Kencana Agri Limited's (SGX:BNE) Shares Leap 44% Yet They're Still Not Telling The Full Story

Kencana Agri Limited's (SGX:BNE) Shares Leap 44% Yet They're Still Not Telling The Full Story

For example, consider that Kencana Agri's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

For example, consider that Kencana Agri's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price. Kencana Agri Limited (SGX:BNE) shares have had a really impressive month, gaining 44% after a shaky period beforehand. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

肯卡納農業有限公司(新加坡證券交易所股票代碼:BNE)的股價表現非常令人印象深刻,在經歷了動盪時期之後上漲了44%。長期股東將對股價的回升表示感謝,因爲在最近的反彈之後的一年中,股價幾乎持平。

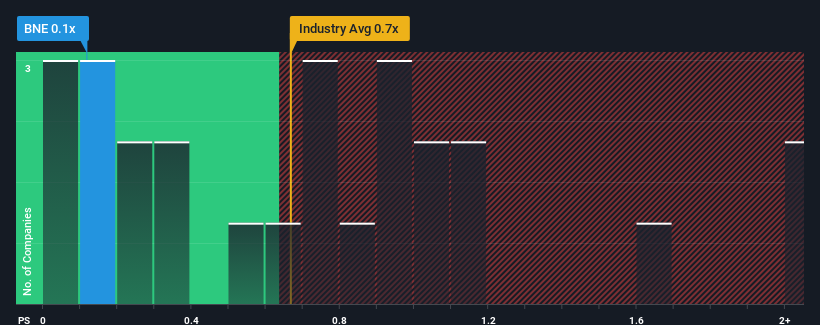

Even after such a large jump in price, it would still be understandable if you think Kencana Agri is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.1x, considering almost half the companies in Singapore's Food industry have P/S ratios above 0.7x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

即使在價格大幅上漲之後,考慮到新加坡食品行業將近一半公司的市盈率高於0.7倍,你認爲Kencana Agri是一隻具有良好投資前景的股票,其市銷率(或 “市盈率”)爲0.1倍,還是可以理解的。但是,市銷率低可能是有原因的,需要進一步調查以確定其是否合理。

SGX:BNE Price to Sales Ratio vs Industry May 30th 2024

新加坡證券交易所:BNE 與行業的股價銷售比率 2024 年 5 月 30 日

What Does Kencana Agri's P/S Mean For Shareholders?

肯卡納農業的市銷率對股東意味着什麼?

For example, consider that Kencana Agri's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

例如,假設Kencana Agri最近由於收入下降而財務表現不佳。一種可能性是市銷率很低,因爲投資者認爲公司在不久的將來在避免整個行業表現不佳方面做得還不夠。但是,如果最終沒有發生這種情況,那麼現有股東可能會對股價的未來走向感到樂觀。

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Kencana Agri's earnings, revenue and cash flow.

我們沒有分析師的預測,但您可以查看我們關於Kencana Agri收益、收入和現金流的免費報告,了解最近的趨勢如何爲公司未來做好準備。

What Are Revenue Growth Metrics Telling Us About The Low P/S?

收入增長指標告訴我們低市銷率有哪些?

In order to justify its P/S ratio, Kencana Agri would need to produce sluggish growth that's trailing the industry.

爲了證明其市銷率是合理的,Kencana Agri需要實現落後於該行業的緩慢增長。

Retrospectively, the last year delivered a frustrating 11% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 31% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

回顧過去,去年該公司的收入下降了11%,令人沮喪。但是,在此之前的幾年非常強勁,這意味着它在過去三年中仍然能夠將總收入增長31%,令人印象深刻。因此,我們可以首先確認該公司在此期間在增加收入方面總體上做得非常出色,儘管在此過程中遇到了一些小問題。

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 2.8% shows it's noticeably more attractive.

將最近的中期收入軌跡與該行業2.8%的年度增長預測進行比較,可以看出該行業明顯更具吸引力。

With this in mind, we find it intriguing that Kencana Agri's P/S isn't as high compared to that of its industry peers. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

考慮到這一點,我們發現有趣的是,Kencana Agri的市銷率與業內同行相比沒有那麼高。顯然,一些股東認爲最近的表現已經超過了極限,並且一直在接受大幅降低的銷售價格。

What We Can Learn From Kencana Agri's P/S?

我們可以從 Kencana Agri 的市銷率中學到什麼?

Despite Kencana Agri's share price climbing recently, its P/S still lags most other companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

儘管肯卡納農業最近股價上漲,但其市銷率仍然落後於大多數其他公司。我們可以說,市銷比率的力量主要不是作爲一種估值工具,而是用來衡量當前的投資者情緒和未來預期。

We're very surprised to see Kencana Agri currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see robust revenue growth that outpaces the industry, we presume that there are notable underlying risks to the company's future performance, which is exerting downward pressure on the P/S ratio. It appears many are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

我們非常驚訝地看到,Kencana Agri目前的市銷率遠低於預期,因爲其最近三年的增長高於整個行業的預期。當我們看到強勁的收入增長超過該行業時,我們認爲公司的未來業績存在明顯的潛在風險,這給市銷率帶來了下行壓力。看來許多人確實在預測收入不穩定,因爲近期這些中期狀況的持續下去通常會提振股價。

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Kencana Agri that you should be aware of.

在投資之前,還有其他重要的風險因素需要考慮,我們發現了Kencana Agri的一個警告信號,你應該注意這一點。

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

重要的是要確保你尋找一家優秀的公司,而不僅僅是你遇到的第一個想法。因此,如果盈利能力的增長與你對一家優秀公司的想法一致,那就來看看這份免費名單吧,列出了最近收益增長強勁(市盈率低)的有趣公司。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接聯繫我們。或者,也可以發送電子郵件至編輯團隊 (at) simplywallst.com。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。