday performance. The Dow Jones Industrial Average only declined in the short term in early trading. The rise accelerated in midday trading, and rose more than 600 points at the end of the session to a new daily high. The Nasdaq Composite Index, which rose nearly 0.3% at the beginning of the session, and the S&P 500 index, which rose nearly 0.2% at the beginning of the session, turned down in early trading. The NASDAQ index fell more than 1.7% and the S&P fell more than 0.8%. Later, the NASDAQ leveled off most of the declines, and the S&P rose and reached a new high at the end of the session. In the end, only the NASDAQ index did not close up, and the S&P and Dow stopped falling for two consecutive times.

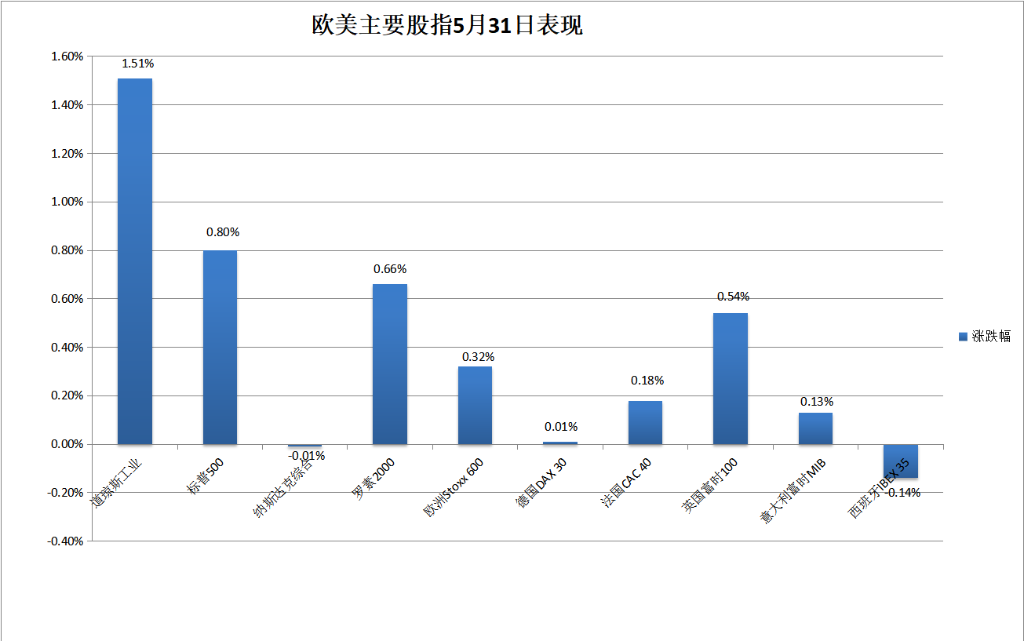

The Dow closed up 574.84 points, or 1.51%, the biggest point increase since June 2, 2023, and the biggest percentage increase since November 2, 2023, at 38686.32 points, breaking away from the closing low since May 1, which was refreshed by three consecutive days of decline. On Thursday, S&P, which hit a closing low since May 13, closed up 0.8% to 5277.51 points. The NASDAQ closed down 0.01% to 16735.02 points. It fell for three consecutive days and hit a new low since May 23 on the 2nd.

The S&P and Dow related ETFs SPDR S&P 500 ETF (SPY) and SPDR Dow Jones Industrial Average ETF (DIA) closed up 0.91% and 1.59% respectively on Thursday, rebounding after closing at new lows since May 13 and May 1, respectively. This week they fell by about 0.4% and 0.8%, respectively, and climbed nearly 5.1% and 2.5%, respectively, in May.

The small-cap stock index Russell 2000, which is mainly value stocks, closed up 0.66%, rising for two consecutive days until May 22. The tech-heavy Nasdaq 100 Index closed down 0.01%, and the related ETF Invesco QQQ Trust Series 1 (QQQ) closed down 0.19%, all falling three times in a row. The two days hit a low level since May 14. The latter fell 1.58% this week and climbed 6.15% in May. The Nasdaq Technology Market Capitalization Weighted Index (NDXTMC), which measures the performance of technology components in the NASDAQ 100 index, closed down 0.31%, falling 1.64% this week, and rising 9.36% in May.

