Surmodics, Inc. (NASDAQ:SRDX) shares have had a really impressive month, gaining 63% after a shaky period beforehand. The last month tops off a massive increase of 130% in the last year.

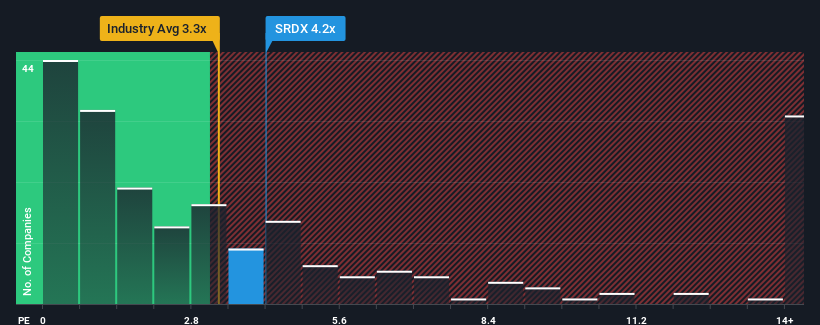

After such a large jump in price, Surmodics may be sending sell signals at present with a price-to-sales (or "P/S") ratio of 4.2x, when you consider almost half of the companies in the Medical Equipment industry in the United States have P/S ratios under 3.3x and even P/S lower than 1.2x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

NasdaqGS:SRDX Price to Sales Ratio vs Industry May 30th 2024

What Does Surmodics' P/S Mean For Shareholders?

Surmodics certainly has been doing a good job lately as it's been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Surmodics will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The High P/S?

In order to justify its P/S ratio, Surmodics would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 39% last year. The latest three year period has also seen an excellent 34% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the four analysts covering the company suggest revenue growth is heading into negative territory, declining 8.9% over the next year. Meanwhile, the broader industry is forecast to expand by 9.7%, which paints a poor picture.

In light of this, it's alarming that Surmodics' P/S sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a very good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

The Final Word

The large bounce in Surmodics' shares has lifted the company's P/S handsomely. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Surmodics' analyst forecasts revealed that its shrinking revenue outlook isn't drawing down its high P/S anywhere near as much as we would have predicted. Right now we aren't comfortable with the high P/S as the predicted future revenue decline likely to impact the positive sentiment that's propping up the P/S. At these price levels, investors should remain cautious, particularly if things don't improve.

Plus, you should also learn about these 2 warning signs we've spotted with Surmodics (including 1 which is concerning).

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.