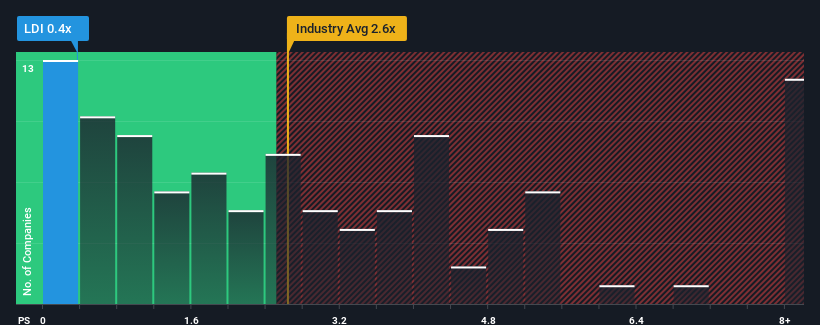

loanDepot, Inc.'s (NYSE:LDI) price-to-sales (or "P/S") ratio of 0.4x might make it look like a strong buy right now compared to the Diversified Financial industry in the United States, where around half of the companies have P/S ratios above 2.6x and even P/S above 5x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

NYSE:LDI Price to Sales Ratio vs Industry May 29th 2024

How Has loanDepot Performed Recently?

Recent times haven't been great for loanDepot as its revenue has been rising slower than most other companies. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on loanDepot.

Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as depressed as loanDepot's is when the company's growth is on track to lag the industry decidedly.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.0% last year. Still, lamentably revenue has fallen 83% in aggregate from three years ago, which is disappointing. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 28% as estimated by the four analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 3.5%, which is noticeably less attractive.

With this in consideration, we find it intriguing that loanDepot's P/S sits behind most of its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On loanDepot's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

loanDepot's analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. The reason for this depressed P/S could potentially be found in the risks the market is pricing in. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

Plus, you should also learn about this 1 warning sign we've spotted with loanDepot.

If you're unsure about the strength of loanDepot's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

LoanDepot, Inc. '與美國的多元化金融行業相比,s(紐約證券交易所代碼:LDI)的市銷率(或 “市盈率”)爲0.4倍可能使其看起來像是一個強勁的買盤。在美國,約有一半的公司的市盈率高於2.6倍,甚至市盈率高於5倍也很常見。但是,我們需要更深入地挖掘,以確定大幅降低市銷率是否有合理的基礎。