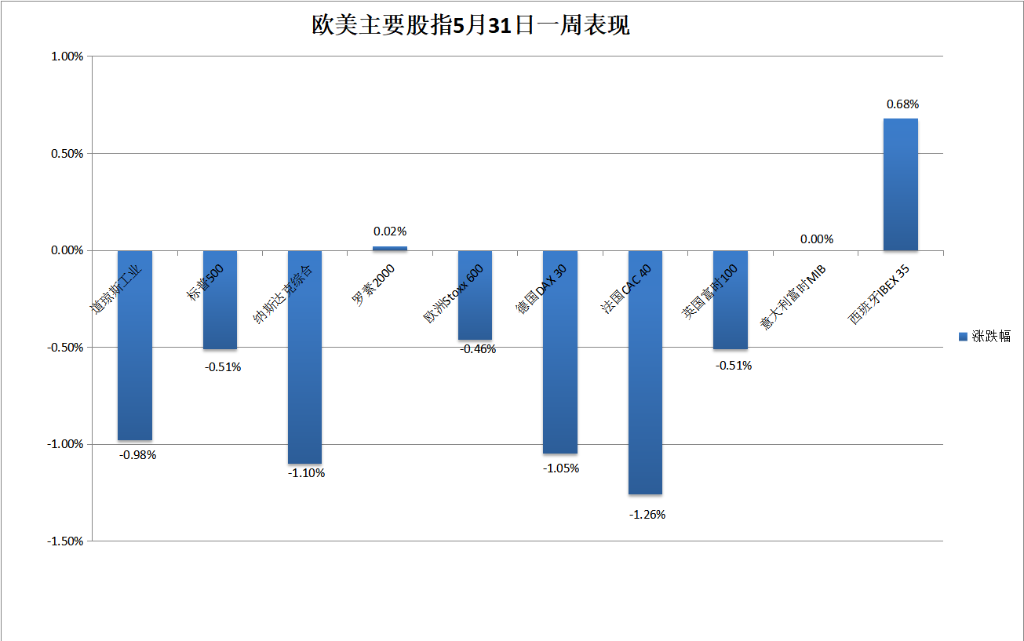

Major US stock indexes fell sharply this week: the S&P, NASDAQ, and NASDAQ 100 fell 0.51%, 1.1%, and 1.44% respectively, all ending five weeks of continuous gains; the Dow fell 0.98%, falling for two weeks after five consecutive weeks. This week's decline was less than 2.3%, the biggest weekly decline since March last year. However, Russell rose slightly by 0.02% in 2000, not continuing the four-week continuous decline that stopped last week.

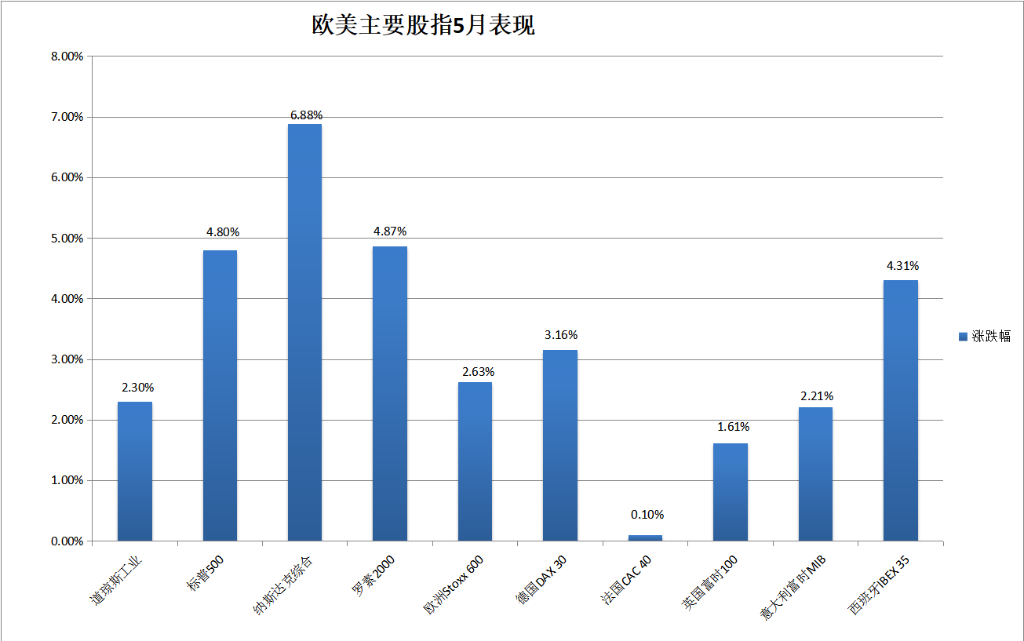

Major stock indexes surged across the board in May. S&P rose 4.8%, the Dow rose 2.3%, the NASDAQ rose 6.88%, and the Nasdaq 100 rose 6.28%. They all rebounded after falling back in April, and rose for the sixth month in the last seven months. Russell also rebounded in 2000, rising 4.87%, for the third month in the last four months.

Among the constituent stocks of the Dow, only Amazon, which fell more than 1%, and Caterpillar, which fell 0.2%, closed down on Friday. Salesforce, which plummeted 20% on Thursday after the financial report was announced, closed up 7.5%, and Unitehealth, the second-largest health care stock, rose nearly 2.9%. Among the ten sectors that closed higher, with the exception of communications services, which rose nearly 0.6%, and non-essential consumer goods, which rose nearly 0.2%, the others rose by at least 1%, leading the way in energy closing by nearly 2.5%.

