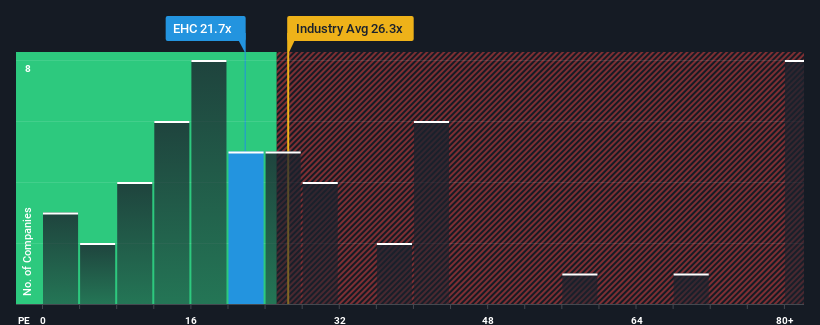

Encompass Health Corporation's (NYSE:EHC) price-to-earnings (or "P/E") ratio of 21.7x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 17x and even P/E's below 9x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Recent times have been pleasing for Encompass Health as its earnings have risen in spite of the market's earnings going into reverse. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors' willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:EHC Price to Earnings Ratio vs Industry May 29th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Encompass Health.

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Encompass Health's is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 38%. EPS has also lifted 25% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 6.2% per year during the coming three years according to the ten analysts following the company. That's shaping up to be materially lower than the 10.0% per year growth forecast for the broader market.

With this information, we find it concerning that Encompass Health is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Encompass Health currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Encompass Health, and understanding them should be part of your investment process.

If you're unsure about the strength of Encompass Health's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Encomass Health Corporation(紐約證券交易所代碼:EHC)的市盈率(或 “市盈率”)爲21.7倍,與美國市場相比,目前可能看起來像賣出,美國約有一半的公司的市盈率低於17倍,甚至市盈率低於9倍也很常見。但是,僅按面值計算市盈率是不明智的,因爲可以解釋爲什麼市盈率如此之高。

If we review the last year of earnings growth, the company posted a terrific increase of 38%. EPS has also lifted 25% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

If we review the last year of earnings growth, the company posted a terrific increase of 38%. EPS has also lifted 25% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

如果我們回顧一下去年的收益增長,該公司公佈了38%的驚人增長。每股收益也比三年前增長了25%,這主要歸功於過去12個月的增長。因此,股東可能會對中期收益增長率感到滿意。

如果我們回顧一下去年的收益增長,該公司公佈了38%的驚人增長。每股收益也比三年前增長了25%,這主要歸功於過去12個月的增長。因此,股東可能會對中期收益增長率感到滿意。