A total of four sectors declined this week. IT fell nearly 1.5%, industry fell nearly 0.9%, communications services and healthcare fell 0.3%, non-essential consumer goods fell 0.3%, energy rose 2%, and showed the best performance. Interest rate sensitive real estate and utilities rose 1.8% and 1.6%, respectively. However, the IT sector continued to rise sharply by nearly 10% in May, followed by utilities rising by nearly 8.5%, real estate rising by nearly 5%, and energy falling only by nearly 1% throughout the month.

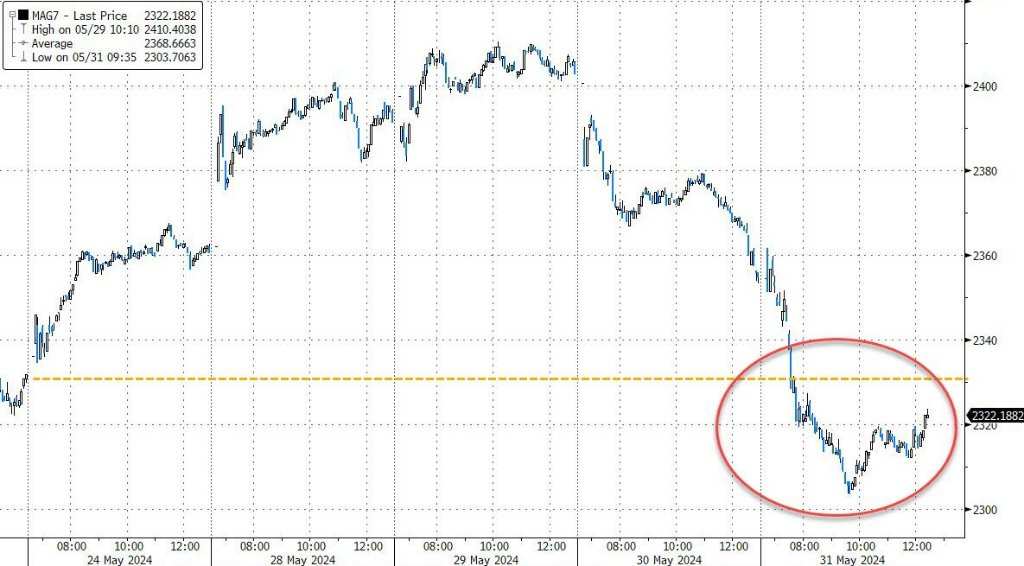

Including Microsoft, Apple, Nvidia, Google's parent company Alphabet, Amazon, Facebook's parent company Meta, and Tesla, the tech giants “Seven Sisters” had a sharp decline in the intraday period and partially turned up at the end of the session. Tesla, which rebounded on Thursday, turned up nearly 0.9% at the beginning of the session. After falling again in early trading, it fell about 2.8% in midday trading. It later smoothed out most of its losses and closed down 0.4%. It has fallen by nearly 0.7% this week and more than 2.8% in May.

Among the six major FAANMG technology stocks, Amazon has fallen 3% in the intraday period, closing down 1.6%, and closing low since April 30; Netflix, which fell more than 2% in early trading, fell nearly 0.9%, falling two times to a low level since May 17; while Apple, which had fallen more than 0.7% after falling in early trading, turned up for five days, breaking the high position since Tuesday, May 21, approaching the closing high since January 26; Microsoft, which had fallen more than 2% in the intraday session, and Alphabet, which had fallen more than 1% in the intraday session, both fell more than 1% in the end of the session Turned higher, closing up 0.1% and 0.2%, respectively, for the time being It was the lowest since May 13 and May 14 due to two consecutive declines; Meta, which fell by more than 2% in the intraday period, smoothed out its decline at the end of the session and closed up less than 0.1%, stopping two consecutive losses.

Most of these six technology stocks fell sharply this week. Microsoft fell nearly 3.5%, Meta and Amazon fell more than 2%, Alphabet fell more than 1%, Netflix fell more than 0.7%, while Apple rose 1.2%; in May, these tech stocks rose 16.6%, Apple rose 12.9%, Meta rose 8.6%, Microsoft rose 6.6%, Alphabet rose nearly 5.7%, and Amazon rose 0.8%.

Chip stocks continued to decline overall, narrowing the intraday decline by at least half. The Philadelphia Semiconductor Index and semiconductor industry ETF SOXX fell more than 3% in the midday session, closing down nearly 1% and 0.8%, respectively. They fell to their low levels since the 3rd until May 17. They have declined by about 1.9% this week, and have increased by about 9.6% and 9.4% respectively in May. Among chip stocks, Nvidia rose 2% at the beginning of the session. After falling by 3.2% in early trading, it narrowed most of its decline, closing down 0.8%, rising more than 2.9% this week, and rising more than 26.8% in May; after announcing earnings reports, Maywell Technology closed down 10.5%, Broadcom fell more than 2% at the close, Ram Research fell nearly 2%, and Micron Technology fell 1%, while AMD, which had fallen 4% in the intraday session, rose nearly 0.2%, and Intel rose more than 2%.

The overall decline in AI concept stocks continued. The AI and robotics stock ETF Glb X Robotics & Afl Intelligence ETF (BOTZ) fell more than 1% in the intraday period and closed up 0.1% after turning up at the end of the session, falling 2.4% this week, and rising 3% in May. After announcing financial reports, Dell (DELL) opened down 15.4%, fell more than 20% in early trading, and closed down 17.9% in mid-day trading, the biggest one-day decline since the US IPO in December 2018. It had a cumulative decline of nearly 13% this week, and continued to rise by nearly 11.6% in May; at the close, ultra-microcomputers (SMCI) fell more than 5%, BigBear.ai (BBAI) fell nearly 2%, Astera Labs (ALAB) fell more than 1%; Palantir (PLTR) fell 0.2%, and C3.ai (AI) With Soundhound.ai (SOUN), it rose more than 3%, and Oracle (ORCL) rose slightly.

Popular Chinese securities generally declined. The Nasdaq Golden Dragon China Index (HXC) and related ETF Invesco Golden Dragon China ETF (PGJ) fell more than 2% in early trading, closing down nearly 1.6% and 1.7%, respectively, breaking the closing lows set on Wednesday since May 1. Both have declined by more than 0.6% this week, and have accumulated gains of nearly 2.7% and more than 2.5% in May, respectively. KWEB and CQQQ closed down around 2% and 1.8%, respectively.

Among the new car builders, Xiaopeng Motors fell 4% at the close, and Ideal Auto fell by more than 2%. NIO Auto, which had risen more than 1% after turning up in early trading, fell nearly 0.2%, while Extreme Krypton, which turned up in early trading, rose more than 2%. Among other individual stocks, Tencent Music fell nearly 4%, Tencent Fandan and iQiyi fell more than 2%, Jingdong fell nearly 2%, Alibaba, Baidu, Pinduoduo, and NetEase fell more than 1%, while Station B rose about 0.7%.

The bank stock index rose for two consecutive days. The overall banking index KBW Bank Index (BKX) closed up 1.8%, breaking the high level since May 22, rising less than 0.1% this week, with a cumulative increase of 3.7% in May; the regional banking index KBW Nasdaq Regional Banking Index (KRX) closed up 1.2%, and the regional bank stock ETF SPDR S&P Regional Bank ETF (KRE) closed up 1.4%, all breaking the one-week high since May 24, with a cumulative decline of more than 0.1% this week, rising nearly 2.5% and 3.5% in May, respectively.

Among individual stocks with high fluctuations, fast fashion giant Gap (GAP) closed 28.6%, the biggest closing increase since November 17, 2023, after announcing that EPS profit for the first fiscal quarter far exceeded expectations, and raised the full-year guidance; cloud security company Zscaler (ZS), whose profit and revenue for the third fiscal quarter were higher than expected, closed 8.5%; after announcing steady sales growth in the first fiscal quarter, the discount chain Nordstrom Rack's sales increased by nearly 7% and reaffirmed the full-year results guidance, ) closed up 5%; clothing company VF Corp (VFC) closed 7.7% after announcing that Sun Choe, the former chief product officer of Lululemon, would be the company's global brand president; Faraday Future (FFIE) rose more than 21% at the beginning of the session, fell 3.5% after falling in early trading, and closed up 3.2% after turning up at the end of the session.

Meanwhile, the database software company MongoDB (MDB), which lowered its guidance for the second quarter and full year, closed down about 23.9%; cybersecurity company SentinelOne (S), whose annual revenue guidance fell 13.3%; after announcing a management reshuffle, the resignation of co-CEO Christopher Thomas, and the promotion of strategic advisor Randy Peck as Chief Operating Officer, the payroll and human capital management software company Paycom Software (PAYC) closed down nearly 8.6%.

In terms of European stocks, although the Eurozone CPI grew faster than expected, the market's expectations of the ECB's interest rate cut in June remained unchanged, and the US PCE temporarily mitigated concerns about inflation. The pan-European stock index rebounded for two days after two consecutive days of decline. The European Stoxx 600 index continues to break away from its closing low since May 6, which was refreshed on Wednesday. Most of the major European countries' stock indexes closed higher. British, French, and Italian stocks rose for two days, while German stocks and Western stocks, which rebounded on Thursday, generally closed down and fell, respectively.

Among the various sectors, utilities rose more than 1.1%, and medical sales rose nearly 1.1%. Among the constituent stocks, the Dutch-listed European pharmaceutical company Novo & Nord rose 1.1%, while the technology sector, which was influenced by its US stock peers, fell more than 1.3%. Among the constituent stocks, German-listed software giant SAP, which fell more than 4% on Thursday, fell nearly 1.6%, and ASML, Europe's highest market-capitalized technology stock listed in the Netherlands, fell nearly 1.2%.

The Stoxx 600 index fell for two consecutive weeks this week. Most stock indexes from various countries have plummeted. German, French and British stocks have fallen for three consecutive weeks. German stocks and French stocks have fallen more than 1%. Italian stocks remained roughly the same level as a week ago on Friday, and Western stocks, which fell back last week, rebounded. Among various sectors, real estate was able to rise nearly 1.5% this week due to a rise of nearly 2% on Thursday. The increase on Thursday was second only to the 1.7% increase for real estate Telecom for the whole week, while technology fell nearly 3.5% this week.

The Stoxx 600 index rose 2.6% in May, smoothing the decline in April and rising for the sixth month in the last seven months. Stock indices from all countries have risen. German, French, Italian and Western stocks rebounded after falling back in April, and British stocks have been rising for three consecutive months. Most of the sectors have been rising. Telecom rose more than 5%, and interest-rate sensitive real estate rose by more than 4%. Despite this week's poor performance, technology continued to rise 3.5% throughout the month.

US bond yields accelerated decline after PCE, two-year yields hit a one-week low

The price of European treasury bonds rose and fell in various ways. Yields rushed higher and fell during the intraday period. After the Eurozone CPI was announced, they reached a new high and low after the US PCE was announced. By the end of the bond market, the yield on the UK 10-year benchmark treasury bond was about 4.32%, down about 3 basis points during the day; the yield on 2-year British bonds was about 4.36%, down about 9 basis points during the day; the yield on the benchmark 10-year German treasury bond was about 2.66%, up about 1 basis point during the day. After the US PCE was announced, US stocks fell 2.64% in early trading and fell about 1 basis point during the day; the 2-year German bond yield was about 3.09%, up about 2 basis points during the day.

European bond yields will continue to rise sharply this week. The 10-year British bond yield has increased by a cumulative total of about 6 basis points. German bond yields have risen by about 8 basis points during the same period, all rising for 2 consecutive weeks. The latter has been rising for 5 weeks in the last 7 weeks. The 10-year British bond yield fell by a total of about 2 basis points in May. After rebounding in April, it declined for the second month of this year after March. German bond yields increased cumulatively by about 8 basis points during the same period, rising for 2 consecutive months.

The US Treasury Bond ETF (GOVT) closed up 0.38%, rising for two consecutive days, falling less than 0.1% this week and rising 1.1% in May.

The yield on the US 10-year benchmark treasury bond rose to a new high of 4.57% after the Eurozone CPI was released in early trading. The decline accelerated after the announcement of the US PCE. The US stock market fell 4.50% in early trading and fell below 4.49% in early trading. It returned to the level before the tender sale of the two batches of US Treasury bonds was completed this Tuesday. It fell about 15 basis points from the high level since May 2, which was refreshed after rising 4.63% on Wednesday. It was about 4.50% by the end of the day, falling by nearly 5 basis points during the day. About 4 basis points. After three weeks of continuous decline, it rose for 2 weeks. In April, there was a big rebound of about After 48 basis points, the cumulative decline was about 18 basis points in May, followed by a decline in the second month of this year after March.

The 2-year US bond yield, which is more sensitive to interest rate prospects, rose above 4.95% to 4.9518% on the European stock market, fell 4.90% after PCE was announced, and fell below 4.87% in early trading, breaking the low since May 23. It fell more than 13 basis points from the high level since May 1, which was close to the 5.0% refresh on Wednesday. It was about 4.87% at the end of the bond market. It fell nearly 6 basis points during the day, after four days of continuous rise, and a cumulative decline of about 8 days after the big rebound of more than 10 basis points last week. In terms of base points, it dropped by a total of about 17 basis points in May, and rose sharply above in April After 40 basis points, it fell, followed by a decline in the second month of this year after January.

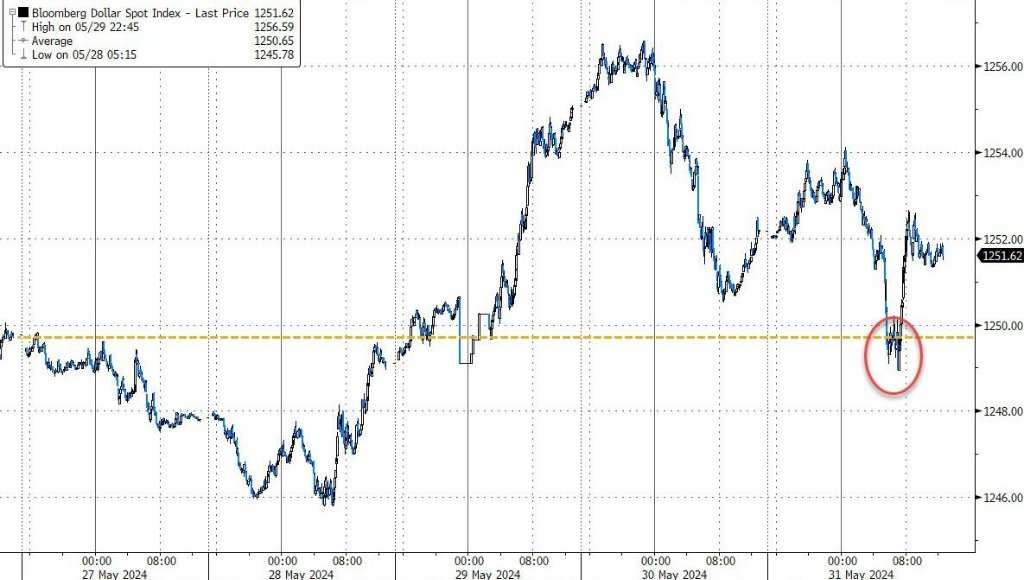

The US dollar index hit a new low day after PCE, fell monthly for the first time in May, and Ethereum rose nearly 20% in May

The ICE US Dollar Index (DXY), which tracks the exchange rate of a basket of six major currencies including the US dollar against the euro, reached a new daily high of 104.90 in the Asian market. European stocks turned down in early trading, and the decline widened after the US PCE was announced. US stocks fell below 104.40 in early trading, falling more than 0.3% during the day, falling from the high intraday level since May 13, which was refreshed close to 105.20 on Thursday.

By the end of the foreign exchange market on Friday, the US dollar index was below 104.70. After rebounding last week, it had a cumulative slight drop of 0.05% this week and a cumulative decline of 1.46% in May; the Bloomberg US Dollar Spot Index, which tracks the exchange rate of the US dollar against ten other currencies, fell 0.1% this week, fell 1.1% in May, and the US dollar index both fell continuously for 2 days and stopped rising for 4 months in May.

Among non-US currencies, the yen failed to continue its rebound on Thursday. The US dollar was close to 157.30 against the European stock market, close to the high level since May 1, when it rose above 157.70 on Wednesday. The US PCE accelerated its decline after the announcement, and the US stock market declined at the beginning of the session. US stocks fell below the 156.60 fresh day low in early trading, fell close to 0.2% during the day, and turned upward in early trading; after the PCE announcement, EUR/USD traded above 1.0880 before the market, and was close to breaking 1.0890 on Wednesday. High level, up nearly 0.5% during the day; the pound against the pound after PCE The US dollar reached a new daily high of 1.2770 in early trading. It rose 0.3% during the day. It turned down before midday trading, and was unable to approach the high level since March 21, when 1.2800 was refreshed on Tuesday.

The offshore renminbi (CNH) reached a new high of 7.2479 against the US dollar in early Asian trading, rising 58 points during the day. The US PCE narrowed most of its losses after the mid-day decline. The intraday decline was less than 20 points, then the decline widened. The early morning trading day of the US stock market was as low as 7.2683, down 204 points from the daily high, and began to fall to the intraday low since April 16, which was refreshed after falling at 7.27 on Wednesday. At 4:59 Beijing time on June 1, the offshore renminbi was reported at 7.2630 yuan against the US dollar, down 93 points from the end of Thursday in New York. It fell 15 points this week, falling for two consecutive weeks, and falling 82 points in May after rebounding in April, falling sharply for the fourth month in the last five months.

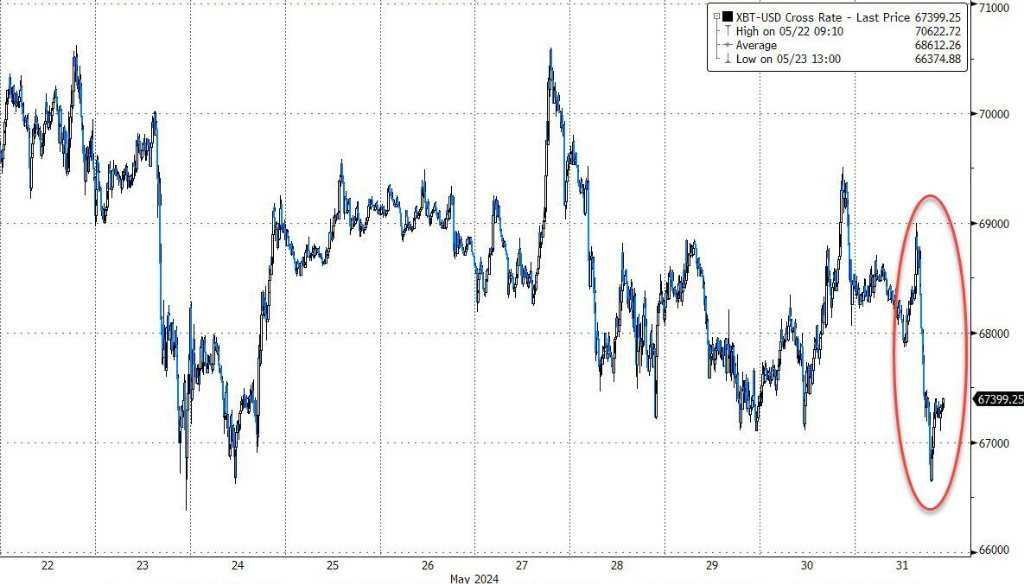

Bitcoin (BTC) was tested at 69,000 US dollars before PCE was announced, and some platforms returned to this level. US stocks fell below 67,000 US dollars to below 66,700 US dollars in midday trading, breaking the low since May 23, falling more than 2,000 US dollars and falling more than 3% from the daily high. US stocks were above 67,600 US dollars at the close, falling more than 1% in the last 24 hours, falling more than 2% in the last 7 days, and rising nearly 6% in May.

Ethereum (ETH), the second-largest cryptocurrency with market capitalization after Bitcoin, rose above $3,840 before the US stock market, and continued to regrow gains. The US stock market declined in the short term and fell below $3,730 during the midday session, falling more than 3% from the daily high. US stocks hovered at the $3,780 line at the close of the day, breaking away from the low level since May 24, which was refreshed by less than 1% in the last 7 days, and continued to rise by about 18% in May.

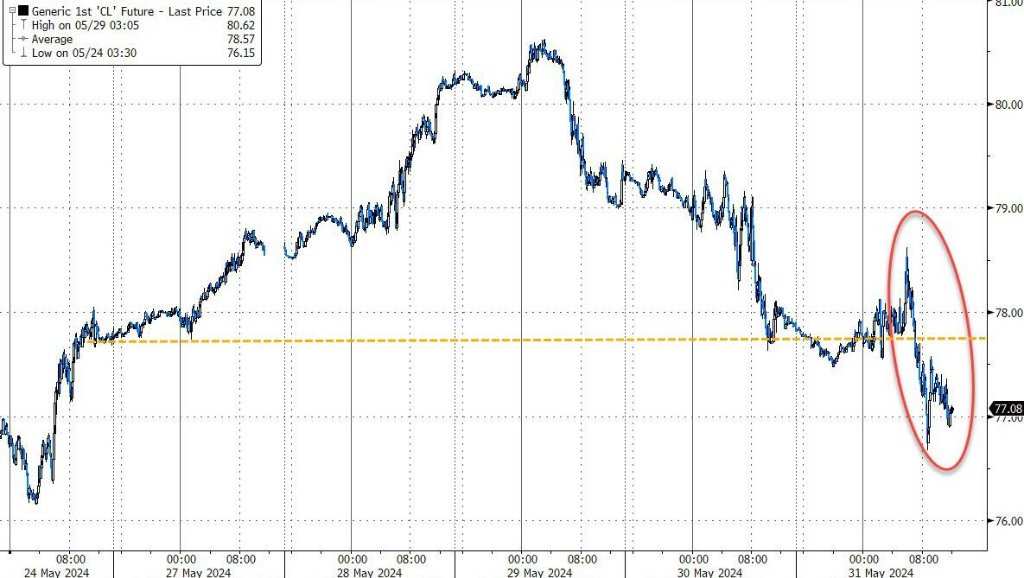

After PCE, crude oil rose for a while and closed close to a three-month low, May recorded the biggest monthly decline in the year

International crude oil futures declined several times in the intraday session on Friday. US stocks rose to 78.62 US dollars after the US PCE announcement and reached a new daily high. US WTI crude oil rose to 78.62 US dollars, rising more than 0.9% during the day. Brent crude oil rose to 82.18 US dollars, rising nearly 0.4% during the day, and continued to decline. After turning to early trading, the decline continued to expand. At a fresh low in midday trading, US oil fell to 76.67 US dollars, down nearly 0.9% during the day.

In the end, crude oil closed down for three consecutive days. WTI crude oil futures for July closed down $0.92, or 1.18%, to $76.99 per barrel; Brent crude oil futures for July closed down $0.24, or 0.29%, to $81.62 per barrel, and both broke their closing lows since May 23, approaching the three-month closing trough set by each on May 23.

US oil fell by 0.94% this week, and oil fell by about 0.61%, falling for two consecutive weeks. Oil fell for the fourth week in the last five weeks. In the 34 weeks since the outbreak of the conflict between Palestine and Israel, US oil has declined in the 19th week and oil has declined in the 16th week. In May, US oil fell by about 6%, and oil fell by about 7.1%, all of which were the biggest monthly declines this year. After rising for three months, US oil fell for two months, and oil fell for four months.

The US Oil ETF United States Oil Fund LP (USO) closed down 0.94%, down 0.7% this week, falling 4.54% in May; the oil ETF United Sttes Brent Oil Fund LP (BNO) closed down 0.73%, down 0.62% this week, and 4.85% in May, all falling from three consecutive days to May 23.

US gasoline and natural gas futures rebounded after falling for two consecutive days on Thursday. On Thursday, NYMEX's June gasoline futures, which hit a low level since February 29, were about 0.95%, at 2.4260 US dollars/gallon, and fell by about 2.3% this week, falling more than 10% in May, falling for two months; on Thursday, NYMEX July natural gas futures, which hit a low level since May 14, closed up about 0.6% to 2.587 US dollars/million British thermal units, falling 6.7% this week for two consecutive weeks.

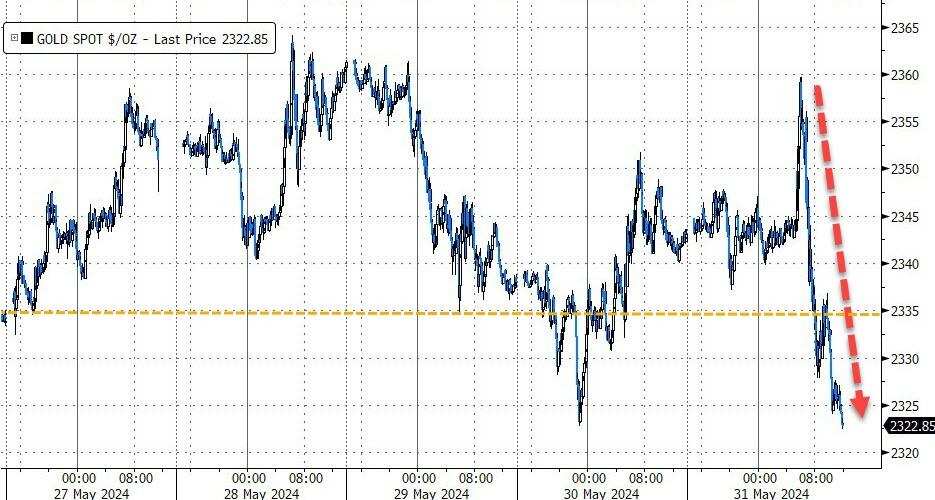

Lunzinc fell more than 3%, and Luntong fell to a new low for three weeks after PCE, gold and silver rose more than 10% in May

London basic metals futures continued to fall sharply on Friday. Lunzinc, which led the decline, fell more than 3%, closing below $3,000 for the first time in two weeks. Helun Aluminum, Lunnickel, and Renxi all fell for two consecutive days. The latter three hit new lows in the past week, more than two weeks, and nearly three weeks respectively. The decline of Luntong, which fell more than 3% on Thursday, eased somewhat. It closed down less than 1%, but it fell for three consecutive days, closing close to the 10,000 US dollar mark for the first time in three weeks. Lun lead fell four days in a row and continued to hit a new low of more than two weeks.

Basic metals fell all this week. Lunzinc, which had been rising for four weeks, dropped nearly 2.9%, while Lunn Copper fell nearly 2.8%, and Lunxi, which fell nearly 2.7%, and Lunxi, which fell nearly 0.6%, all fell for two weeks. Lun lead, which had been rising for four weeks, fell more than 1%, and Lunn Aluminum, which had been rising for two weeks, fell nearly 0.4%. Basic metals continued to rise across the board in May. Lunxi rose nearly 5.9%, rising for six months. Luntong rose nearly 0.5%, far less than April when it rose nearly 13%, and Lunzn, which rose more than 2%, and Lunzn, which rose 1.5%, both rose for three months. Both ln nickel and ln lead rose more than 2% and two months in a row.

Gold declined on Friday and turned higher in the intraday period. After the US PCE was announced, when US stocks rose to a new high before the market, New York gold futures rose to 2381.2 US dollars, up more than 0.6% during the day. Spot gold approached 2,360 US dollars, rising more than 0.4% during the day. After falling by 0.4% in early trading, US stocks declined overall. At a fresh low in midday trading, futures fell to 2341.1 US dollars, falling nearly 1.1% during the day. Spot gold fell below $2,321, down nearly 1% during the day.

By the end of midday US stock futures trading, COMEX June gold futures, which rebounded to a high closing level since May 22, closed down 0.87% to 2345.8 US dollars/ounce. This week they had accumulated gains of 0.48% and 1.86% in May. SPDR Gold Trust (GLD) closed down 0.59%, falling about 0.3% this week and rising 1.6% in May. At the close of the US stock market, spot gold was below $2,330, falling more than 0.6% during the day.

New York futures declined for two days after three consecutive gains. COMEX silver futures closed down 3.47% to $30.44 per ounce in July, breaking the low since May 16 at $29.876, falling 0.19% this week and rising 14.2% in May. Both this week and futures rebounded after falling back last week. Both this week and futures rebounded after falling back last week, rising for three consecutive months in the last four weeks. Asus Silver Trust SLV closed down 2.32%, rising 0.07% this week and 15.43% in May.

Editor/Jeffy